{kind=link}

Sterling’s selloff continues today as UK government bond yields surged to new highs, underlining deep market concerns over the nation’s fiscal outlook. 10-year Gilt yield breached 4.8%, a level not seen in 17 years, while 30-year yield climbed past 5.4%, marking its highest point in 27 years.

At the core of this crisis are doubts about the government’s ability to meet its fiscal targets without resorting to higher taxes or additional spending cuts. Prime Minister Keir Starmer reaffirmed his commitment to the government’s fiscal rules, but his sidestepping of questions about austerity measures did little to calm investor nerves.

Meanwhile, Chancellor Rachel Reeves is facing scrutiny for her economic strategies—although Starmer offered unwavering support, calling her performance “fantastic.” Traders appear unconvinced, with concerns that rising debt-servicing costs could strain public finances and weigh on the Pound for some time.

Sterling will undergo crucial tests this week with the release of CPI data on Wednesday, followed by GDP figures on Thursday. While traders keep an eye on inflationary trends, a disappointing GDP print could intensify the bearish pressure on the currency. Many analysts worry that further signs of subdued economic growth, especially after the Autumn budget, could deepen the negative spiral surrounding the Pound’s outlook.

Euro, too, faced pressure today as ECB officials reaffirmed their commitment to a gradual path of monetary easing. With Fed now expected to deliver only one—or potentially zero—rate cuts in 2025, the widening rate differential is undercutting Euro. However, the single currency found some support against Sterling and Swiss Franc, helped by ECB Chief Economist Philip Lane’s call for a “middle path” on rate decisions, that’s ” neither too aggressive nor too cautious.”

Overall in the markets, Yen emerged as the strongest performer of the day, buoyed by risk aversion, despite rising yields in the US and Europe. Canadian Dollar and Aussie also posted gains. Meanwhile, Dollar and Kiwi maintained middle-ground positions, leaving the Swiss Franc, Euro, and Sterling as the weakest currencies, with the latter suffering the steepest declines due to heightened fiscal and economic concerns.

Technically, EUR/CHF recovered ahead of 0.9329 support today, as sideway trading from 0.9440 continues. Further rise remains in favor through 0.9440 in the near term. Though strong resistance is expected from 38.2% retracement of 0.9928 to 0.9204 at 0.9481 to limit upside. Firm break of 0.9329, however, will indicate that the corrective rebound from 0.9204 has already completed.

In Europe, at the time of writing, FTSE is down -0.66%. DAX is down -0.64%. CAC is down -0.60%. UK 10-year yield is up 0.0039 at 4.847. Germany 10-year yield is up 0.0089 at 2.582. Earlier in Asia, Japan was on holiday. Hong Kong HSI fell -1.00%. China Shanghai SSE fell -0.25%. Singapore Strait Times fell -0.26%.

ECB’s Lane stresses the need for “middle path” on interest rates

ECB Chief Economist Philip Lane, in an interview with Der Standard, highlighted that a “middle path” is essential to achieving the inflation target without stifling economic growth or allowing inflationary pressures to persist.

Lane warned that if interest rates fall too quickly, it could undermine efforts to bring services inflation under control. On the other hand, keeping rates too high for too long risks that inflation could “materially fall below target”.

“We think inflation pressure will continue to ease this year,” Lane stated, while adding that wage increases in 2025 are expected to moderate significantly, which could contribute to a softer inflationary environment.

While acknowledging that the overall direction of monetary policy is clear, Lane underlined the complexities of striking the right balance of “being neither too aggressive nor too cautious.”

ECB’s Vujcic: Gradual rate cuts justified amid elevated uncertainty

Croatian ECB Governing Council member Boris Vujcic emphasized a cautious and deliberate approach to monetary policy adjustments during comments to Econostream Media.

Vujcic stated that any acceleration in the pace of rate cuts would require a “significant departure” from the current economic projections, which he noted were being met by ongoing developments.

“In circumstances where uncertainties are still elevated,” Vujcic explained, “it’s better to move gradually, and this is what we’re doing.”

Vujcic also highlighted the ECB’s independence from other central banks, including the Fed. “We are not dependent on the Fed or any other central bank,” he remarked.

