{kind=link}

The steady drip of tariff news from US President Donald Trump continued overnight, pushing US equities lower and weighing on risk sentiment globally. The tech-heavy NASDAQ led the decline with a drop of over 2%, while broader US indexes also closed in the red. In Asia, Japan’s Nikkei and South Korea’s Kospi followed with notable declines—particularly in auto stocks—while other regional bourses stayed relatively steady, suggesting selective impact.

Despite the equity selloff, currency markets have shown muted reactions so far. Major FX pairs and crosses are treading water, largely trapped within yesterday’s ranges. This suggests that while traders are alert to the evolving trade policy, many are experiencing tariff fatigue and are reluctant to reposition aggressively before next week’s pivotal developments.

The latest tariff news centers around a 25% duty on imported cars and light trucks “not made in the United States,” scheduled to take effect on April 3. However, the rollout comes with key exemptions. Automotive parts compliant with USMCA are spared, and all other auto parts imports are exempt until May 3 to allow time for administrative clarity. It’s a classic case of shock softened by implementation ambiguity.

The centerpiece remains April 2, which Trump has dubbed “liberation day” and “the big one,” when reciprocal tariffs will be formally announced. However, in a shift of tone, Trump now says the measures will be “very lenient,” and “less than the tariff they’ve been charging (the US) for decades,” hinting at a softer-than-expected rollout. That may explain the relatively calm tone in FX markets despite the ongoing trade drama.

In terms of currency performance this week, Canadian Dollar is leading the charge along with commodity currencies. Aussie and Kiwi follow, while traditional safe havens like Yen and Dollar are under pressure. Euro joins them as one of the weakest, while Sterling and Swiss Franc are in the middle of the pack.

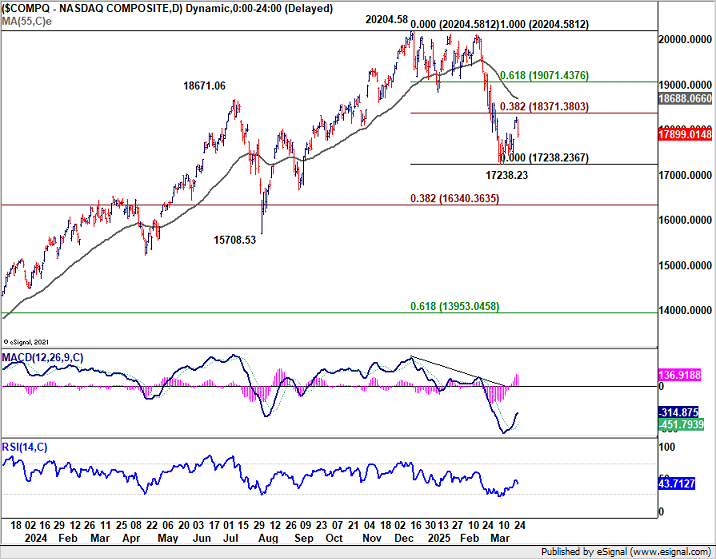

Technically, the selloff in NASDAQ overnight is just continuation of the near-term consolidation pattern from the 17238.23 low. Another bounce toward 38.2% retracement of 2024.58 to 17238.23 at 18371.38 remains possible. But strong resistance at the 55 D EMA (now at 18688.06) should cap upside. The larger correction from the 20204.58 peak is still expected to resume eventually, with a break below 17238.23 at a later stage.

In Asia, at the time of writing, Nikkei is down -0.97%. Hong Kong HSI is up 0.79%. China Shanghai SSE is up 0.23%. Singapore Strait Times is up 0.41%. Japan 10-year JGB yield is up 0.006 at 1.593, approaching 1.6% mark. Overnight, DOW fell -0.31%. S&P 500 fell -1.12%. NASDAQ fell -2.04%. 10-year yield rose 0.031 to 4.338.

Fed’s Musalem: Persistent tariff inflation could delay cuts or force hikes

St. Louis Fed President Alberto Musalem warned that while the initial effects of import tariffs may be short-lived, their broader inflationary impact could linger. He stressed concern that underlying inflation may be influenced more persistently than expected, and if so, Fed might have to consider a tighter policy stance.

Although this isn’t his baseline scenario, Musalem emphasized that the Fed must remain vigilant to second-round effects from tariffs.

He noted that if inflation stays above the 2% target and the economy remains strong, the current “modestly restrictive” monetary stance would need to be maintained longer.

More significantly, “If the labor market remains resilient and the second-round effects from tariffs become evident, or if medium- to longer-term inflation expectations begin to increase actual inflation or its persistence, then modestly restrictive policy will be appropriate for longer or a more restrictive policy may need to be considered,” he said.

