{kind=link}

Canadian Dollar weakened modestly in early US session following disappointing retail sales data. January’s figures showed a larger-than-contraction, and more importantly, an advance estimate points to another drop in February. This suggests consumer spending might be in a weakening trend, raising fresh concerns about Canada’s economic momentum heading into Q2.

However, the selloff in the Loonie has been relatively limited so far. BoC Governor Tiff Macklem’s comments from Thursday may have offered some cushion. Macklem warned against allowing initial price spikes from tariffs to morph into broader inflationary pressures, highlighting the need for vigilance in monetary policy. This has fueled market speculation that BoC may pause its rate cutting cycle in April to better assess tariff impacts and inflation risks.

Meanwhile, Euro is coming under some pressure along with Germany’s DAX index, despite a historic win for the country’s fiscal policy. Germany’s Bundesrat passed a major spending package aimed at reviving growth and bolstering defense. However, traders seem to be locking in profits after weeks of rallying on anticipation of this very outcome, suggesting the news may have been fully priced in.

For the week so far, Swiss Franc is now the top performer, followed by Kiwi and then Loonie. Aussie lags at the bottom, trailed by Euro and Yen. Dollar and Pound are stuck in the middle of the pack.

Canadian retail sales down -0.6% mom in Jan, more contraction in Feb

Canada’s retail sales dropped -0.6% mom to CAD 69.4B in January, marking a steeper-than-expected decline and signaling subdued consumer spending.

The largest drag came from motor vehicle and parts dealers, while overall sales fell in three of nine subsectors.

Core retail sales, which strip out gasoline and auto-related purchases, also slipped -0.2%.

Adding to the concern, Statistics Canada’s advance estimate suggests retail sales fell another -0.4% in February.

Japan’s CPI core slows less than expected to 3% in Feb

Japan’s core consumer inflation eased for the first time in four months in February, but less than market expectations. While the data strengthens the case for another BoJ rate hike at the April 30–May 1 meeting, policymakers may still choose to wait until July to better assess the impact of US tariff escalation and broader global financial market risks.

CPI core (excluding fresh food) slowed from 3.2% yoy to 3.0% yoy, slightly above expectations of 2.9%. The moderation was partly due to the resumption of government subsidies on utility bills. Despite this, core inflation has stayed above BoJ’s 2% target since April 2022.

More significantly, core-core CPI (excluding food and energy) rose from 2.5% yoy to 2.6% yoy, marking the fastest pace since March 2024. This continued strength in underlying inflation, even as services inflation softened slightly from 1.4% yoy to 1.3% yoy, reflects steady pass-through of higher labor costs.

Meanwhile, headline CPI slowed from 4.0% yoy to 3.7% yoy.

New Zealand posts NZD 510m trade surplus as exports surge across key markets

New Zealand posted a surprise trade surplus of NZD 510m in February, defying expectations of a NZD -235m deficit.

Goods exports jumped 16% yoy to NZD 6.7B, led by strong demand from key trading partners including China, Australia, and the EU. Notably, exports to China surged by 16% yoy, while shipments to Australia and the EU rose by 17% yoy and 37% yoy, respectively. The only major decline was seen in exports to the US, which slipped by -5.5% yoy.

Goods imports edged up a modest 2.1% yoy to NZD 6.2B, with notable volatility in country-level data. Imports from the US spiked 41% yoy, while those from South Korea plunged -57% yoy. Imports from Australia (-9.3% yoy) and the EU (-3.3% yoy)also declined. Despite the pickup from the US and China (3.8% yoy), subdued import figures from other regions helped tilt the trade balance into surplus.

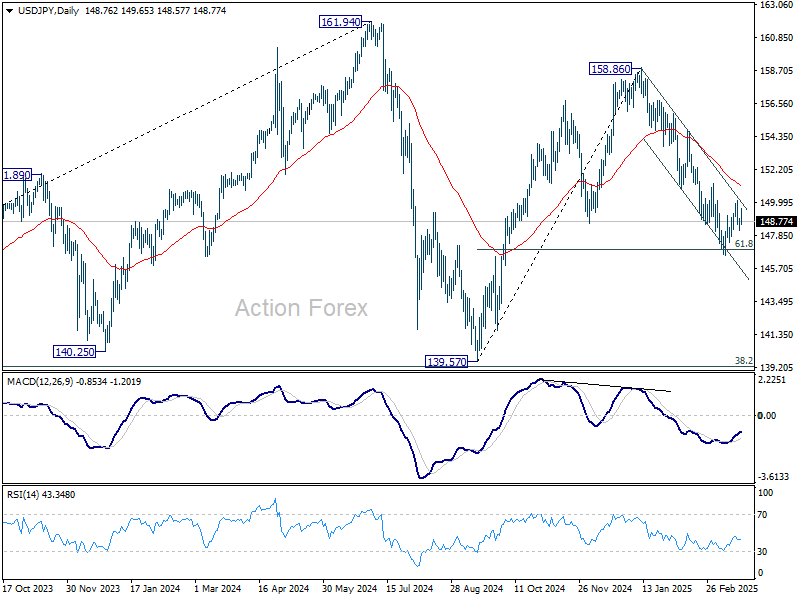

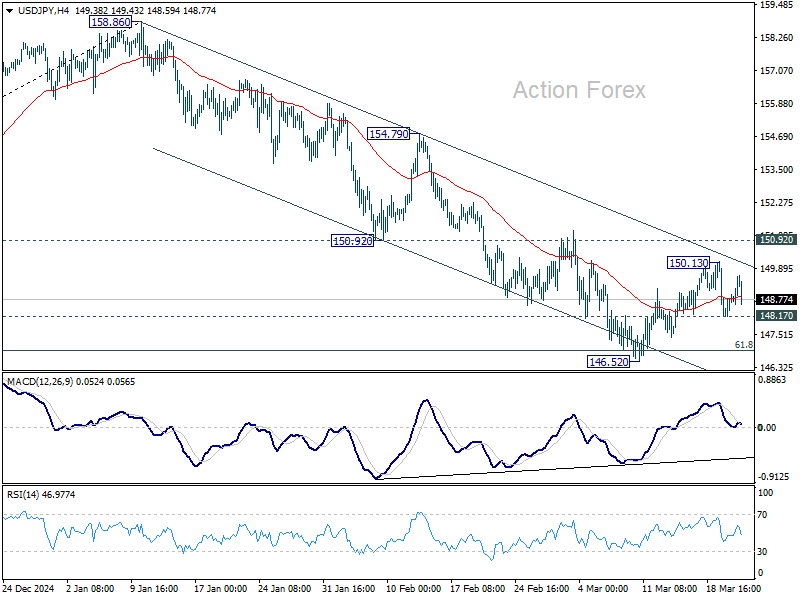

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.32; (P) 148.64; (R1) 149.10; More…

Intraday bias in USD/JPY remains neutral and outlook is unchanged. Corrective pattern from 146.52 might extend. But in case of stronger recovery, upside should be limited by 150.92 support turned resistance. On the downside, firm break of 148.17 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.