{kind=link}

Commodity currencies are starting the week with a modest recovery as Aussie, Kiwi, and Loonie attempt to pare steep losses from earlier in the month. Gains remain limited in the subdued holiday trading environment, but these currencies could see further upside if China’s NBS PMIs due tomorrow deliver an improved outlook for 2025. However, any significant moves are expected to materialize only after trading volumes normalize post-New Year.

Adding to the focus on China, the World Bank last week raised its GDP growth forecasts for the country. The 2024 GDP growth forecast was revised up slightly to 4.9%, from June’s projection of 4.8%, though it remains below Beijing’s target of around 5%. For 2025, growth was upgraded more notably, from 4.1% to 4.5%. Yet, the World Bank also warned that slower household income growth and the negative wealth effect of falling home prices could continue to weigh on consumption, posing challenges to sustained growth.

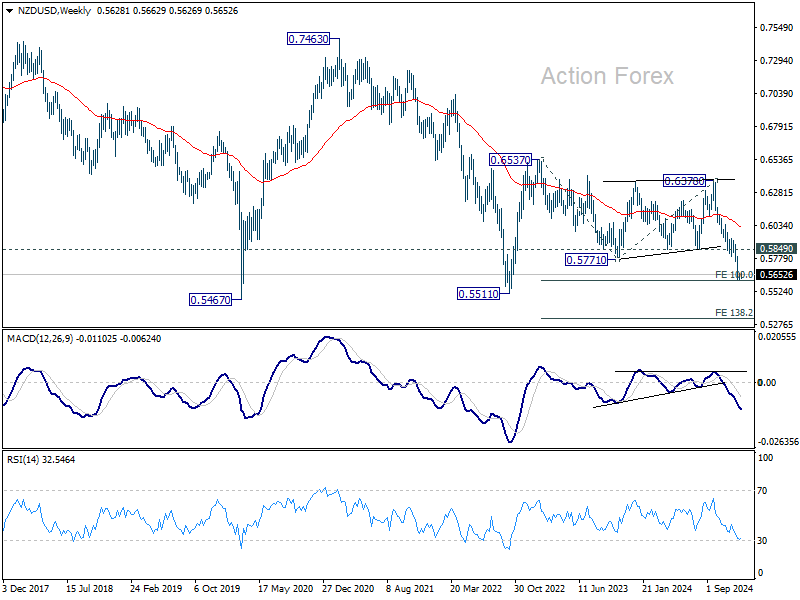

Overall, Dollar remains the best performer for the month, while New Zealand Dollar sits as the second weakest. Technically, NZD/USD is now pressing an important fibonacci level, 100% projection of 0.6537 to 0.5771 from 0.6378 at 0.5612. Strong bounce from current level, followed by firm break of 0.5849 support turned resistance, will be the first sign that decline from 0.6537 has completed as a corrective move. Stronger rebound should then be seen back to 55 W EMA (now at 0.6012) at least. However, decisive break of 0.5612 will argue that large down trend is resuming with further downside acceleration through 0.5468/5511.

In Asia, Nikkei fell -0.96%. Hong Kong HSI fell -0.09%. China Shanghai SSE rose 0.21%. Singapore Strait Times rose 0.37%. Japan 10-year JGB yield fell -0.0132 to 1.091.

Swiss KOF falls below average, signals dampened outlook

Swiss KOF Economic Barometer fell to 99.5 in December, down from 102.9 in November and below market expectations of 101.1. This decline brings the indicator slightly below its medium-term average, signaling a “dampened” outlook for the Swiss economy .

KOF Economic Institute attributed the drop to weaker performance across multiple sectors. In particular, indicators for manufacturing, other services, the hospitality industry, foreign demand, and private consumption showed significant declines, collectively driving the overall decrease.

Japan’s PMI manufacturing finalized at 49.6, nears stabilization and cost pressures persist

Japan’s Manufacturing PMI for December was finalized at 49.6, an improvement from November’s 49.0, indicating a gradual move toward stabilization in the sector.

According to Usamah Bhatti of S&P Global Market Intelligence, the data “painted a picture of a near-stabilization” in manufacturing conditions as declines in both production and new orders softened.

Encouraged by these improvements, firms increased hiring, partly to address existing labor shortages and in anticipation of future demand recovery.

