{kind=link}

Forex markets are trading with a mild risk-off tone in a relatively quiet day so far, with many Asian markets closed for Lunar New Year holiday. Safe-haven currencies, including Yen, Swiss Franc, and Dollar, are holding firm, while commodity-linked currencies are on the weaker side. However, there is little follow-through momentum, with traders hesitant to make significant moves for now. The AI-driven tech rout that dominated sentiment earlier in the week appears to have faded from traders’ focus, with attention squarely on Fed and BoC policy updates.

In Asia Pacific, expectations for an RBA rate cut in February have strengthened following weaker-than-expected Q4 CPI data. Westpac’s Chief Economist Luci Ellis emphasized that trimmed mean inflation data suggests disinflation is advancing more quickly than anticipated, which should give RBA confidence to start cutting rates. CBA’s Head of Australian Economics, Gareth Aird, echoed this view, calling the latest figures a “green light” for policy normalization. While Australian Dollar weakened in response to the data, there has been no sharp acceleration in selling pressure, indicating that markets had already priced in the likelihood of the dovish shift.

BoC is widely expected to cut rates by 25bps today, lowering the policy rate to 3.00%. As rates enter deeper into the estimated neutral range of 2.25–3.25%, policymakers will likely take a more cautious approach moving forward. Adding to the uncertainty is the risks of trade conflict with the US, which could complicate BoC’s policy outlook. Traders will pay close attention to Governor Tiff Macklem’s assessment of economic risks, particularly how the central bank plans to balance easing monetary policy with external uncertainties.

Meanwhile, FOMC is expected to hold rates steady at 4.25–4.50%. The main focus will be on whether Fed signals an extended pause in its rate-cutting cycle, either in its statement or through Chair Jerome Powell’s press conference. Market pricing currently assigns a 67.6% probability of a hold in March and a 49.3% chance in May, with expectations for the next rate cut rising to 75% in June. Powell’s tone will be critical in either reinforcing or reshaping these expectations, with any hawkish signals likely to support the Dollar, while a dovish stance could provide room for further risk-on sentiment.

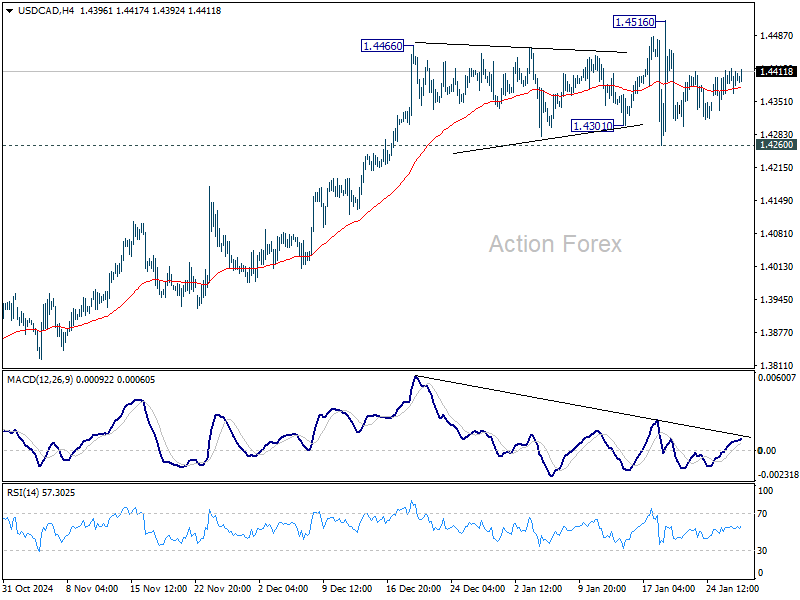

Technically, USD/CAD remains within range between 1.4260 and 1.4516. While the broader outlook remains bullish as long as 1.4260 holds as support, an immediate breakout appears unlikely unless today’s policy announcements deliver a significant surprise. A clearer directional move may only emerge once the tariff situation between the US and Canada is clarified, which remains a key source of uncertainty for the pair.

For the week so far, risk aversion continues to dominate, though without significant intensification. Yen remains the strongest performer, followed by Swiss Franc and Dollar. Aussie continues to struggle at the bottom, followed by Kiwi and then Euro. Sterling and Loonie are positioning in the middle.

German Gfk consumer sentiment falls to -22.4, recovery hopes fade

Germany’s GfK Consumer Sentiment Index for February fell to -22.4, down from -21.4 and missing expectations of -20.5.

In January, economic expectations dropped by 1.9 points to -1.6, while income expectations declined by 2.5 points to -1.1. The most concerning development came from willingness to buy, which fell 3 points to -8.4, its lowest level since August 2024,.

Rolf Bürkl, consumer expert at NIM, noted that “the Consumer Climate has suffered another setback and starts gloomy into the new year.”

The moderate optimism seen in late 2024 has faded, with Bürkl adding that the trend since mid-2024 has been stagnation at best. A key concern is inflation, which has recently picked up again, limiting prospects for a meaningful rebound in consumer demand.

Australia’s CPI slows to 2.4% in Q4, trimmed mean CPI down to 3.2%

Australia’s Q4 CPI rose just 0.2% qoq, same as the prior quarter, falling short of expectations of 0.4% yoy. Trimmed mean CPI also undershot forecasts, rising 0.5% qoq versus the expected 0.6% qoq.

