{kind=link}

Risk aversion deepened across global markets today as China unveiled a forceful response to the sweeping US tariffs announced earlier this week. Beijing will impose an additional 34% tariff on all US goods starting April 10, in a move that effectively escalates the trade war into a full-scale economic confrontation. China sent the signal that it’s prepared to endure economic pain to counter US pressure. The Chinese Commerce Ministry justified the decision on grounds of national security and international obligations, but the timing and scope leave no doubt it’s a retaliatory measure.

US stock futures plunged in response, with DOW pointing to another 1000-point drop at the open. Wall Street’s mood was already fragile after a volatile week driven by tariff headlines, and the market’s inability to find relief even after a much stronger-than-expected non-farm payrolls report highlights the depth of the panic. Traders are rushing into US Treasuries, pushing the 10-year yield below the key 3.9% level, a sign of rising demand for safe havens amid intensifying uncertainty.

In the currency markets, Aussie has taken the hardest hit, tumbling sharply after China’s retaliation was announced. Kiwi followed as the second-worst performer. Loonie also weakened notably after domestic employment data showed a surprise job loss in March, though it remains a distant third among the day’s laggards.

On the flip side, Swiss Franc extended its stellar run to lead the pack again today. Yen is also well supported, though not quite matching the Franc’s gains. Euro remains relatively firm, continuing to draw strength as a liquid alternative to Dollar amid global uncertainty. Meanwhile, Sterling and Dollar are holding in the middle of the pack.

In Europe, at the time of writing, FTSE is down -3.50%. DAX is down -3.46%. CAC is down -3.22%. UK 10-year yield is down -0.092 at 4.439. Germany 10-year yield is down -0.145 at 2.511. Earlier in Asia, Nikkei fell -2.75%. Japan 10-year JGB yield fell -0.195 to 1.156. Singapore Strait Times fell -2.95%. Hong Kong and China were on holiday.

US NFP grows 228k, unemployment rate ticks up to 4.2%

US labor market showed unexpected strength in March, with non-farm payrolls rising by 228k, well above the consensus estimate of 128k. Growth was also notably stronger than the prior 12-month average of 158k.

The robust job gains highlight continued resilience in hiring, even amid heightened uncertainty surrounding trade policies and financial conditions.

Unemployment rate ticked up slightly from 4.1% to 4.2%, marking the upper end of its recent range, though the increase was accompanied by a modest uptick in labor force participation to 62.5%.

Average hourly earnings rose 0.3% month-over-month, aligning with expectations, suggesting that wage pressures remain steady.

Canada posts surprise -32.6k job loss

Canada’s labor market delivered a sharp disappointment in March, with employment falling by -32.6k, well below expectations of a 10.4k gain.

This marked the first monthly job loss since January 2022 and was driven by a steep decline in full-time positions, which dropped by 62k. Employment rate dipped 0.2 percentage points to 60.9%.

The unemployment rate ticked up to 6.7%, in line with expectations. Wage growth slowed to 3.6% yoy from 3.8% yoy in February.

BoJ’s Ueda: US tariffs likely to pressure Japan’s economy

BoJ Governor Kazuo Ueda warned that the 24% tariffs imposed by the US on Japanese goods could have broad implications. He emphasized that heightened uncertainty over the economic outlook may weigh on corporate sentiment and trigger volatile market behavior. This, in turn, could place “downward pressure on global and Japanese economies”.

Meanwhile, Ueda noted that the effect on inflation remains uncertain, as the tariffs could either suppress prices by weakening demand or push them higher through supply chain disruptions.

Despite these concerns, Ueda maintained a cautiously optimistic view on Japan’s economy. He pointed out that corporate sentiment remains positive, and capital expenditure plans are stronger than in the same period of prior years.

He referred to the latest Tankan survey as supportive of BoJ’s baseline view that Japan’s economy is “recovering moderately”. Still, Ueda noted that the survey, conducted from late February to March 31, may not have fully captured the impact of the US tariff announcements.

