{kind=link}

Yen saw broad declines during Asian session, briefly falling below 158 against Dollar, but the selloff was quickly mitigated by verbal intervention, as least partially.

The decline was triggered by weaker-than-expected Tokyo inflation data. Stripping out energy and food prices, core-core inflation remained relatively stable, signaling limited urgency for BoJ to proceed with further rate hikes in the near term.

This aligns with the cautious tone seen in the BoJ’s December meeting summary, which revealed deep divisions among policymakers. While a minority of hawks pushed for “forward-looking” and “preemptive” actions, the majority seemed favoring a measured approach, citing concerns over wage growth and external risks.

Verbal intervention from Japanese officials helped limit losses in Yen, nevertheless. Finance Minister Katsunobu Kato reiterated the government’s commitment to addressing excessive currency movements, stating, “The Japanese government has been alarmed by foreign exchange developments, including those driven by speculators, and will take appropriate action against excessive moves.” While this provided temporary relief, it was insufficient to reverse Yen’s broader weakness.

For the week so far, Dollar is currently the strongest, supported by lingering strength from Fed’s recent hawkish outlook. However, the greenback’s momentum remains constrained, with gains capped below last week’s highs amid thin year-end holiday trading. Euro has emerged as the second-strongest currency, followed by Loonie. Yen has taken the weakest spot, followed by Swiss Franc and Aussie. Both Kiwi and Sterling are positioning in the middle.

Looking ahead, market activity is expected to remain subdued through the rest of the week, with an ultra-light economic calendar offering little to stir volatility. The sole notable release is US goods trade balance, which is unlikely to prompt significant moves. Barring surprises, trading volumes are expected to remain low until after the New Year holiday next week.

BoJ summary highlights division on timing of rate hikes

BoJ Summary of Opinions from its December 18–19 meeting revealed a divided board on the timing of monetary policy normalization. While some members advocated for action soon, citing upside risks to prices, others expressed caution due to slow wage growth, soft overseas demand, and heightened uncertainties.

One member emphasized that with economic activity and prices aligning with BoJ’s outlook, risks to inflation were becoming “skewed to the upside.” The member argued for a “forward-looking, timely, and gradual” adjustment of monetary policy. Similarly, another member noted that the sustained increase in prices over the past three years, partly driven by Yen’s depreciation, would likely contribute to higher underlying inflation, warranting “preemptive” rate hikes.

Conversely, more dovish members maintained that the current risks to prices “do not suggest a pressing need” for rate hike. One member cited uncertainties surrounding tax and fiscal policies in Japan and the stance of the incoming US administration as reasons to maintain the current policy stance, emphasizing a risk management approach.

Overall, the BoJ board appears focused on assessing the outcomes of next year’s spring wage negotiations and the impact of US policy shifts before making further moves toward policy normalization.

Japan’s Tokyo CPI core rises to 2.4% in Dec, but core-core dips to 1.8%

Japan’s Tokyo core CPI (excluding food) rose from 2.2% yoy to 2.4% yoy in December, marking its highest level since August but falling short of expectations for 2.5%. The increase was largely driven by a 13.5% yoy surge in energy prices, reflecting the phase-out of government subsidies for gas and electricity bills. However, when excluding utility costs, inflation pressures appear steady.

Core-core CPI (excluding food and energy) softened to 1.8% yoy from 1.9% yoy, while services inflation edged up slightly from 0.9% to 1.0%. Meanwhile, headline inflation accelerated to 3.0% yoy from 2.6% yoy, with energy and food prices, including rice, contributing significantly to the increase too.

The uptick in Tokyo inflation highlights lingering pressures from rising utility and food costs, which may weigh on consumer spending and deter firms from implementing further price hikes. These factors, coupled with broader signs of economic weakness, could delay BoJ ’s timeline for raising interest rates.

Japan’s industrial output slips -2.3% mom in Nov, indecisive fluctuation continues

Japan’s industrial production declined -2.3% mom in November, outperforming expectations of a -3.4% mom drop, but marking the first contraction in three months.

The decrease was driven by weaker exports of semiconductor manufacturing devices and cars, highlighting challenges in external demand. Out of 15 industrial sectors, 11 recorded declines, while 3 sectors reported gains.

