{kind=link}

While Sterling continues to be the market’s primary focus as it faces heavy losses, Japanese Yen is quietly staging a modest, but broad-based recovery. However, Yen’s rally appears driven more by position adjustments ahead of tomorrow’s US non-farm payrolls report, as risk sentiment has across markets has turned more cautious. Meanwhile, there little support for Yen from increasingly dovish expectations surrounding BoJ policy.

The probability of a BoJ rate hike this month is waning. Although Japan’s wage growth has shown strong improvement, economic uncertainty is casting doubt on immediate action. March is now starting to appear to be a more plausible timeline for further policy normalization.

Former BoJ Governor Haruhiko Kuroda noted in a recent research paper that while gradual rate hikes are anticipated, estimating the neutral interest rate remains challenging, making the path for monetary policy less clear.

Separately, ex-BoJ board member Makoto Sakurai expressed skepticism about a January hike, attributing it to the uncertainties surrounding global economic trends and the incoming US Trump administration. Sakurai suggested a 70% likelihood of a March hike, indicating that BoJ might prefer to wait for more clarity.

In the UK, government officials attempted to downplay concerns over the recent financial market volatility. Chief Secretary to the Treasury Darren Jones dismissed calls for emergency intervention, stating there was “no need” for such measures despite the sharp drop in Sterling and government bond prices. Jones attributed the movements to broader global financial dynamics and emphasized the government’s firm stance on borrowing only for investment purposes. However, these reassurances did little to lift the Pound, which remains near multi-month lows.

Overall for the day so far, Yen leads gains, followed by Dollar and Swiss Franc. Sterling is the day’s worst performer, followed by Aussie and Kiwi. These rankings reflect a tilt toward risk aversion. Euro and Canadian Dollar hover in the middle. Nevertheless, the global equities have yet to reflect significant negativity.

Technically, Copper’s strong rally this week and break of 4.2831 resistance suggests that fall from 4.6904 has completed at 3.9667. Rise from there is now seen as the third leg of the corrective pattern from 3.9127 low, and could extend further towards 4.6904.

However, the fundamental backdrop for Copper raises questions about sustainability. China’s economic sluggishness, coupled with the looming threat of new US tariffs under the incoming administration, could temper the optimism in commodity markets. Yet, extended rally in Copper could help AUD/USD bounces off 0.6169 key support level.+

Eurozone retail sales marginally rise 0.1% mom in Nov, lag expectations

Eurozone retail sales edged up by 0.1% mom in November, falling short of expectations for 0.3% mom increase. Within the retail sectors, volume of sales rose slightly for food, drinks, and tobacco by 0.1%, while non-food product sales, excluding automotive fuel, contracted by -0.6%. Meanwhile, sales of automotive fuel increased by 0.8%, providing a modest lift to the overall figure.

At the EU level, retail sales grew by 0.2% mom. Among member states, Cyprus posted the strongest retail performance with a 2.3% increase, followed by Bulgaria at 1.3%, and Denmark and Latvia, both recording a 1.1% rise. Conversely, Belgium faced the sharpest contraction at -2.4%, with Germany and Spain both reporting a -0.6% decline. Poland and Finland also recorded slight decreases of -0.2%.

BoJ regional report highlights broadening price hikes

BoJ, in its latest Regional Economic Report, upgraded its economic outlook for two of Japan’s nine regions—Tohoku and Hokuriku—citing signs of moderate recovery.

The assessment for the remaining seven regions was left unchanged, with all areas described as either “picking up” or “recovering moderately.”

The report highlighted an increasingly widespread trend of price hikes by firms aiming to accommodate rising wages. While some companies, particularly larger ones, are already deliberating the scale of wage increases, smaller firms remain cautious. Concerns about the impact of higher costs on profit margins have slowed their willingness to commit to pay raises.

Japan’s nominal wage gains hit 3% in Nov, but inflation erodes real earnings

Japan’s real wages fell by -0.3% yoy in November, marking the fourth consecutive monthly decline as wage growth failed to outpace inflation again.

While nominal wages rose by a robust 3.0% yoy—beating expectations of 2.7% yoy and extending a 35-month streak of growth—consumer prices grew at an even faster pace of 3.4% yoy during the same period, up from 2.6% yoy in October.

A notable highlight in the data was the sharp rise in special cash earnings, including bonuses, which surged by 7.9% yoy. Excluding bonuses and nonscheduled payments, average wages increased by 2.7% yoy, the fastest rate in 32 years, suggesting some underlying improvement in base wages.

Australia’s retail sales growth misses expectations at 0.8% mom in Nov

Australia’s retail sales increased by 0.8% mom in November, falling short of market expectations for 1.1% mom rise. Despite the miss, all retail industries recorded growth during the month, reflecting the ongoing impact of Black Friday.

