{kind=link}

Sterling to leads declines among European currencies, with its selloff accelerating as US markets open. Downward revisions to December’s PMI manufacturing data reaffirm the grim economic outlook for both Eurozone and UK. While these revisions offered no new surprises, they underline the widespread challenges confronting major European economies. Weak growth remains a shared concern for Germany, France, and the UK, though additional political instability in Germany and France amplifies the uncertainty. The UK, meanwhile, is grappling with stagnation risks exacerbated by the impact of the latest budget measures.

Compounding the region’s troubles are looming threats of a trade war with the US, which could materialize as early as January 20 when Donald Trump officially assumes the presidency. Proposals to impose tariffs on European goods could significantly disrupt already fragile economies and further dent business sentiment in the region.

In currency markets, there is growing speculation about EUR/USD approaching parity as ECB continues its steady rate-cutting cycle of 25bps per meeting until reaching neutral range. However, the medium-term outlook for Euro is not entirely bleak. Political stabilization in Germany following upcoming elections could restore some investor confidence, offering a counterweight to bearish pressures.

The broader market picture today shows Yen as the strongest performer, followed by the Australian Dollar and New Zealand Dollar. At the other end of the spectrum, Sterling holds the title of the weakest currency, trailed by Euro and Canadian Dollar, while Dollar and Swiss Franc are mixed in the middle.

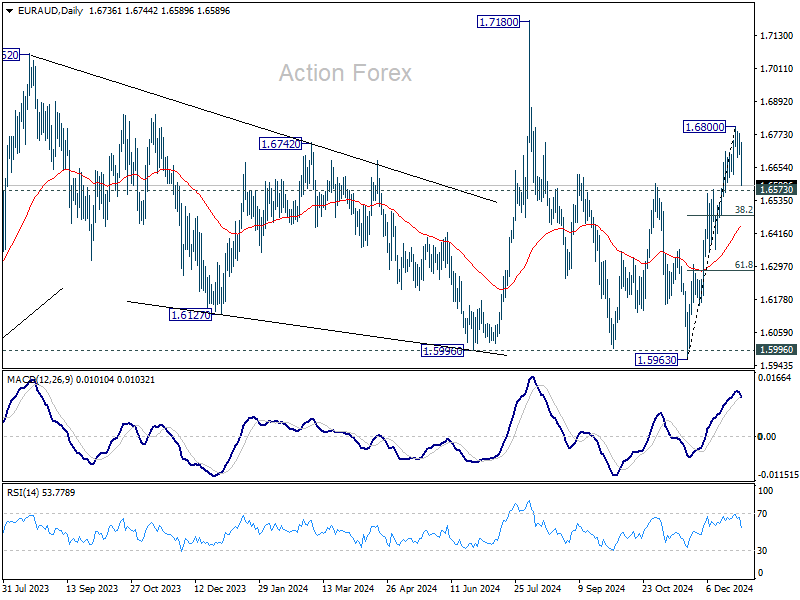

Technically, EUR/AUD’s steep decline today suggests that a short term top is possible formed at 1.6800 already. Break of 1.6573 support would bring deeper pull back to 38.2% retracement of 1.5963 to 1.6800 at 1.6480. But downside should be contained by 55 D EMA (now at 1.6443) to bring rebound.

In Europe, at the time of writing, FTSE is up 0.72%. DAX is up 0.10%. CAC is down -0.56%. UK 10-year yield is down -0.001 at 4.567. Germany 10-year yield is down -0.025 at 2.344. Earlier in Asia, Japan was on holiday. Hong Kong HSI fell -2.18%. China Shanghai SSE fell -2.66%. Singapore Strait Times rose 0.35%.

US initial jobless claims falls to 211k, vs exp 223k

US initial jobless claims fell -9k to 211k in the week ending December 28, below expectation of 223k. Four-week moving average of initial claims fell -3.5k to 223k.

Continuing claims fell -52k to 1844k in the week ending December 21. Four-week moving average of continuing claims fell -7k to 1871k.

UK PMI manufacturing finalized at 47, sentiment at two-year low

UK PMI Manufacturing was finalized at 47.0 in December, down from 48.0 in November, marking the third consecutive month of contraction. Persistent challenges, both domestic and international, weighed heavily on the sector, resulting in the sharpest production decline in nearly a year.

Rob Dobson, Director at S&P Global Market Intelligence, highlighted a “stalling domestic economy, weak export sales, and future cost concerns” as key drivers of the downturn. Business confidence fell to its lowest point in two years.

Small and medium-sized enterprises have been hit hardest during the downturn, while labor market pressures intensify. December saw the steepest job cuts since February, as firms moved to restructure in anticipation of 2025 National Insurance and minimum wage increases. Export sales also suffered due to weaker demand from Europe, Asia, and the US.

Input costs continued to rise, fueled by higher transportation, labor, and material expenses, with some increases linked to ongoing supply chain challenges. Looking ahead, the impact of Budget 2025 measures is expected to drive costs higher, potentially complicating BoE’s decision on further rate cuts despite mounting signs of economic stress.

Eurozone PMI manufacturing finalized at 45.1, Spain outshines peers with low China exposure

Eurozone PMI Manufacturing was finalized at 45.1 in December, down from November’s 45.2, marking the sector’s 30th consecutive month of contraction. Key indicators, including new orders and inventory levels, signaled ongoing struggles across the bloc.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, emphasized the continued downturn: “New orders have dropped even more than in the previous two months, crushing any hopes for a quick recovery.” Inventories of intermediate and finished goods declined sharply, reflecting weak demand expectations.