BoJ Deputy Governor Shinichi Uchida, also speaking at the session, reiterated that the central bank remains committed to adjusting rates if the likelihood of achieving its 2% inflation target increases.

Uchida emphasized that future policy decisions will be made on a meeting-by-meeting basis, based on updated forecasts, “without any preconception”.

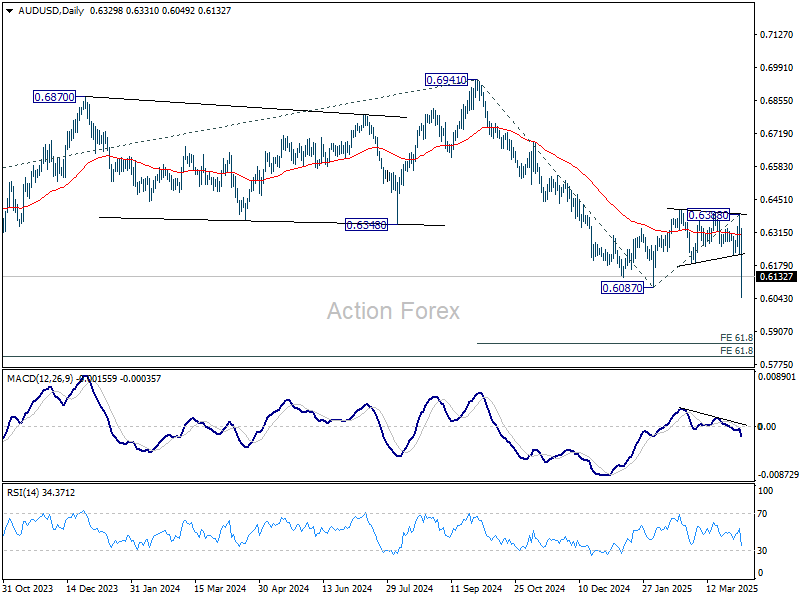

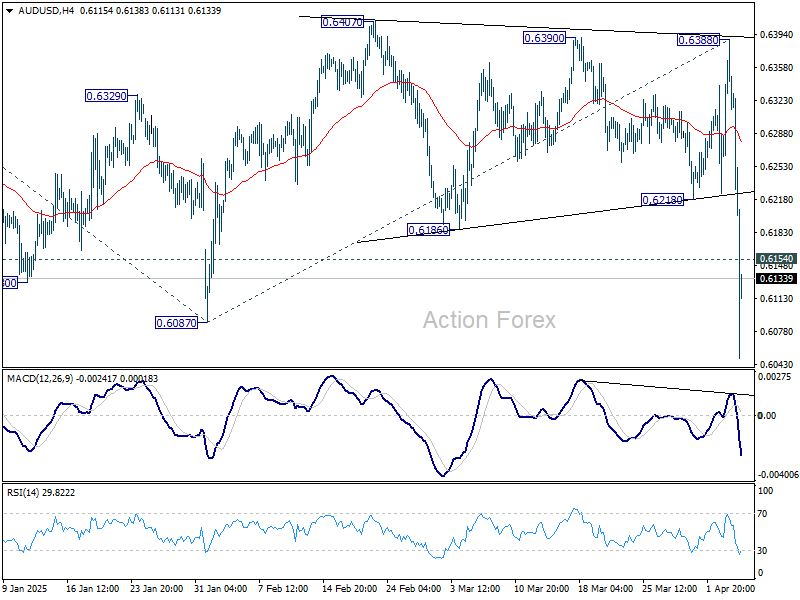

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6240; (P) 0.6315; (R1) 0.6403; More...

AUD/USD’s steep decline today and breach of 0.6087 support indicates resumption of whole fall from 0.6941. Intraday bias is back on the downside. Next target is 61.8% projection of 0.6941 to 0.6087 from 0.6388 at 0.5860. On the upside, above 0.6154 minor resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 0.6388 resistance holds.