{kind=link}

Dollar’s decline accelerated as the week progressed towards the last day, weighed down by strong risk-on sentiment and investor optimism. S&P 500 closed at a new record high on Thursday, with NASDAQ and DOW poised to follow soon.

Contributing to this sentiment were remarks from US President Donald Trump at the World Economic Forum, where he linked falling oil prices to a demand for lower interest rates. However, analysts widely believe the Fed will maintain its independence, with no immediate response to such rhetoric. Fed fund futures currently show a 99.5% likelihood of a hold at next week’s meeting, while the probability of a May rate cut stands at 50%. Expectations for a second cut by year-end, nevertheless, have risen slightly to 55%.

Another boost to market sentiment came from signals of potential improvement in US-China relations. In a Fox News interview, Trump expressed a preference for resolving trade disputes without resorting to tariffs, saying, “I’d rather not have to use [tariffs],” while acknowledging their leverage over Beijing. In the background, Trump granted a 75-day reprieve to TikTok earlier in the week, suggesting flexibility in implementing a law requiring the divestiture of its US business.

All these gestures indicated a much softer tone from the White House, comparing to Trump’s election rhetoric, and raised hopes for renewed negotiations with China. These developments reinforced investor confidence and tempered fears of immediate tariff escalations, contributing to the broader risk-on mood.

Currency markets reflect this shifting sentiment. Dollar is now the weakest performer of the week, pressured by strong risk appetite and fading concerns over immediate trade tensions. Yen follows as the second-worst performer, despite some recovery after BoJ’s rate hike today. Loonie rounds out the bottom three. Meanwhile, Kiwi and Aussie are the week’s strongest currencies, buoyed by the global risk-on mood, with Euro also gaining ground. Pound and Swiss Franc remain mixed in middle positions.

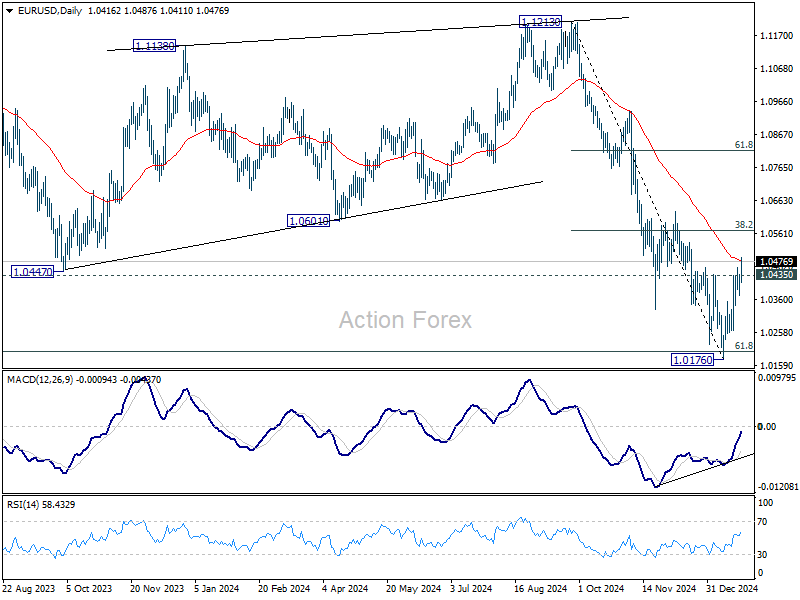

Technically, EUR/USD’s break of 1.0435 resistance suggests that it’s correcting the whole fall from 1.1213 to 1.0176. Further rise should be seen to 38.2% retracement of 1.1213 to 1.0176 at 1.0572. Strong resistance should be seen there to limit upside, at least on first attempt. However, decisive break of 1.0572 will raise the chance of bullish trend reversal.

BoJ delivers expected rate hike, upgrades core inflation forecasts

BoJ raised its uncollateralized overnight call rate by 25bps to 0.50% as widely expected, marking the highest level since 2008. The decision, made by an 8-1 vote, saw dissent from board member Nakamura Toyoaki, who advocated for a delay until March.

In the new economic projections, core CPI forecasts were significantly revised upward from 1.9% to 2.4% for fiscal 2025, and slightly from 1.9% to 2.0% for fiscal 2026. Core-core CPI (excluding energy and fresh food) forecast was also raised from 1.9% to 2.1% for fiscal 2025, remaining unchanged at 2.1% for fiscal 2026. Real GDP growth projections were left steady at 1.1% for fiscal 2025 and 1.0% for fiscal 2026.