This marks the third consecutive month of retail sales growth, following gains of 0.5% mom October and 0.4% mom in September. The steady trend highlights a degree of resilience in consumer spending, though the pace remains moderate.

Robert Ewing, head of business statistics at the Australian Bureau of Statistics, noted “Black Friday sales events proved once again to be a big hit”. He also pointed out that the sales promotions now extend beyond the traditional weekend, influencing spending patterns across the entire month of November.

China’s inflation stalls at 0.1% in Dec, factory prices remain deflationary

China’s inflation decelerated again in December, with the CPI rising only 0.1% yoy, matching expectations and marking the slowest pace since April.

This brings full-year inflation for 2024 to 0.2%, far below the official target of around 3%, extending a 13-year streak of missing the annual inflation goal.

Core inflation, which strips out volatile food and energy prices, offered a slight reprieve, ticking up from 0.3% yoy to 0.4% yoy, the highest in five months.

PPI data showed a marginal improvement, with factory-gate prices contracting by -2.3% yoy compared to -2.5% yoy in November, slightly better than market expectations of -2.4% yoy. However, PPI has now stayed in deflationary territory for an extended 27 months.

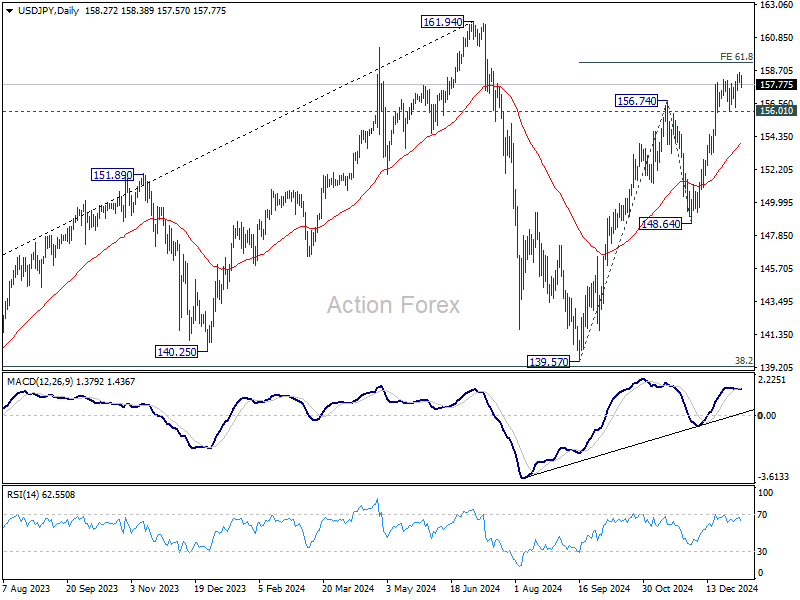

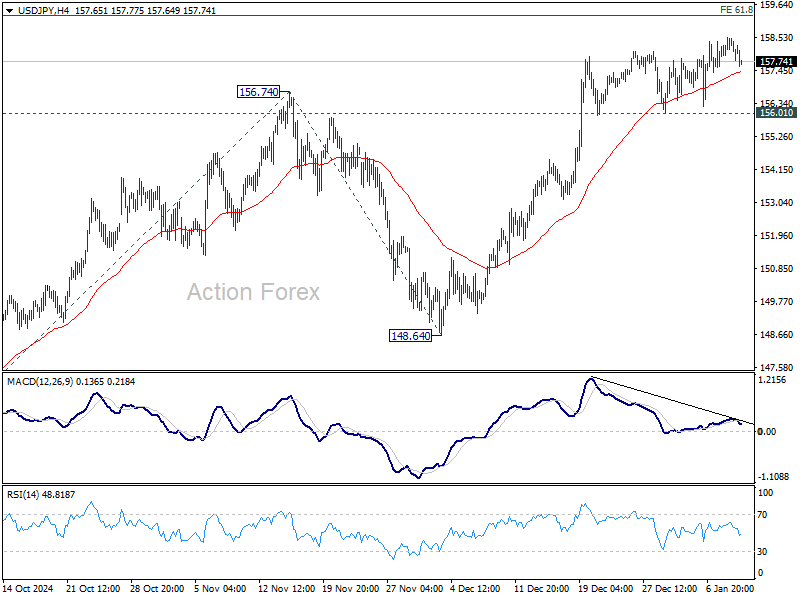

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.99; (P) 158.27; (R1) 158.64; More…

Intraday bias in USD/JPY is turned neutral first with current retreat. But further rally will remain in favor as long as 156.01 support holds. Break of 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 will extend the rally from 139.57 to retest 161.94 high. However, considering bearish divergence condition in 4H MACD, firm break of 156.01 support will indicate short term topping. Intraday bias will then be back on the downside for 55 D EMA (now at 153.98) instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.