{kind=link}

Global markets are having a precious moment of calm, with risk sentiment stabilizing across Asia and Europe, and US futures pointing to a higher open. The recent wave of aggressive selling appears to have peaked—at least temporarily—offering traders a breather from the huge volatility experienced since last week. However, this rebound should not be mistaken for a true reversal in sentiment. Markets remain highly sensitive, and downside risks persist should trade tensions escalate further.

The immediate flashpoint lies in US-China relations. US President Donald Trump has warned that if China does not withdraw its 34% retaliatory tariffs by Wednesday, the US will impose an additional 50% tariff on Chinese goods. Should that happen, the effective tariff rate on Chinese imports would soar beyond 100%, marking a significant and historic escalation in global trade conflict.

Meanwhile, Chinese authorities are making visible efforts to bolster domestic market confidence. Sovereign wealth fund Central Huijin Investment, often dubbed the “national team,” confirmed ETF purchases and pledged further action to support equity prices. This has been echoed by major state-owned enterprises and listed firms announcing share buybacks. In tandem, China’s financial regulator is preparing to lift caps on insurance fund investments in equities to provide further support to the capital markets.

Beyond equity stabilization, currency markets are on alert. The Chinese Yuan is nearing record lows against Dollar, with market speculations over whether Beijing will allow it to depreciate as a countermeasure to tariffs. Should the PBoC relax its grip and let the Yuan slide further, it could trigger fresh turbulence in the regional markets that ripples globally.

From a pure technical perspective, USD/CNH’s correction from 7.3964 should have completed at 7.2153 already. Firm break of 7.3964/3745 key resistance zone will quickly push USD/CNH to 61.8% projection of 6.9709 to 7.3694 from 7.2153 at 7.4616.

In Europe, at the time of writing, FTSE is up 2.54%. DAX is up 2.57%. CAC is up 2.34%. UK 10-year yield is up 0.029 at 4.636. Germany 10-year yield is up 0.056 at 2.667. Earlier in Asia, Nikkei rose 6.03%. Hong Kong HSI rose 1.51%. China Shanghai SSE rose 1.58%. Singapore Strait Times fell -2.01%. Japan 10-year JGB yield rose 0.163 to 1.279.

ECB’s de Guindos urges cool heads as Europe faces trade wake-up call

ECB Vice-President Luis de Guindos struck a cautiously hopeful tone on Europe’s ability to manage rising global trade tensions, suggesting that markets tend to overreact in the short term but eventually recalibrate.

Speaking at an event in Spain, de Guindos noted that despite the sharp volatility triggered by the US tariff escalation, market liquidity remains intact.

Despite the pressure, de Guindos said he was “relatively optimistic” about Europe’s ability to weather the storm, calling the situation a “wake-up call” to pursue greater economic and military autonomy.

De Guindos stressed the importance of negotiating with the U.S. “with a cool head”.

Separately, Greek ECB Governing Council member Yannis Stournaras offered a more cautious view, warning that a renewed surge in inflation or rising inflation expectations could disrupt ECB’s path to monetary policy normalization.

“Tariffs imposed on one country’s imports would affect other countries participating in the global chains, even if no countermeasures were imposed,” Stournaras added.

Aussie Westpac consumer sentiment slumps post-tariff shock; RBA seen tilting toward May rate cut

Australia’s Westpac Consumer Sentiment index plunged -6.0% in April, dropping from 95.9 to 90.1. The steep fall was notably skewed by the timing of the survey in relation to US announcement of reciprocal tariffs on April 2.

Respondents surveyed before the announcement showed only a modest dip in sentiment to 93.9. Those surveyed after reported a sharp drop of nearly 10% to 86.6. .

The sub-indices measuring sentiment towards the economy were particularly hard-hit, with the outlook for the next 12 months falling -5.7% to 90.5, and the 5-year outlook slipping back by -3.0%

With RBA set to meet on May 19-20, Westpac believes the weakening external backdrop, coupled with softer inflation, will push RBA to deliver another 25 bps rate cut. RBA is likely to become “much more focused on downside risks to growth than lingering questions about inflation”.

Australia NAB business confidence dips to -3 ahead of tariff impact

Australia’s NAB Business Confidence index dipped slightly from -2 to -3 in March, remaining firmly in negative territory. Business Conditions, however, edged up from 3 to 4, a modest improvement that still leaves them slightly below average overall.