At the post-meeting press conference, Governor Kazuo Ueda downplayed the sharp inflation forecast revisions, stating, “The rise in underlying inflation is moderate. I don’t think we are seriously behind the curve in dealing with inflation.”

He reiterated the importance of a gradual approach to policy adjustments, and there no “preset idea” on the timing and pace of rate hikes. He also highlighted the estimated neutral range of 1%-2.5%, emphasizing that the current rate of 0.5% still has “some distance” to reach neutral.

Also released, CPI core (ex-food) jumped from 2.7% yoy to 3.0% yoy in December, marking the highest rate in 16 months. CPI core-core (ex-food & energy) was unchanged at 2.4% yoy. Headline CPI rose from 2.9% yoy to 3.6% yoy.

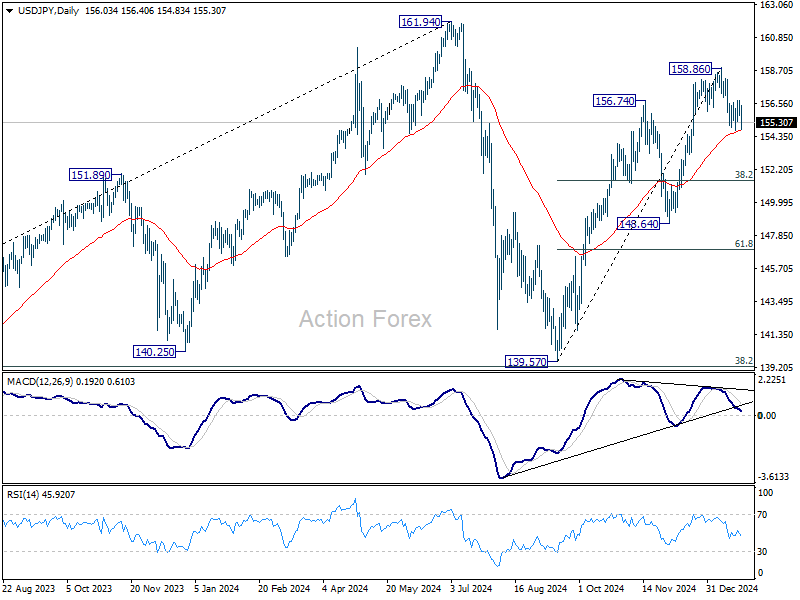

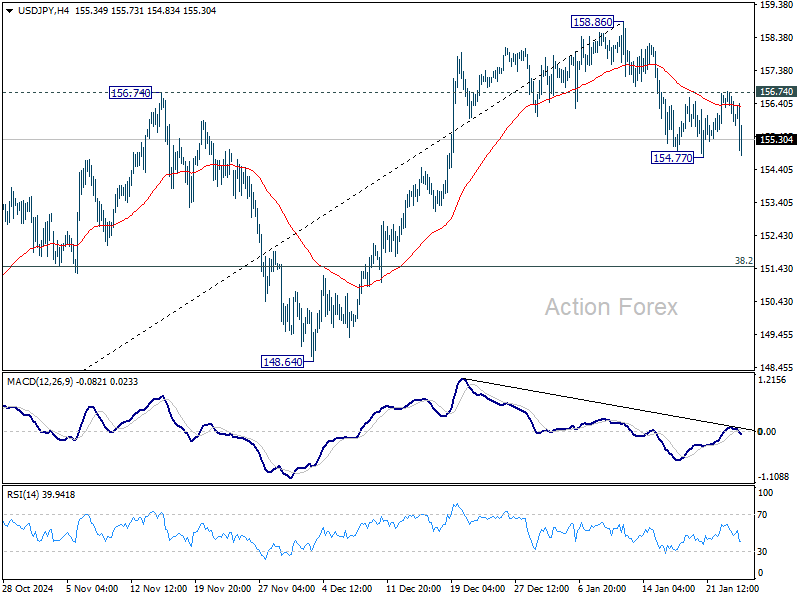

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.59; (P) 156.23; (R1) 156.71; More…

USD/JPY’s is staying above 154.77 temporary low despite today’s dip, and intraday bias remains neutral. Further decline remains in favor for now. Sustained trading below 55 D EMA (now at 154.73) will extend the correction from 158.86 to 38.2% retracement of 139.57 to 158.86 at 151.49 next. On the upside, though, above 156.74 minor resistance will bring retest of 158.86 instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.