{kind=link}

Risk aversion is sweeping through global financial markets today, with equities across Asia and Europe plunging ahead of the US’s so-called tariff “Liberation Day” on April 2. The selloff began in Asia, and continued through European Session. US futures are also pointing sharply lower, with the tech-heavy NASDAQ bearing the brunt of the pressure. Meanwhile, Gold continues to surge, with prices pushing above 3120 and showing no signs of slowing.

Currency markets reflect the prevailing risk-off tone, with Yen leading gains as investors seek refuge. Dollar and Sterling are also relatively firm. Aussie, Kiwi and Loonie are the weakest performers. Euro and Swiss Franc are trading mixed in the middle.

Australia’s RBA decision tomorrow will be in focus, though it’s unlikely to trigger fireworks. The central bank is widely expected to keep rates on hold at 4.10%, emphasizing its vigilance on inflation while pushing back on expectations for a rapid easing cycle.

The big four banks are split on the path forward. CBA, Westpac, and NAB anticipate three more RBA cuts this year starting in May, subject to Australia’s Q1 CPI report due April 2. ANZ, on the other hand, sees just one more cut in August, which would leave the cash rate at 3.85%.

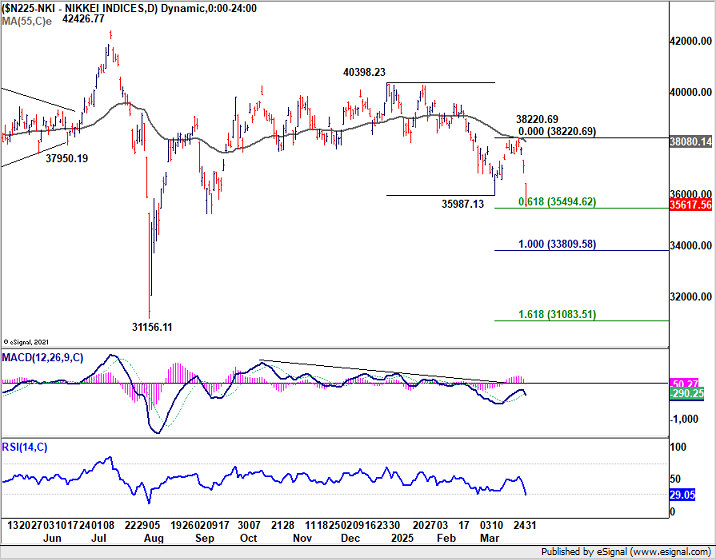

Technically, Nikkei broke through 35987.13 to resume the decline from 40398.23. The development affirms that case that corrective pattern from 42426.77 (2024 high) is already in its third leg. Firm break of 61.8% projection of 40398.23 to 35987.13 from 38220.69 at 35494.62 could prompt downside acceleration to 100% projection at 33809.58. If realized, the next fall in Nikkei would likely be accompanied by another down leg in USD/JPY.

In Europe, at the time of writing, FTSE is down -1.26%. DAX is down -1.73%. CAC is down -1.71%. UK 10-year yield is down -0.051 at 4.660. Germany 10-year yield is down -0.04 at 2.695. Earlier in Asia, Nikkei fell -4.05%. Hong Kong HSI fell -1.31%. China Shanghai SSE fell -0.46%. Singapore Strait Times fell -0.23%. Japan 10-year JGB yield fell -0.066 to 1.488.

ECB Lagarde: Europe must march toward economic independence amid tariff threats

ECB President Christine Lagarde emphasized the need for Europe to assert more control over its economic future in light of looming US tariffs, set to begin on April 2.

In a France Inter radio interview, Lagarde reframed the narrative around “Liberation Day,” saying that while the US sees it as a move toward sovereignty, Europe must seize it as an inflection point—“a march toward independence.”

Lagarde reiterated her previous estimates that tariffs from the US could shave around 0.3% off Eurozone growth in the first year. Should Europe retaliate with reciprocal measures, the negative impact could deepen to as much as 0.5%.

On inflation, Lagarde noted that keeping it in check remains a “constant battle.” She stressed that while some progress has been made, inflation needs to fall in a sustainable way. That, she said, requires a carefully calibrated interest rate policy.

ECB’s Panetta: Uncertainty demands caution on rate cuts

Italian ECB Governing Council member Fabio Panetta warned that the battle against inflation “cannot yet be said to be over.” and urged caution in the timing of interest rate cuts.

In a speech today, Panetta pointed to the heightened uncertainty stemming from “contradictory” announcements on US trade policy, suggesting that such unpredictability complicates the ECB’s path forward. As a result, the central bank must continue to monitor “all the factors that could hinder the return to the 2% target”

Panetta emphasized the balancing act the ECB now faces. On one hand, subdued consumption and investment, driven by geopolitical tensions and weak Eurozone growth, are helping to ease inflationary pressures.

But on the other hand, the resurgence of uncertainty—particularly around US tariffs—means the ECB must remain vigilant and not rush into policy loosening.

Japan’s industrial production beats with 2.5% mom growth in Feb

Japan’s industrial production rose 2.5% mom in February, beating market expectations of 1.9% mom gain. The strong growth was driven by key tech-related sectors, with chipmaking machinery output jumping 8.2% and electronic parts and devices surging 10.1%.

A survey by Ministry of Economy, Trade and Industry projects continued, albeit modest, gains in output of 0.6% mom in March and 0.1% mom in April.