Production machinery saw a significant -9.1% drop, largely due to falling exports of chip-making equipment to China and Taiwan, while motor vehicle output fell -4.3%, and fabricated metal products dropped -5.7%.

Despite the slump, the Ministry of Economy, Trade, and Industry maintained its view that industrial production “fluctuates indecisively,” while warning of risks tied to the economic outlooks of the US and China.

Looking ahead, METI’s poll of manufacturers predicts a rebound, with output expected to rise 2.1% in December and an additional 1.3% in January.

Separately, retail sales posted a robust 2.8% yoy gain, exceeding expectations of 1.5%, signaling resilience in domestic demand.

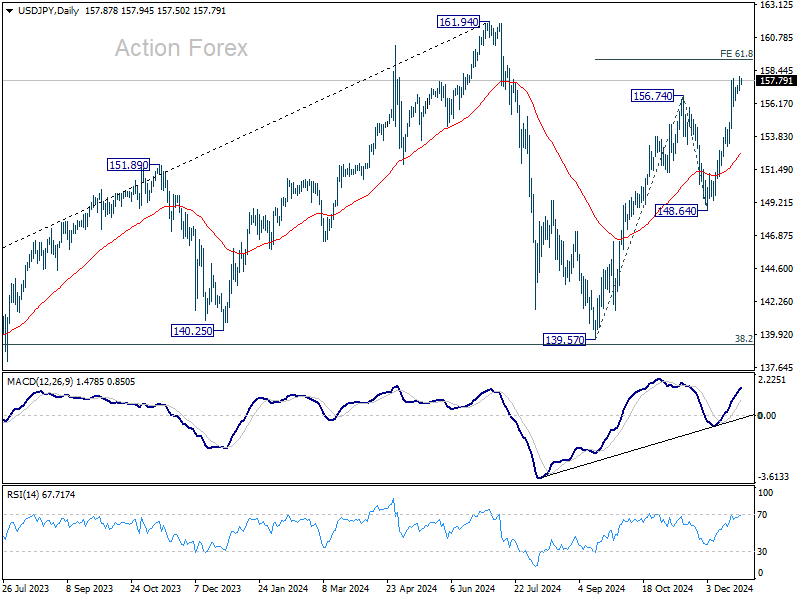

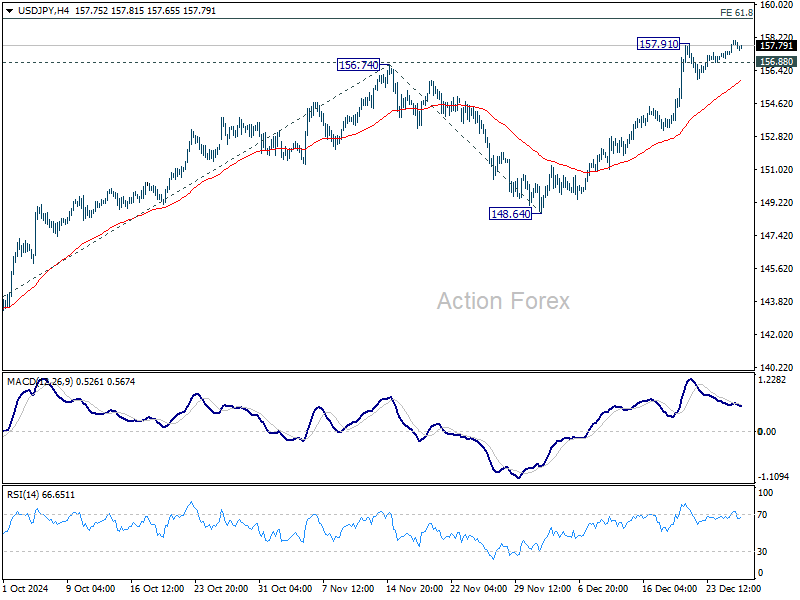

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.32; (P) 157.70; (R1) 158.42; More…

USD/JPY’s rally is trying to resume by breaching 157.91 temporary top and intraday bias is back on the upside. Rise from 139.57 is extending to 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. Firm break there will pave the way back to 161.94 high. On the downside, though, below 156.88 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.