{kind=link}

Risk aversion erupted across Asian markets today, with Japan bearing the brunt of the selloff. Nikkei plummeted by nearly than -4%, marking its worst day in months and sending the index to its lowest level since September last year. The sharp move comes as traders scramble to reassess the impact of US President Donald Trump’s 25% tariffs on all automobile imports, which are set to take effect Thursday. Previously, there had been some hope that Japan, a long-standing US ally, might be spared. But with no signs of exemption, the market is now forcefully pricing in the worst-case scenario.

Japanese Yen surged broadly on the wave of safe-haven buying, with investors rushing to unwind risk trades amid intensifying global trade tensions. The Yen’s rally was amplified by the direct blow to Japan’s key auto sector, a pillar of its export economy. The sharp shift in sentiment underscores how markets had underappreciated the possibility of Japan being caught in the crossfire of Trump’s aggressive trade policy.

The turbulence comes just days ahead of the so-called “Liberation Day” on Wednesday, when the US is expected to announce sweeping reciprocal tariffs on trading partners. The threat of a global trade war escalation is now overtaking all other themes in the market, overshadowing this week’s otherwise significant calendar including the US ISM indexes, non-farm payrolls, Eurozone inflation, and RBA rate decision.

Overall in the currency markets, Yen is by far the top performer today so far, followed by another safe haven Swiss Franc. Sterling is holding up better than most, helped by reports that British Prime Minister Keir Starmer and President Trump had “productive” trade talks over the weekend, suggesting the UK may be spared from some of the harsher tariff measures.

Commodity currencies are the clear losers, with Kiwi and Aussie at the bottom of the board amid their risk-sensitive profiles and economic ties to China. Loonie, Dollar, and Euro are also under pressure, though less dramatically.

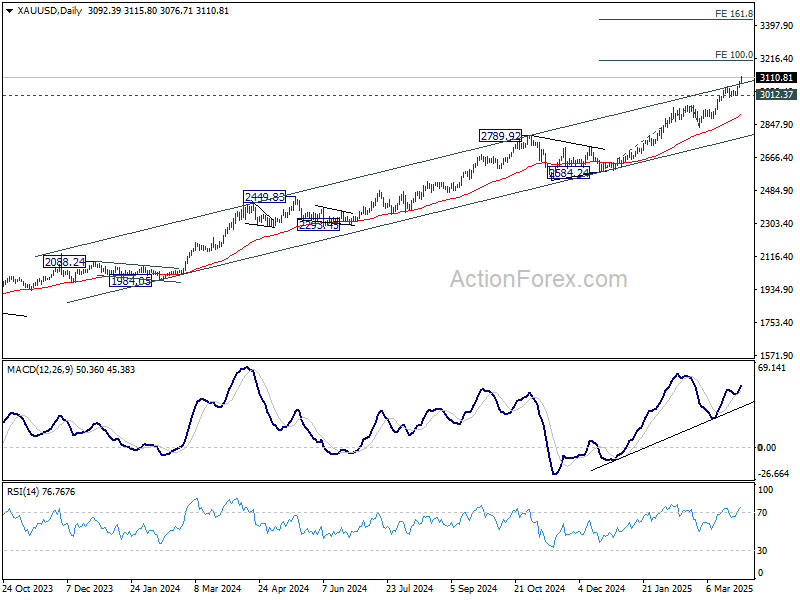

Risk aversion also pushed Gold to new record high above 3100 mark. Technically, the break of medium term channel resistance is a significant sign of upside acceleration. For now, near term outlook will stay bullish as long as 3012.27 support holds. Next target is 100% projection of 2584.24 to 2956.09 from 2832.41 at 3204.26. But considering current momentum, Gold might indeed be having an eye on 161.8% projection at 3434.06, or even 3500 psychological level already.

In Asia, at the time of writing, Nikkei is down -3.95%. Hong Kong HSI is down -1.48%. China Shanghai SSE is down -0.68%. Singapore Strait Times is down -0.23%. Japan 10-year JGB yield is down -0.044 at 1.510.

Japan’s industrial production beats with 2.5% mom growth in Feb

Japan’s industrial production rose 2.5% mom in February, beating market expectations of 1.9% mom gain. The strong growth was driven by key tech-related sectors, with chipmaking machinery output jumping 8.2% and electronic parts and devices surging 10.1%.