Cost pressures remained broadly stable, with purchase costs rising 1.4% in quarterly equivalent terms and product price growth holding at 0.5%. Labour cost growth eased slightly.

NAB Chief Economist Sally Auld noted that conditions continue to vary across industries, with the services sector faring best while manufacturing and retail remain under pressure.

Importantly, this data predates the escalation of the global trade dispute, particularly the reciprocal tariff measures announced in early April. As Auld cautioned, these developments could “flow through to forward looking measures in the next survey.”

RBNZ set to cut again, bearish momentum resumes in NZD/JPY

RBNZ is widely expected to deliver another 25bps cut tomorrow, bringing the Official Cash Rate down to 3.50%. With the move largely priced in, traders will be focused on how the central bank interprets the rapidly evolving global environment.

As the first major central bank to meet since the US launched the sweeping reciprocal tariffs, RBNZ’s tone and guidance will not only be key for New Zealand, but will also offer insights for the broader Asia-Pacific region.

While there are speculative whispers about the possibility of a larger-than-expected rate cut to cushion the economy against the external shock, RBNZ will likely refrain from doing so just yet. The current level of uncertainty, both in terms of policy responses and economic impact, should see the central bank remain cautious, maintaining its easing bias without overcommitting.

With another cut already projected in May, RBNZ is expected to stay on its path of gradual policy accommodation while waiting for more concrete data on trade disruption effects. The question of whether the RBNZ will eventually push OCR below 3.00% remains open. Much will depend on how the trade war unfolds, how consumer and business sentiment hold up, and the extent of the ripple effects across Asia’s open economies.

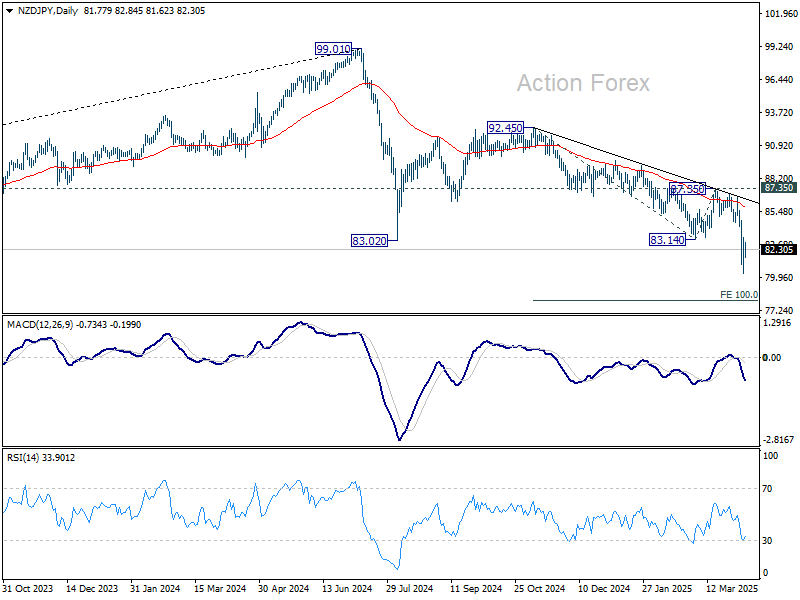

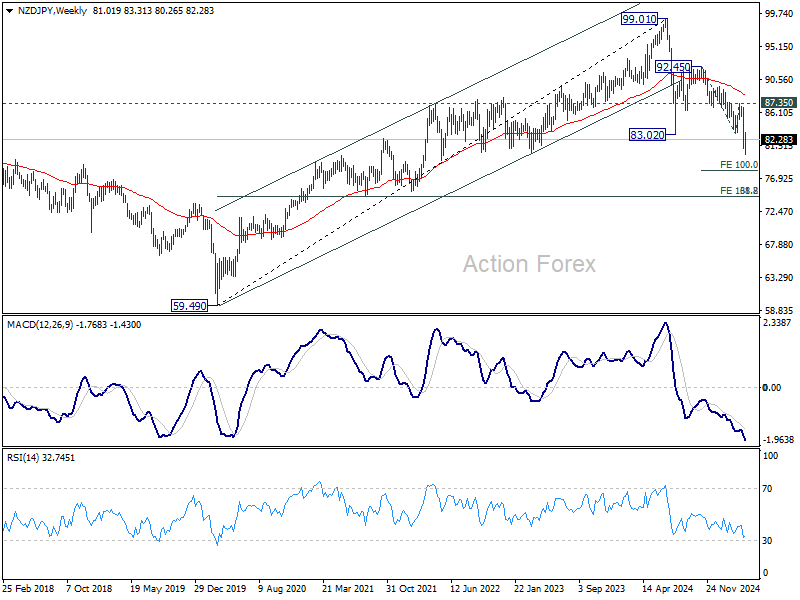

Technically, NZD/JPY’s down trend from 99.01 (2024 high) resumed by breaking through 83.02 low last week. Whether this is a correction of the multi-year uptrend from the 2020 low of 59.49, or a full reversal, is yet to be determined.