BoC minutes: Rate cut driven by tariff threats, signals no guidance amid uncertainty

BoC’s March 12 Summary of Deliberations revealed that the decision to cut the policy rate by 25 bps to 2.75% was driven primarily by “tariff threats and elevated uncertainty”.

Governing Council members acknowledged that, under normal circumstances, holding the rate at 3% would have been appropriate. However, the impact of steel and aluminum tariffs, additional tariff threats, and the unpredictable stance of the US administration had begun to materially affect business and consumer decisions. This was “significantly weakening the near-term outlook”.

Looking ahead, BoC emphasized the complexity of the situation and the fluid nature of trade tensions. “It would not be appropriate to provide guidance on the future path for the policy interest rate,” the minutes noted.

Looking ahead

Eurozone M3 money supply is the only feature in European session. Later in the day, US will release Q1 GDP final, goods trade balance, jobless claims and pending home sales.

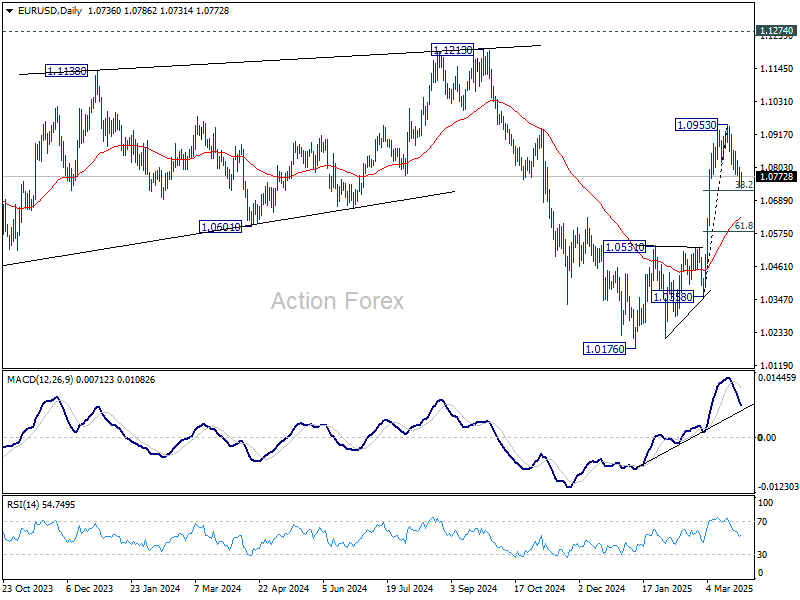

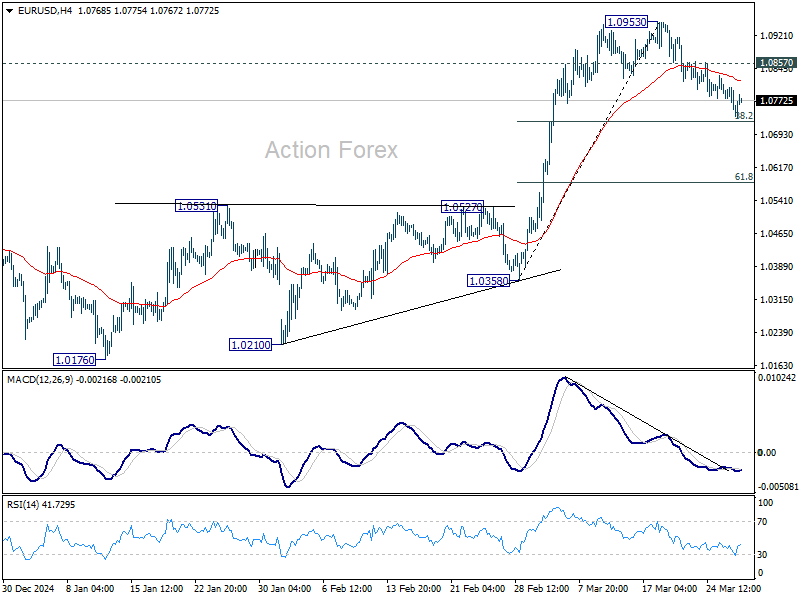

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0729; (P) 1.0767; (R1) 1.0789; More…

Outlook in EUR/USD is unchanged that strong support is expected from 38.2% retracement of 1.0358 to 1.0953 at 1.0726 to completion the correction from 1.0953. On the upside, break of 1.0857 will bring retest of 1.0953 first. Firm break there will resume larger rise from 1.0176. However, sustained break of 1.0726 will bring deeper correction to 55 D EMA (now at 1.0630).

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.