{kind=link}

Dollar continues to grapple with reversing its recent bearish trend, but momentum behind the rebound remains tentative at best. The greenback has received modest support from Fed’s stance, with policymakers emphasizing there’s no urgency to resume rate cuts. This, combined with a general reassessment of earlier bearish bets, has helped slow the pace of decline in Dollar, even as sentiment remains cautious.

One of the key themes driving recent market behavior has been the ongoing trade war narrative. Despite rising concerns about a recession in the US triggered by escalating tariffs, those fears have yet to materialize in hard data. Even Fed Chair Jerome Powell maintained a relatively balanced tone in this week’s FOMC press conference, holding back from sounding overly pessimistic. Traders may now be stepping back from aggressive short positions, waiting for more clarity—particularly around the reciprocal tariffs due in early April.

Looking across the currency markets, Yen is the worst performer so far this week, gaining little traction even after stronger-than-expected inflation data from Japan. Aussie follows, pressured by disappointing jobs data, while the Euro is beginning to consolidate gains following renewed optimism over the EU’s large-scale fiscal expansion plans. On the flip side, the Canadian Dollar surprisingly leads, despite Canada’s exposure to US tariffs, with Swiss Franc and Kiwi following Dollar and Sterling are relatively mixed, occupying the middle of the pack.

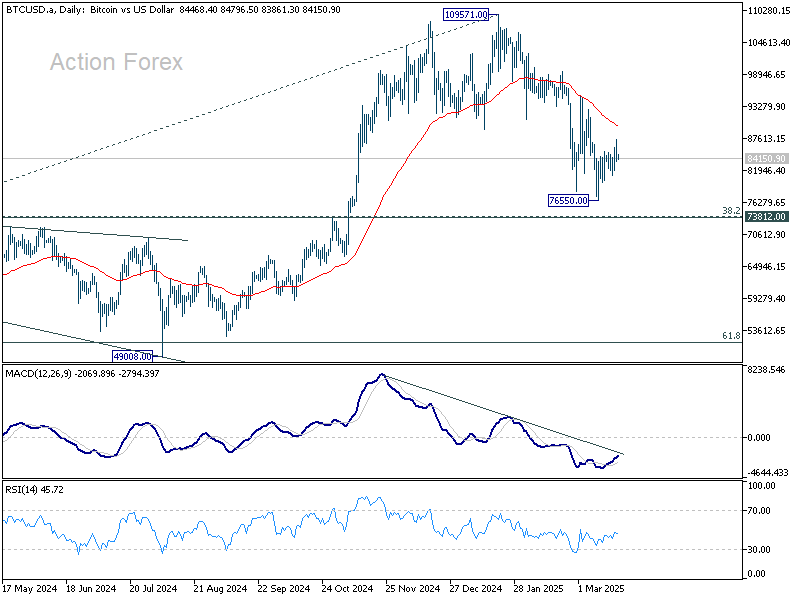

Meanwhile, Bitcoin’s recovery is showing signs of fatigue after hitting 87462 earlier in the week. President Donald Trump’s bold declaration that the US will become the global “undisputed Bitcoin superpower” at a recent crypto conference failed to spark meaningful market response. Despite the rhetoric, traders seem more focused on underlying technical and macroeconomic factors than political promises.

Nevertheless, technically, Bitcoin is still holding firmly above 73812 cluster support (38.2% retracement of 15452 to 109571 at 73617. The choppy decline from 109571 is viewed as a correction only. Firm break of 55 D EMA (now at 89980) will argue that the pullback has already completed, and bring stronger rebound back to retest 109571 high.

In Asia, Nikkei fell -0.20%. Hong Kong HSI is down -2.06%. China Shanghai SSE is down -1.29%. Singapore Strait Times is down -0.08%. Japan 10-year JGB yield fell -0.004 to 1.527. Overnight, DOW fell -0.03%. S&P 500 fell -0.22%. NASDAQ fell -0.33%. 10-year yield fell -0.023 to 4.233.

Japan’s CPI core slows less than expected to 3% in Feb

Japan’s core consumer inflation eased for the first time in four months in February, but less than market expectations. While the data strengthens the case for another BoJ rate hike at the April 30–May 1 meeting, policymakers may still choose to wait until July to better assess the impact of US tariff escalation and broader global financial market risks.

CPI core (excluding fresh food) slowed from 3.2% yoy to 3.0% yoy, slightly above expectations of 2.9%. The moderation was partly due to the resumption of government subsidies on utility bills. Despite this, core inflation has stayed above BoJ’s 2% target since April 2022.

More significantly, core-core CPI (excluding food and energy) rose from 2.5% yoy to 2.6% yoy, marking the fastest pace since March 2024. This continued strength in underlying inflation, even as services inflation softened slightly from 1.4% yoy to 1.3% yoy, reflects steady pass-through of higher labor costs.

Meanwhile, headline CPI slowed from 4.0% yoy to 3.7% yoy.

New Zealand posts NZD 510m trade surplus as exports surge across key markets

New Zealand posted a surprise trade surplus of NZD 510m in February, defying expectations of a NZD -235m deficit.

