{kind=link}

Commodity currencies are finding a bid in Asian session today, though still largely range-bound against Dollar. A sharp rally in Copper prices, driven by US tariff fears, is likely giving Aussie a tailwind, countering lingering drag from today’s slightly weaker-than-expected inflation data. Meanwhile, Loonie is benefitting from speculation that Canada may be assigned lower tariffs under US President Donald Trump’s upcoming global trade measures.

According to a Toronto Star report, the Trump administration is preparing a tiered structure for its reciprocal tariffs, grouping trading partners into low, medium, and high tariff categories. Though details remain vague, sources suggest that Canada could be in the “low” tier—but with a twist: tariffs may be cumulative across sectors. The lack of clarity on what qualifies as “high” is keeping markets on edge too, with figures ranging from 25% to triple digits being floated.

Despite the moves in FX, the broader market isn’t displaying strong risk-on conviction. Yen and Swiss Franc are both under pressure—typically a signal of risk appetite—but equities have yet to respond in kind. Yen, in particular, is back as the day’s worst performer, following a recovery yesterday. The lack of follow-through in stocks suggests traders remain hesitant ahead of next week’s highly anticipated “Liberation Day” tariffs announcement on April 2.

In Europe, UK CPI data will be the key focus today. Barring any dramatic surprises, the figures should support BoE’s current stance of slow, measured easing, with rate cuts expected once per quarter. That likely caps any Sterling upside for now, even as traders shift focus toward Euro and GBP cross flows for near-term positioning.

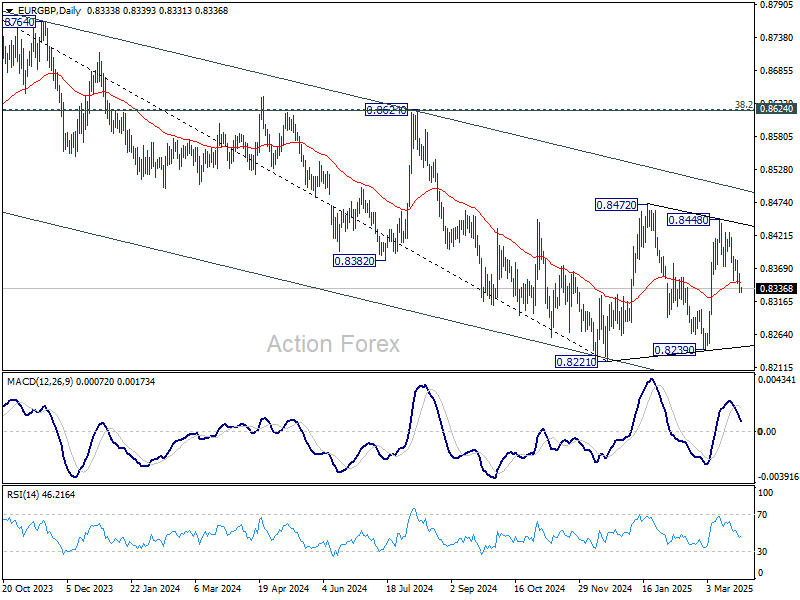

Technically, EUR/GBP’s break of 55 D EMA now argues that rebound from 0.8239 has completed at 0.8448 already, as a leg inside the sideway pattern from 0.8221. Deeper fall would be mildly in favor back to 0.8239 support next.

In Asia, at the time of writing, Nikkei is up 1.02%. Hong Kong HSI is up 0.25%. China Shanghai SSE is up 0.02%. Singapore Strait Times is up 0.36%. Japan 10-year JGB yield is up 0.014 at 1.587. Overnight, DOW rose 0.01%. S&P 500 rose 0.16%. NASDAQ rose 0.46%. 10-year yield fell -0.024 to 4.307.

Fed’s Goolsbee sees surging inflation expectations as a red flag

Chicago Fed President Austan Goolsbee warned that a shift in market-based long-run inflation expectations toward the elevated levels seen in consumer surveys, such as the University of Michigan’s, would be a “major red flag” demanding immediate Fed attention.

He emphasized that if investor sentiment converges with households’ expectations, now at the highest since 1993, Fed would have little choice but to respond.

Goolsbee noted that Fed has moved into “a different chapter” marked by heightened uncertainty, contrasting with the “golden path” of 2023 and 2024, when inflation eased without damaging growth or jobs.