A survey by Ministry of Economy, Trade and Industry projects continued, albeit modest, gains in output of 0.6% mom in March and 0.1% mom in April.

While the headline data is encouraging, the METI acknowledged that the outlook could quickly shift. Though no direct production impact from the proposed US tariffs has been reported yet, METI emphasized the need to monitor the situation more closely going forward.

On the consumer side, retail sales grew just 1.4% yoy, missing expectations of a 2.4% rise.

NZ ANZ business confidence dips to 57.5, rising inflation expectations stir doubts over RBNZ cuts

New Zealand’s ANZ Business Confidence dipped slightly from 58.4 to 57.5 in March. Own Activity Outlook improved from 45.1 to 48.6.

However, the data also brought a clear warning on inflationary pressures. Cost expectations surged from 71.3 to 74.1, the highest level in a year. Pricing intentions climbed from 46.2 to 51.3, marking the strongest since May 2023.

Perhaps more importantly, one-year inflation expectations also ticked up from 2.53% to 2.63%, inching further above the RBNZ’s 2% midpoint target.

ANZ flagged the rising inflation signals as “a little disconcerting,” cautioning that these developments could influence how enthusiastic RBNZ will be about delivering further rate cuts.

A rate cut at the April meeting appears locked in, and a second in May is viewed as likely. However, ANZ noted that the odds of a third cut in July are now “more of a coin toss.”

China’s official PMI manufacturing rises to 50.5, but labor market lags

China’s official PMI data for March offered modest optimism, with the manufacturing index rising from 50.2 to 50.5, matching expectations and marking its highest level in a year.

Sub-indices for production and new orders both improved to 52.6 and 51.8, respectively. However, employment index slipped to 48.2, highlighting persistent weakness in labor market conditions within the manufacturing sector.

Non-manufacturing activity also improved slightly, with the PMI climbing from 50.4 to 50.8, beating expectations of 50.5.

Still, employment in the non-manufacturing sector deteriorated, with the index falling to 45.8, as both the services and construction sectors shed workers.

Central banks and top-tier data share spotlight with tariffs

Markets are understandably fixated on the looming April 2 announcement of reciprocal tariffs by the US. However, this week is also packed with central bank events and high-impact economic data that could shift sentiment and market direction.

RBA will be a key event, with broad consensus pointing to a hold at 4.10%. Despite some recent softness in data, RBA officials have maintained a modestly hawkish stance following the February rate cut. A follow-up move in April appears unlikely, especially with the next quarterly inflation report not due until April 30. The big four banks—CBA, Westpac, NAB, and ANZ—all expect the central bank to stay on hold this month.

Meanwhile, the US will release a slate of economic data, including ISM manufacturing and services indexes and the all-important non-farm payrolls report. ISM manufacturing dipped back into contraction in February, but the services side has remained resilient. So far, tariff threats have not shown up in the ISM data, but it’s unclear whether that changes in March’s readings. The labor market remains a key variable—strong job growth would support Fed’s patient stance. But a sudden deterioration, though likely viewed as noise, could still rattle policymakers.

The Eurozone’s flash CPI will be equally important as speculation builds over a potential rate pause by the ECB. While some members have floated the idea of holding rates in April, data hasn’t been convincing enough to justify it. This week’s inflation print could be the deciding factor. Additionally, ECB minutes from the March meeting will be dissected for clues about internal divisions and how much weight is being placed on the evolving external risks like tariffs.

Beyond these, there are several key international releases to keep an eye on. Japan’s Tankan business sentiment survey, Canada’s employment data, Swiss CPI, and China’s PMIs will round out a dense calendar.

Here are some highlights for the week:

- Monday: Japan industrial production, retail sales; New Zealand ANZ business confidence; China official PMIs; Germany import prices, retail sales, CPI flash; US Chicago PMI.

- Tuesday: Japan Tankan survey, PMI manufacturing final; China Caixin PMI manufacturing; RBA rate decision, Australia retail sales; Swiss retail sales; Eurozone PMI manufacturing final, CPI flash, unemployment rate; UK PMI manufacturing final; Canada PMI manufacturing; US ISM manufacturing.