However, price pressures remained elevated, with input costs rising at their fastest pace since August due to higher raw material and labor costs, compounded by Yen’s weakness. To manage these cost burdens, manufacturers passed on higher prices to clients, resulting in the strongest output charge increases in five months.

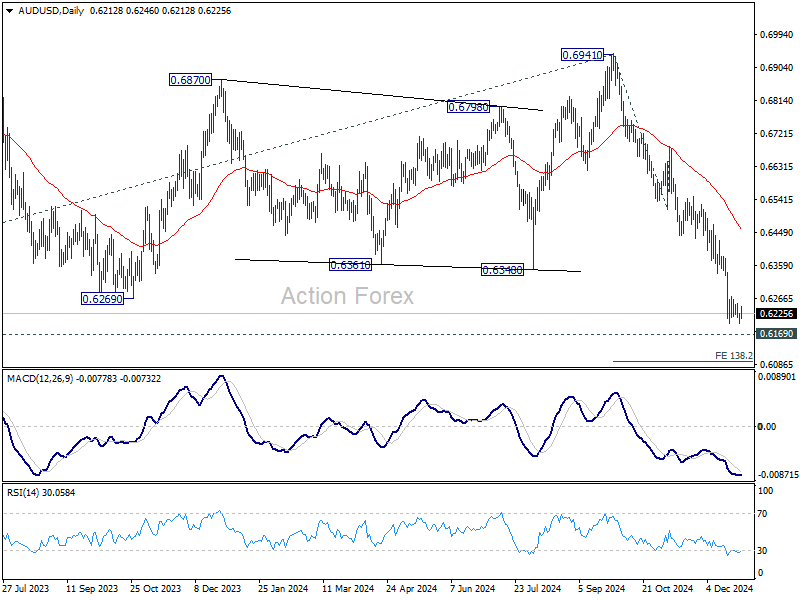

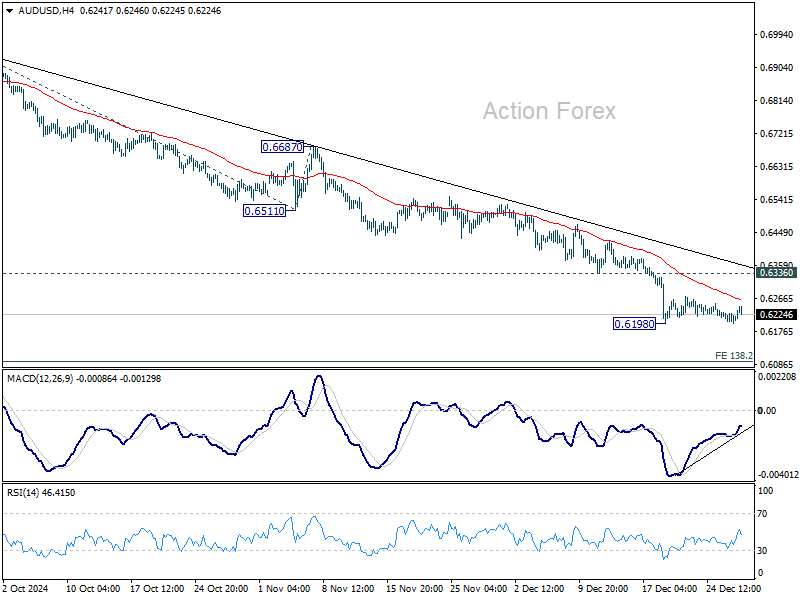

AUD/USD Daily Report

Daily Pivots: (S1) 0.6199; (P) 0.6218; (R1) 0.6236; More...

AUD/USD recovers mildly today but overall outlook is unchanged. Intraday bias stays neutral first, and consolidations from 0.6198 should be relatively brief as long as 0.6336 support turned resistance holds. On the downside, break of 0.6198 will resume the fall from 0.6941 to 0.6169 long term support, and then 138.2% projection of 0.6941 to 0.6511 from 0.6687 at 0.6074. Nevertheless, firm break of 0.6336 will bring stronger rebound lengthier correction before staging another decline.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. Firm break of 0.6169 support will confirm down trend resumption for 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6588) holds.