{kind=link}

Global headlines remain focused on US President Donald Trump’s unfolding tariff regime. But traders are telling a slightly different story. FTSE and DAX slip into negative territory, but the pullback in equities remains limited. Sterling and Euro are both strengthening against Dollar indeed.

Tones out of London and Brussels are in stark contrast. UK Chancellor Rachel Reeves signaled a desire to avoid escalation, saying the UK has no intention to join the trade war at this stage. European Commission President Ursula von der Leyen struck a firmer stance, warning the US tariffs would harm businesses and consumers. EU also vowed retaliation with a “robust toolbox.”

So far, it appears that the bounce in EUR/USD and GBP/USD are mainly due to Dollar’s own weakness. If anything, Dollar’s decline suggests traders might already be pre-positioning for next week’s announcement of reciprocal tariffs. But it’s hard to draw firm conclusions yet, especially with quarter-end portfolio adjustments likely distorting some of the price action across assets.

In the broader currency markets, commodity currencies remain firmly in control. Aussie has taken over as the week’s leader, followed by Loonie and Kiwi. At the other end of the spectrum, Yen remains the weakest. Euro and Dollar are trailing just ahead of Yen, while Sterling and Swiss Franc sit in the middle of the performance board.

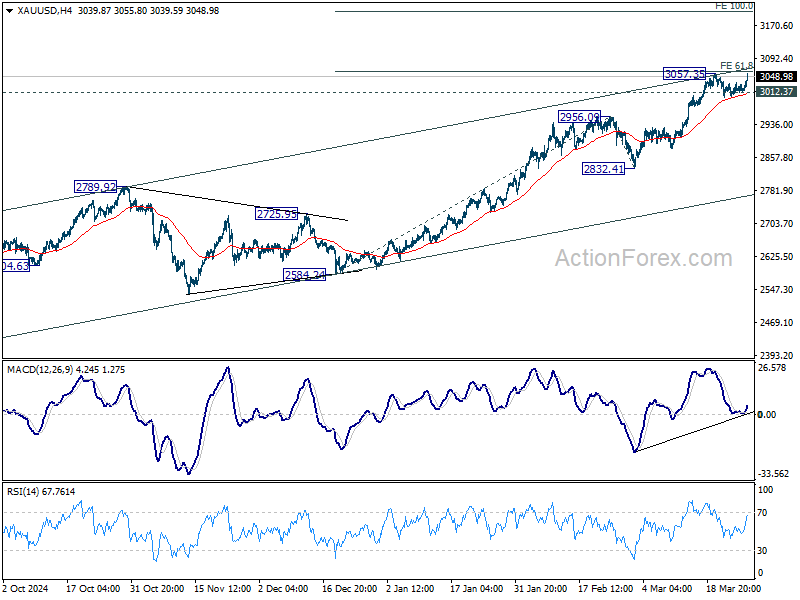

Technically, Gold is having a strong session, rebounding sharply as traders digest the latest trade rhetoric. Rise from 2832.31 might still have one more leg. But we’d maintain that upper channel resistance (now at around 3080) should post strong resistance to limit upside and bring correction. Break of 3012.37 support will bring deeper pull back to 2956.09 resistance turned support and below.

In Europe, at the time of writing, FTSE is down -0.84%. DAX is down -1.20%. CAC is down -0.72%. UK 10-year yield is up 0.058 at 4.791. Germany 10-year yield is down -0.026 at 2.774. Earlier in Asia, Nikkei fell -0.60%. Hong Kong HSI rose 0.41%. China Shanghai SSE rose 0.15%. Singapore Strait Times rose 0.45%. Japan 10-year JGB yield rose 0.005 to 1.592.

US initial jobless claims falls to 224k vs exp 225k

US initial jobless claims fell -1k to 224k in the week ending March 22, versus expectation of 225k. Four-week moving average of initial claims fell -5k to 224k. Continuing claims fell -25k to 1856k in the week ending March 15. Four-week moving average of continuing claims rose 2k to 1870k.

Also released, goods exports rose 4.1% mom to USD 178.6B, seasonally adjusted, in February. Goods imports fell -0.2% mom to USD 326.5B. Trade balance reported USD 147.9B deficit, larger than expectation of USD 134.6B.

Q4 GDP growth was finalized at 2.4% annualized. GDP price index was finalized at 2.3%.