In either case, near term outlook will remain bearish as long as 87.35 resistance holds, in case of recovery. Next target is 100% projection of 92.45 to 83.14 from 87.35 at 78.04. Firm break there will target 138.2% projection at 74.48. This coincides with 61.8% retracement of 59.49 to 99.01 at 74.58.

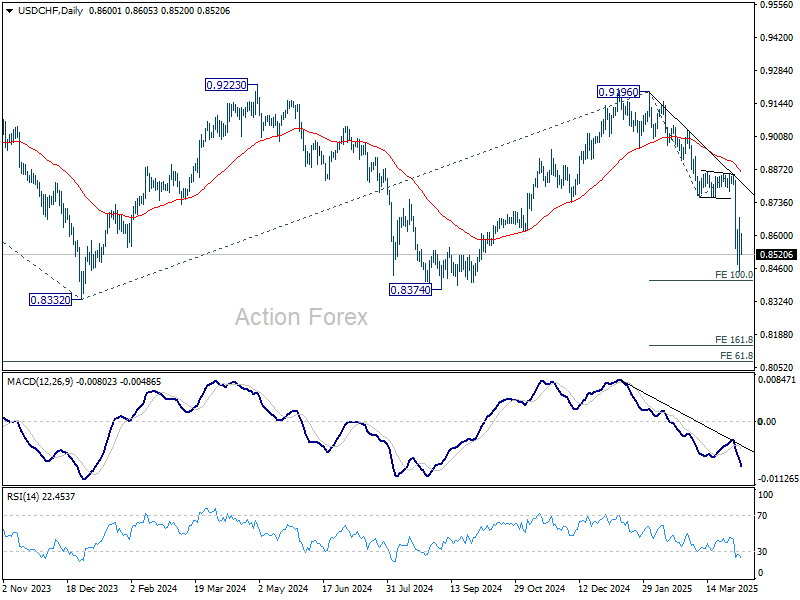

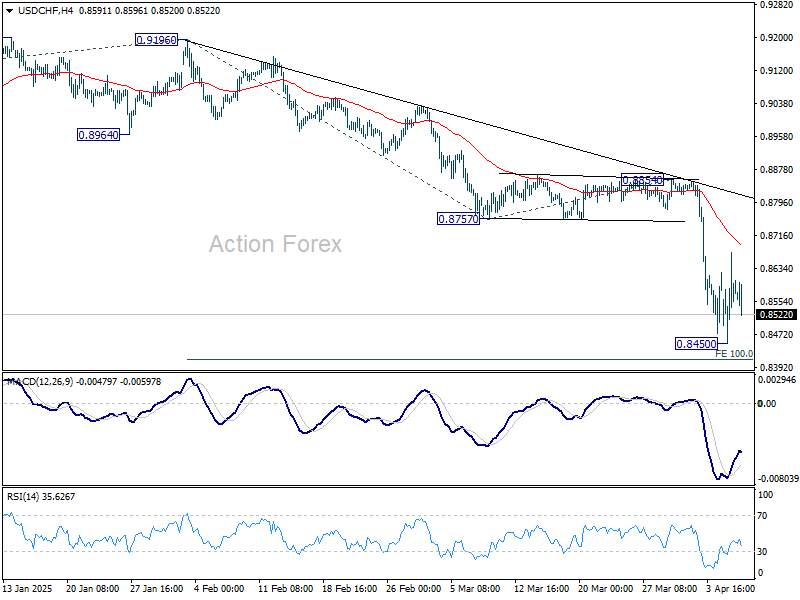

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8480; (P) 0.8577; (R1) 0.8704; More…

Intraday bias in USD/CHF remains neutral for the moment, and more consolidations would be seen above 0.8450. Upside of recovery should be limited below 0.8757 support turned resistance. On the downside, below 0.8450 will resume the fall from 0.9196 and target 100% projection of 0.9196 to 0.8757 from 0.8854 at 0.8415.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption. Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075.