- Wednesday: Japan monetary base; US ADP employment, factory orders.

- Thursday: Australia trade balance; China Caixin PMI services; Swiss CPI; Eurozone PMI services final, PPI, ECB accounts; UK PMI services final; Canada trade balance; US jobless claims, trade balance, ISM services.

- Friday: Japan household spending; Swiss unemployment rate; Germany factor orders; UK PMI construction; Canada employment; US non-farm payrolls.

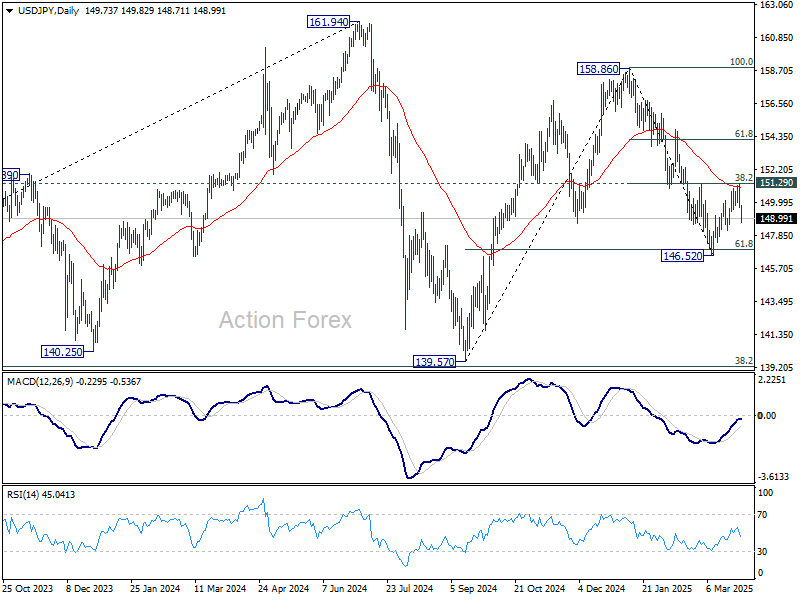

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.26; (P) 150.23; (R1) 150.79; More…

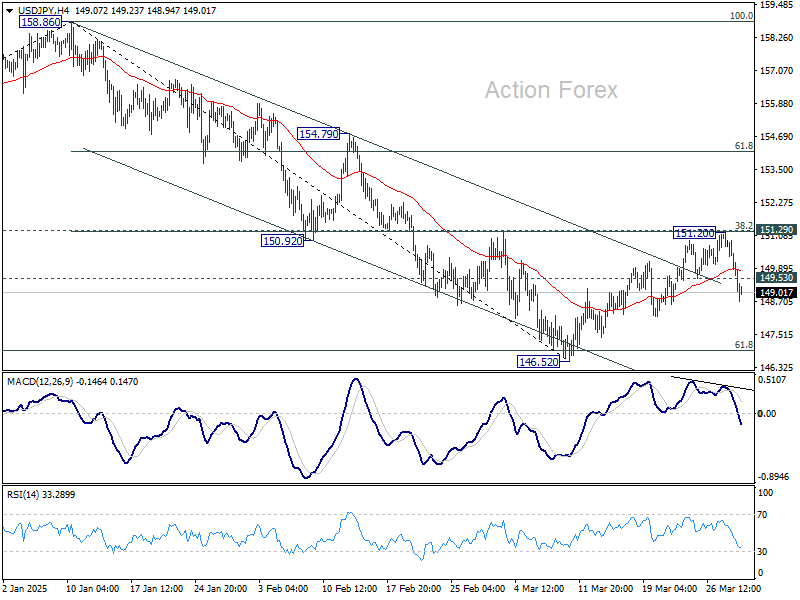

USD/JPY’s break of 149.53 support suggests that corrective recovery has already completed at 151.20. That came just ahead of 151.29 cluster resistance (38.2% retracement of 158.86 to 146.52 at 151.23). Intraday bias is back on the downside for retesting 146.52 low first. Firm break there will resume whole decline from 158.86 towards 139.57 support next. For now, outlook will remain bearish as long as 151.23/9 holds in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.