ECB’s Wunsch: April rate pause should be on the table

Belgian ECB Governing Council member Pierre Wunsch suggested that pausing rate cuts in April should at least be “on the table”, and highlighted how tariff-induced stagflation poses a policy dilemma.

Wunsch warned that tariffs would complicate ECB’s path forward: “To the extent that tariffs will impact the economy … this will have an impact on our decision-making,” he noted.

While downplaying the immediate importance of April’s tariff development, Wunsch stressed that “It’s going to have an impact over the medium term.”

In contrast, Latvian Governing Council member Martins Kazaks suggested that if ECB’s baseline scenario holds, a “gradual reduction in rates in the future” could be expected.

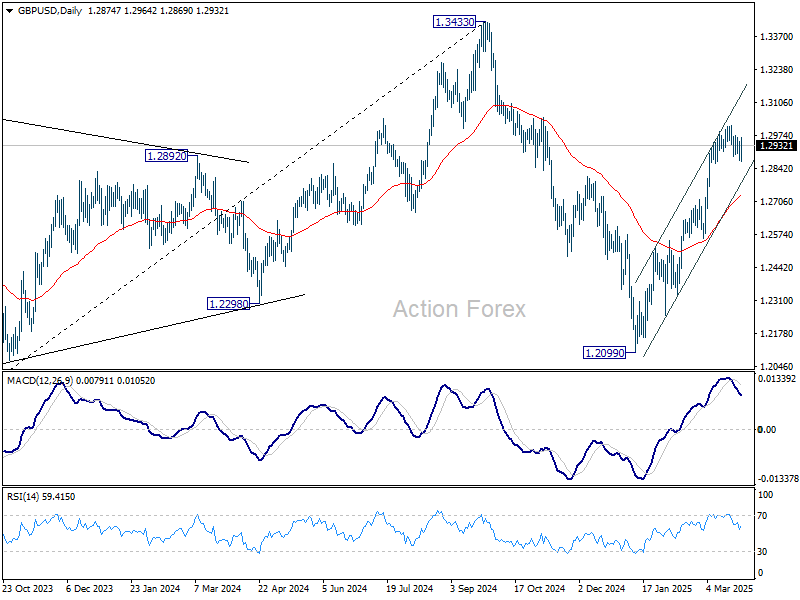

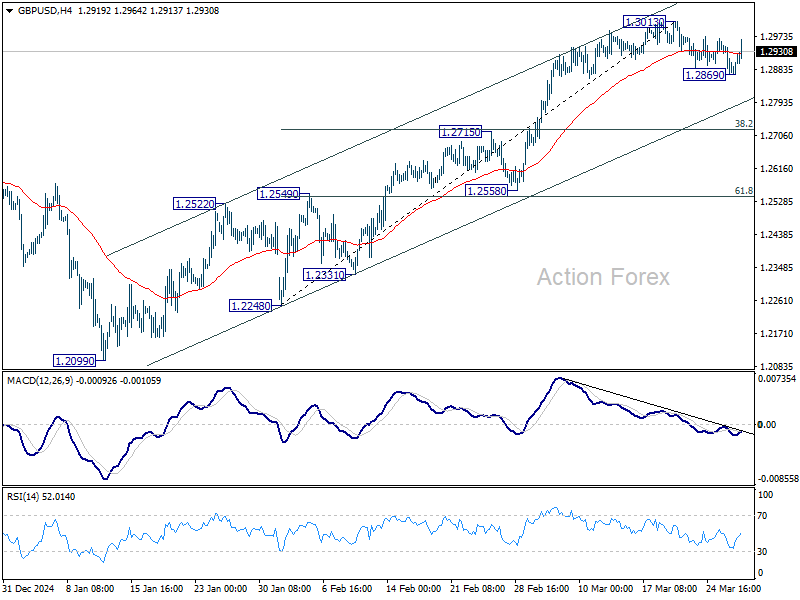

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2858; (P) 1.2905; (R1) 1.2935; More…

GBP/USD rebounded notably today but stays in range below 1.3013 short term top. Intraday bias remains neutral first. Corrective fall from 1.3013 could still extend lower to channel support (now at 1.2806). But downside should be contained by 38.2% retracement of 1.2248 to 1.3013 at 1.2721 to bring rebound. On the upside, break of 1.3013 will resume the rally from 1.2099.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.