While he still sees interest rates being “a fair bit lower” in the next 12–18 months, he acknowledged that economic unpredictability, particularly surrounding trade policy, may delay Fed’s next move. His stance: “wait and see is the correct approach,” though not without costs.

In conversations with business leaders, Goolsbee said April 2—the date of expected US tariff announcements—has become a key flashpoint of anxiety. This uncertainty, he said, is fueling a broad hesitancy in investment and hiring decisions across the Fed district.

BoJ’s Ueda: Vigilant on upside inflation risks, signals readiness for stronger action

BoJ Governor Kazuo Ueda emphasized today that the central bank remains “vigilant” to upside surprises in “underlying inflation.

While recent “very high” inflation has been driven largely by temporary factors like import costs and food prices, there’s still a possibility that underlying inflation could accelerate more quickly than expected.

Ueda warned that if such “broad-based inflation” materializes, BoJ would need to respond by raising interest rates and even take “stronger steps”.

However, for now, he reaffirmed the view that underlying inflation remains “just a bit” short of the 2% target, though it is on track to gradually converge to that level.

Meanwhile, data released today showed Japan’s services producer price index rose 3.0% yoy in February, a deceleration from January’s 3.2% and below expectations of 3.1%.

Australia CPI slows to 2.4% in Feb, trimmed mean ticks down to 2.7%

Australia’s monthly CPI eased to 2.4% yoy in February, slightly below expectations of 2.5% yoy and marking a step down from the steady 2.5% yoy pace seen over the past two months.

Core inflation measures also softened, with the trimmed mean slipping from 2.8% yoy to 2.7% yoy. CPI excluding volatile items and holiday travel eased from 2.9% yoy to 2.7% yoy.

The largest contributors to annual inflation were food and non-alcoholic beverages (+3.1%), alcohol and tobacco (+6.7%), and housing (+1.8%).

Still, the overall slowdown adds to the case for RBA to remain on hold at its upcoming meeting. The central bank has made it clear that February’s rate cut does not set an automatic path for further easing. With the more comprehensive Q1 CPI data still to come, today’s numbers are unlikely to shift policy expectations in a meaningful way.

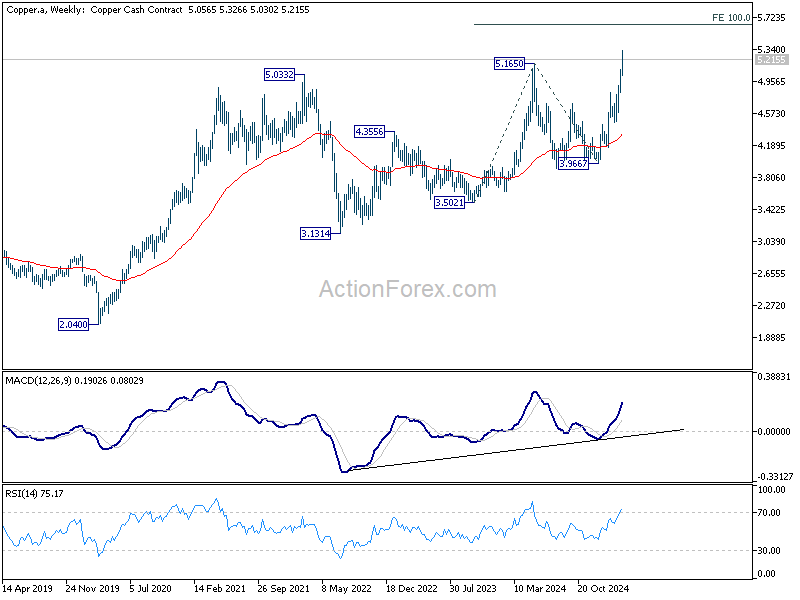

Tariff fears drive Copper to record in classic commodity fifth-wave extension

US Copper prices surged to fresh record highs, driven by rising expectations that President Donald Trump may soon impose tariffs on copper imports.

Traders are responding to signals that the Commerce Department’s review—ordered by Trump in February—is advancing quickly, and that a decision, possibly imposing tariffs of up to 25%, could be announced within weeks.

The surge reflects not only speculative buying but also a defensive scramble as traders and manufacturers brace for supply disruptions. A key driver of the move is fear, with the current rally taking the form of a classic fifth-wave extension seen in commodity markets—when panic buying exacerbates already tight conditions.