Job cuts persisted across Eurozone, with the pace of reductions remaining significant, despite a slight deceleration. This trend is expected to continue as companies restructure operations amid weak industrial activity.

Spain remained a bright spot, with its PMI rising to 53.3, indicating robust expansion. Greece also posted growth at 53.2, a five-month high. However, the largest economies continued to struggle: Germany (42.5) reached a three-month low, France (41.9) fell to a 55-month low, and Italy (46.2) managed only a slight improvement.

Spain’s relative resilience stems from its low export exposure to China (2%) and benefits from lower energy costs, which have helped it weather the industrial crisis better than its peers. However, with Spain accounting for only 12% of Eurozone GDP, its strength alone cannot offset the widespread industrial recession.

China’s Caixin PMI manufacturing falls back to 50.5 as downward pressures persist

China’s Caixin Manufacturing PMI dropped to 50.5 in December, down from 51.5 and below market expectations of 51.6, signaling a moderation in the sector’s growth.

While supply and demand expanded modestly, external demand remained a significant drag, according to Wang Zhe, Senior Economist at Caixin Insight Group.

Zhe highlighted several challenges, noting that external demand was “sluggish”, while job market suffered a “notable contraction.” Additionally, sales prices were weak, and market optimism continued to decline.

The survey pointed to “prominent downward pressures”, stemming from subdued domestic demand and challenging external conditions, which have squeezed profit margins and dented confidence.

The report also suggested that the impact of previous policy stimulus measures has yet to yield consistent results, with more time needed to gauge their effectiveness.

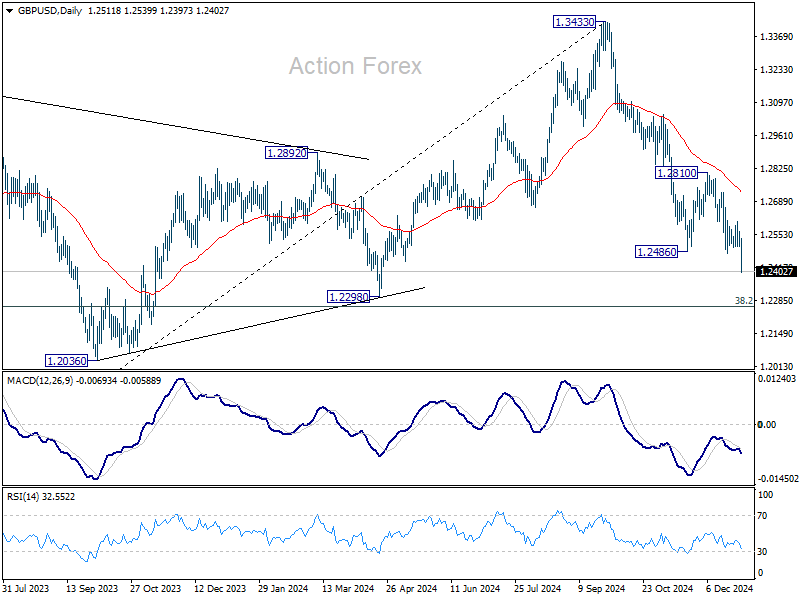

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2481; (P) 1.2545; (R1) 1.2582; More…

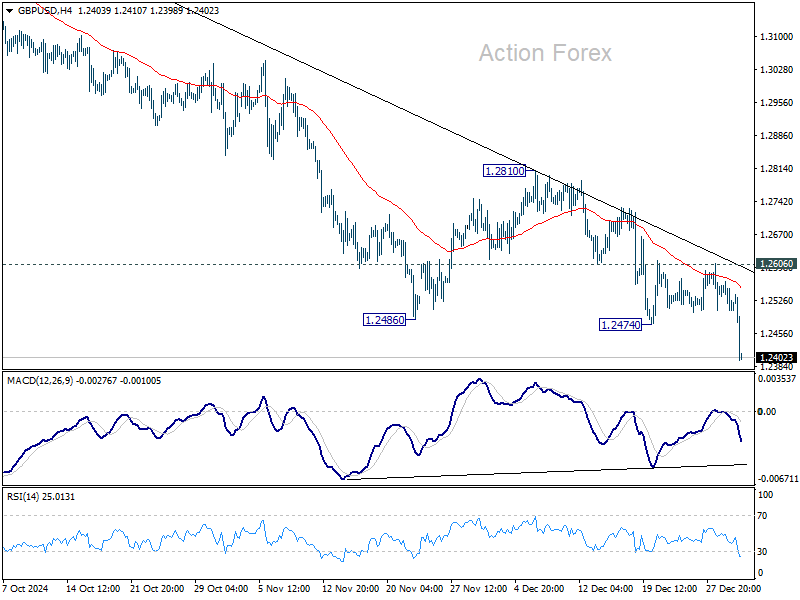

GBP/USD’s decline from 1.3433 resumed by breaking through 1.2474 support today. Intraday bias is back on the downside for 1.2298 cluster support zone. Strong support is expected there to contain downside to bring rebound, at least on first attempt. On the upside, break of 1.2606 minor resistance will indicate short term bottoming, and turn bias back to the upside for 1.2810 resistance next.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.