While the headline data is encouraging, the METI acknowledged that the outlook could quickly shift. Though no direct production impact from the proposed US tariffs has been reported yet, METI emphasized the need to monitor the situation more closely going forward.

On the consumer side, retail sales grew just 1.4% yoy, missing expectations of a 2.4% rise.

NZ ANZ business confidence dips to 57.5, rising inflation expectations stir doubts over RBNZ cuts

New Zealand’s ANZ Business Confidence dipped slightly from 58.4 to 57.5 in March. Own Activity Outlook improved from 45.1 to 48.6.

However, the data also brought a clear warning on inflationary pressures. Cost expectations surged from 71.3 to 74.1, the highest level in a year. Pricing intentions climbed from 46.2 to 51.3, marking the strongest since May 2023.

Perhaps more importantly, one-year inflation expectations also ticked up from 2.53% to 2.63%, inching further above the RBNZ’s 2% midpoint target.

ANZ flagged the rising inflation signals as “a little disconcerting,” cautioning that these developments could influence how enthusiastic RBNZ will be about delivering further rate cuts.

A rate cut at the April meeting appears locked in, and a second in May is viewed as likely. However, ANZ noted that the odds of a third cut in July are now “more of a coin toss.”

China’s official PMI manufacturing rises to 50.5, but labor market lags

China’s official PMI data for March offered modest optimism, with the manufacturing index rising from 50.2 to 50.5, matching expectations and marking its highest level in a year.

Sub-indices for production and new orders both improved to 52.6 and 51.8, respectively. However, employment index slipped to 48.2, highlighting persistent weakness in labor market conditions within the manufacturing sector.

Non-manufacturing activity also improved slightly, with the PMI climbing from 50.4 to 50.8, beating expectations of 50.5.

Still, employment in the non-manufacturing sector deteriorated, with the index falling to 45.8, as both the services and construction sectors shed workers.

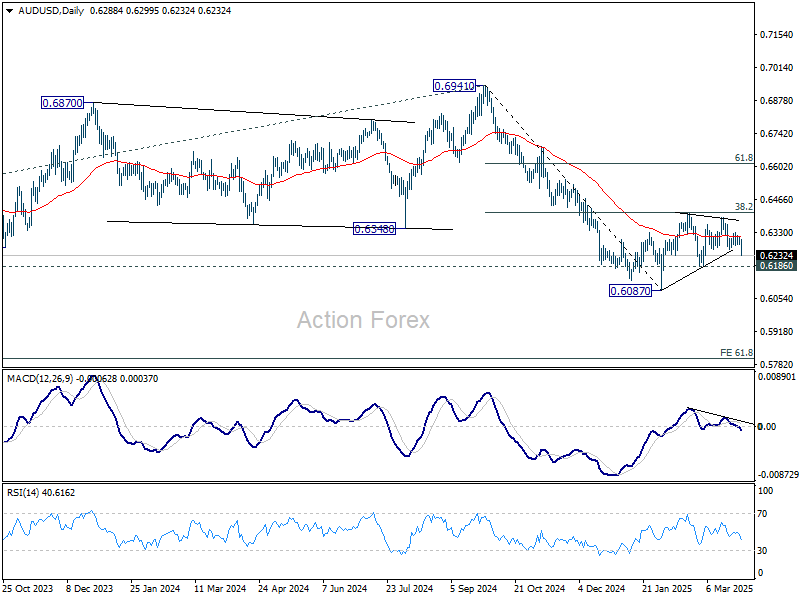

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6275; (P) 0.6293; (R1) 0.6306; More...

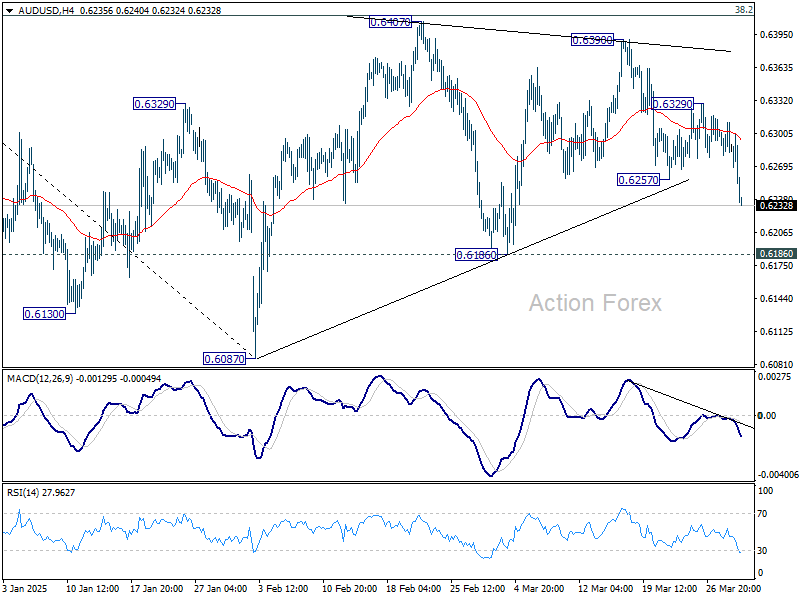

Intraday bias in AUD/USD is back on the downside with break of 0.6257 support. Fall from 0.6390 should now target 0.6186 next. Firm break there e will indicate that corrective pattern from 0.6087 has completed and larger fall from 0.6941 is ready to resume. For now, risk will stay on the downside as long as 0.6329 resistance holds, in case of recovery.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6467) holds.