Goods exports jumped 16% yoy to NZD 6.7B, led by strong demand from key trading partners including China, Australia, and the EU. Notably, exports to China surged by 16% yoy, while shipments to Australia and the EU rose by 17% yoy and 37% yoy, respectively. The only major decline was seen in exports to the US, which slipped by -5.5% yoy.

Goods imports edged up a modest 2.1% yoy to NZD 6.2B, with notable volatility in country-level data. Imports from the US spiked 41% yoy, while those from South Korea plunged -57% yoy. Imports from Australia (-9.3% yoy) and the EU (-3.3% yoy)also declined. Despite the pickup from the US and China (3.8% yoy), subdued import figures from other regions helped tilt the trade balance into surplus.

BoC Governor: Crucial to Stop Initial Tariff Price Shocks from Becoming Generalized Inflation

Bank of Canada Governor Tiff Macklem issued a stark warning on the economic consequences of prolonged US tariffs, emphasizing that broad-based and long-lasting trade barriers will depress Canadian exports, reduce overall output, and push consumer prices higher.

In a speech overnight, Macklem noted that the unpredictability of US tariffs, marked by “constant policy reversals”, has injected significant uncertainty into the outlook for Canadian businesses and households.

Macklem highlighted two major areas of concern: uncertainty about which tariffs will be imposed and for how long, and uncertainty about their economic impact.

Already, the BoC has observed that businesses are cutting back investment and hiring, and many households are growing more cautious with spending. He warned that if broad-based tariffs remain in place, the result will be “less demand, less economic growth and higher inflation”.

While monetary policy cannot prevent the initial rise in prices caused by tariffs, Macklem stressed that it must act to “prevent those initial, direct price increases from spreading”.

“We must ensure that higher prices from tariffs do not become ongoing generalized inflation,” he emphasized.

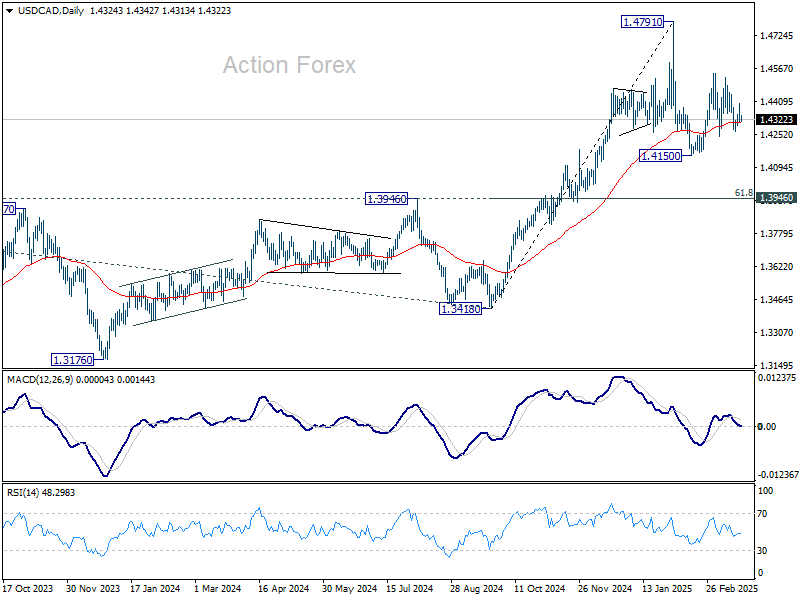

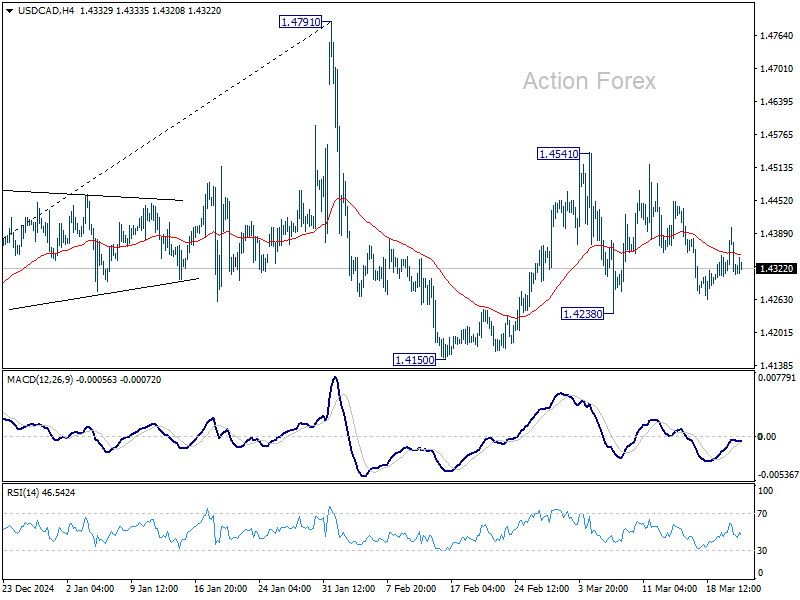

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4290; (P) 1.4346; (R1) 1.4379; More…

Intraday bias in USD/CAD remains neutral as range trading continues. On the downside, break of 1.4238 support will argue that corrective pattern from 1.4791 has started the third leg already. Intraday bias will be back on the downside for 1.4150 support and below. On the upside, though, break of 1.4541 will resume the rebound from 1.4150, as the second leg of the pattern.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.