On an annual basis, headline CPI slowed from 2.8% yoy to 2.4% yoy, slightly below 2.5% yoy consensus. Trimmed mean CPI fell from 3.6% yoy to 3.2% yoy, missing 3.3% yoy estimate.

These weaker inflation prints reinforce expectations that RBA may begin easing policy as early as its February 17-18 meeting.

The decline in annual inflation was largely driven by steep drops in electricity prices (-25.2%) and automotive fuel (-7.9%). Goods inflation slowed sharply to 0.8% yoy, down from 1.4% yoy in Q3. Meanwhile, services inflation remained elevated at 4.3% yoy, though slightly lower than the 4.6% yoy in the previous quarter.

In December, monthly CPI rebounded from 2.3% yoy to 2.5% yoy, matched expectations.

RBNZ’s Conway sees cautious OCR path to neutral

RBNZ Chief Economist Paul Conway stated in a speech today that Official Cash Rate at 4.25% remains “north of neutral”. The central bank estimates the neutral rate between 2.5% and 3.5%.

“Easing domestic pricing intentions and the recent drop in inflation expectations help open the way for some further easing,” Conway added.

However, Conway emphasized a cautious approach, noting that policymakers will “feel our way” as rates approach neutral. RBNZ will continuously reassess its neutral rate estimate, adjusting based on economic conditions.

If neutral is underestimated, stronger-than-expected activity and inflation would signal a less restrictive policy than intended, prompting recalibration, he added.

The central bank expects potential output growth to range between 1.5% and 2% annually over the next three years, reflecting a lower economic “speed limit.” This weaker outlook stems from sluggish productivity and reduced net immigration, limiting long-term economic capacity.

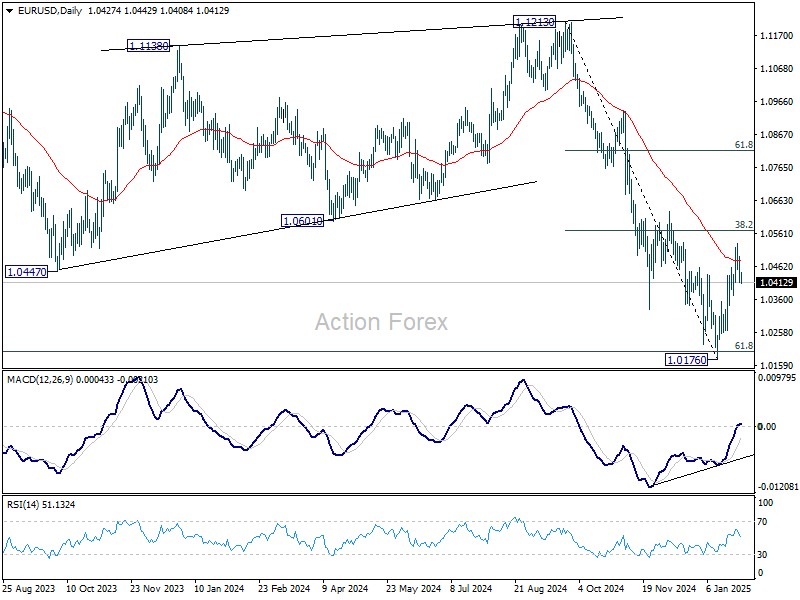

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0398; (P) 1.0447; (R1) 1.0480; More…

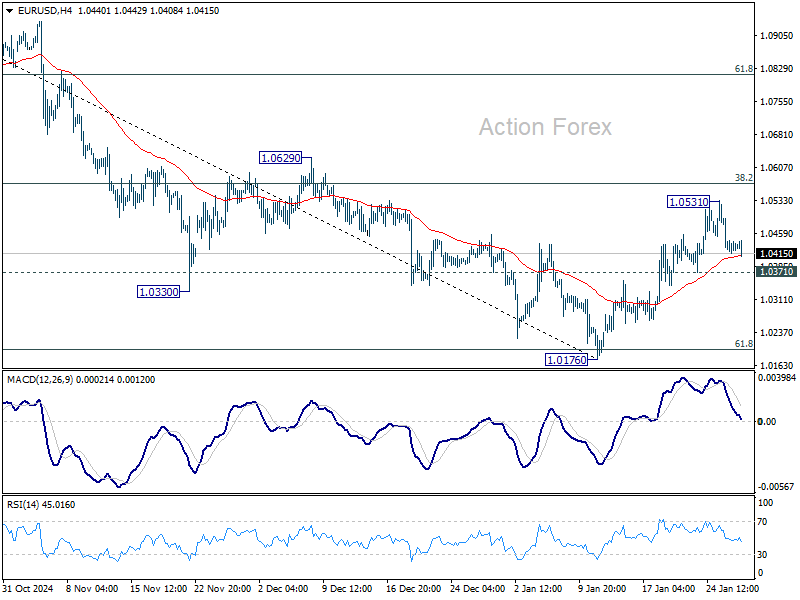

Intraday bias in EUR/USD stays neutral and outlook is unchanged. On the downside, break of 1.0371 support will indicate rejection by 38.2% retracement of 1.1213 to 1.0176 at 1.0572 and retain near term bearishness. Retest of 1.0176 low should be seen next. On the upside, though, decisive break of 1.0572 will raise the chance of bullish reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, outlook is mixed as fall from 1.1274 (2023 high) could either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. Strong support from 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will favor the former case, and sustained break of 55 W EMA (now at 1.0722) will argue that the third leg might have started. However, sustained trading below 1.0199 will favor the latter case and bring retest of 0.9534 low.