Technically, the uptrend from January low at 3.9667 is now in its final leg of a five-wave sequence. While there may still be some upside left, strong resistance lies ahead.

Despite the bullish momentum, Copper should soon face strong resistance soon. Two key projection levels—5.538 (161.8% of the 4.1568 to 4.8168 move from 4.4702) and 5.6298 (100% projection of 3.5021 to 5.1650 from 3.9667)—form a crucial zone that should cap the rally.

Looking ahead

UK CPI is the main focus in European session while Swiss will release UBS economic expectations. Later in the day, US durable goods orders will be published. BoC will release summary of deliberations.

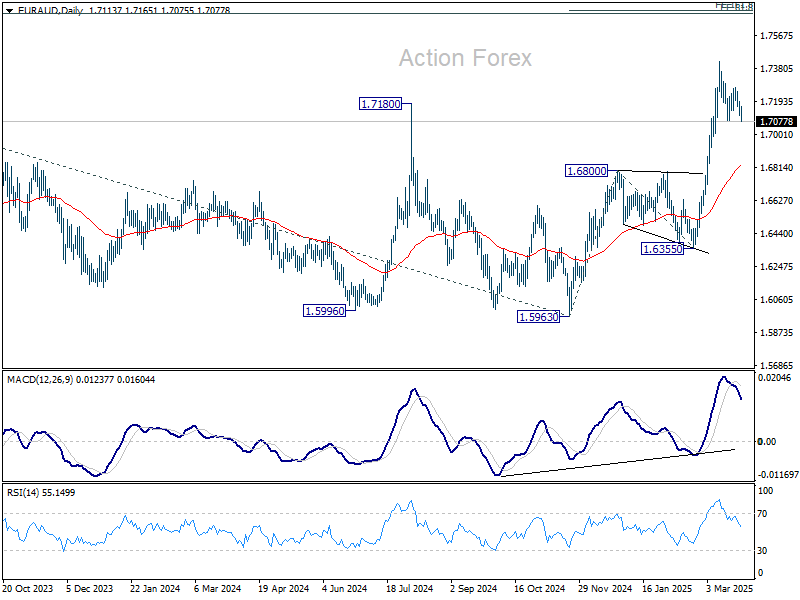

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7092; (P) 1.7143; (R1) 1.7173; More…

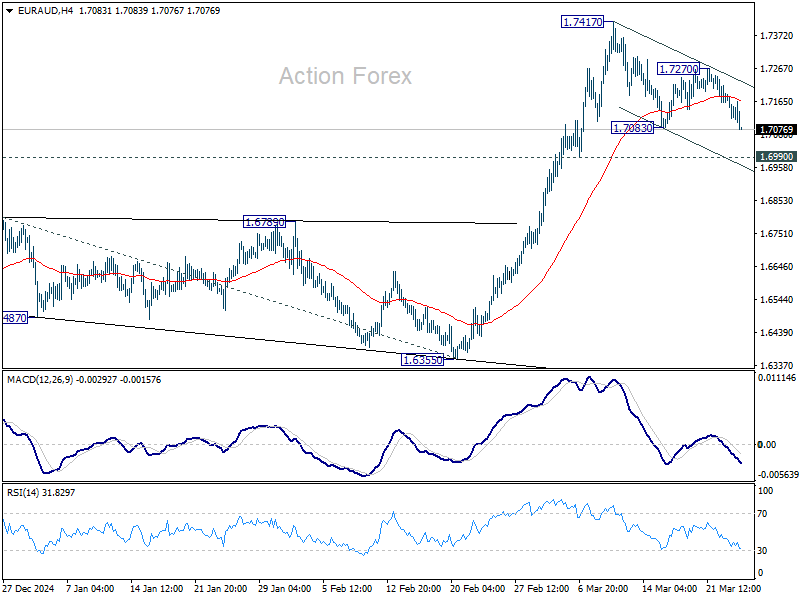

EUR/AUD’s corrective fall from 1.7417 short term top is resuming and intraday bias is mildly on the downside. Still, downside of the pullback should be contained by 0.6990 support to bring rebound. On the upside, above 1.7270 will bring retest of 1.7417 first. Break there will resume rise from 1.6335 to 161.8% projection of 1.5963 to 1.6800 from 1.6355 at 1.7709 next.

In the bigger picture, the breach of 1.7180 key resistance (2024 high) suggests that up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 will confirm and target 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6800 resistance turned support holds, even in case of deep pullback.