His comments lent support to current market expectations for ECB’s policy path, which he described as “justified” in the near term.

ECB’s Rehn: Restrictive monetary policy to end latest by mid-summer

Finnish ECB Governing Council member Olli Rehn reaffirmed the central bank’s commitment to easing monetary policy as disinflation remains on track and the region faces a weakening growth outlook. Speaking with Bloomberg TV, Rehn stated that it “makes sense to continue rate cuts.”

Rehn projected that ECB is likely to exit restrictive monetary territory “sometime in the spring-winter,” a timeline he clarified could range from January to June in Finland’s seasonal context.

He added, “I would say at the latest by midsummer, we should have left restrictive territory.”

Rehn also emphasized ECB’s independence in policy decisions, distancing it from the Fed’s approach.

“The ECB is not the 13th federal district of the Federal Reserve System,” he noted, reinforcing that the bank’s decisions are guided solely by its mandate to maintain price stability within the Eurozone.

China’s monthly trade surplus soars to USD 104.8B as exports jumps 10.7% yoy

China’s trade data for December delivered a solid performance, reflecting resilience in exports and a surprising recovery in imports.

Exports surged 10.7% yoy, significantly outpacing the 7.3% yoy expected growth and accelerating from November’s 6.7%.

Shipments to major markets rose sharply, with exports to the US jumping 18.9% yoy, ASEAN by 15.6% yoy, and the EU by 8.7% yoy. Some analysts highlighted that front-loading ahead of the Lunar New Year and trade policy shifts under Donald Trump’s incoming administration likely bolstered the month’s figures.

Imports grew 1.0% yoy, defying expectations of a -1.5% yoy decline and marking a rebound after consecutive contractions of -3.9% yoy in November and -2.3% yoy in October. This recovery was driven in part by increased purchases of commodities like copper and iron ore, with importers potentially capitalizing on lower prices.

Regionally, imports from the US rose by 2.6% yoy, while ASEAN imports grew 5.4% yoy. However, imports from the EU fell by -4.9% yoy.

Trade surplus widened from USD 97.4B in November to USD 104.8B in December, surpassing expectations of USD 100B.

Looking ahead, markets will closely monitor China’s upcoming GDP figures, due for release on Friday. Expectations are for fourth-quarter growth to clock in at 5.0% yoy.

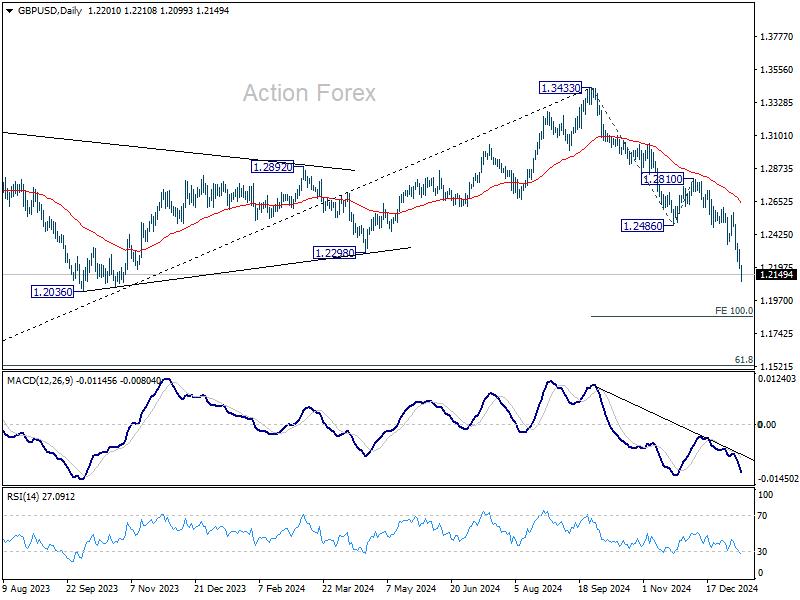

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2160; (P) 1.2241; (R1) 1.2291; More…

Intraday bias in GBP/USD remains on the downside for the moment. Current decline from 1.3433 is in progress for 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863. On the upside, break of 1.2321 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.2486 support turned resistance holds, in case of recovery.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.