{kind=link}

Dollar edged higher in subdued holiday trading, maintaining its recent strength but staying within a narrow range below last week’s highs against major currencies. Markets largely brushed aside the disappointing US durable goods orders data, as the series is known for its volatility. Moreover, traders are prioritizing labor market and consumption trends, which Fed views as more significant for its policy decisions for the moment.

Canadian Dollar Showed little reaction to the better-than-expected October GDP growth, as concerns about sustained economic strength linger. November’s advance estimate pointed to a contraction, reinforcing the overall sluggish outlook. BoC has shifted into a measured phase of easing, where further rate cuts are evaluated on a meeting-by-meeting basis. While policymakers have signaled a slower pace of reductions in 2025, uncertainty remains around the overall depth and timing of further easing, keeping CAD on the defensive.

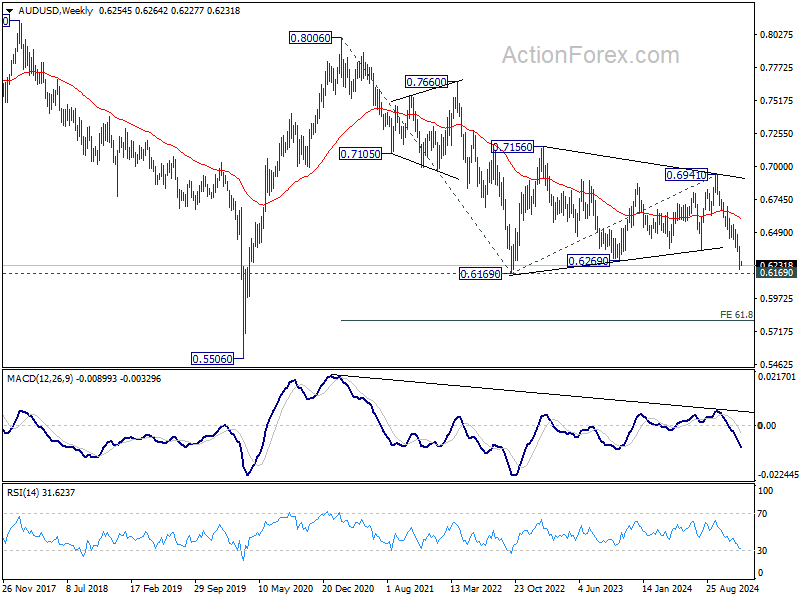

Looking ahead to the Asian session, RBA’s December meeting minutes will be a focal point. RBA’s latest dovish shift has raised speculation that policymakers are moving closer to rate cuts, though recent data suggests that easing is not yet imminent. Traders will scrutinize the minutes for details on the board’s reasoning for the pivot and the conditions that could prompt the first cut.

Technically, AUD/USD is quickly approaching 0.6169 key support after last week’s downside acceleration. For now, given the light economic calendar at this year period, it’s unlikely for the pair to break through this support yet. Indeed, less dovish that expected RBA minutes might help AUD/USD for a bounce. Yet, the medium term down trend is expected at a later stage, probably in later January after Australia’s Q4 CPI is published. Any bounce in the near term could be viewed as selling possibilities.

In Europe, at the time of writing, FTSE is up 0.12%. DAX is down -0.14%. CAC is down -0.07%. UK 10-year yield is up 0.034 at 4.543. Germany 10-year yield is up 0.025 at 2.312. Earlier in Asia, Nikkei rose 1.19%. Hong Kong HSI rose 0.82%. China Shanghai SSE fell -0.50%. Singapore Strait Times rose 0.87%. Japan 10-year JGB yield rose 0.0136 to 1.069.

US durable goods orders slump -1.1% mom, transportation sector leads decline

US durable goods orders dropped -1.1% mom in November to USD 285.1B, significantly missing market expectations of a -0.3% mom decline. This also marks the third decline in the last four months.

Excluding transportation, orders edged down -0.1% mom to USD 189.6B, while orders excluding defense fell -0.3% mom to USD 267.4B. The transportation equipment category, which has also fallen in three of the past four months, accounted for the largest share of the decline, with a -2.9% mom drop to USD 95.5B.

Canada’s GDP beats Oct expectations, but Nov decline looms

Canada’s GDP rose 0.3% mom in October, surpassing expectations of 0.2% mom, with 12 out of 20 sectors contributing to the growth.

This marked a rebound for the goods-producing industries, which expanded by 0.9% mom after four months of contraction, driven primarily by mining, quarrying, and oil and gas extraction.

The services-producing industries edged up by 0.1% mom, supported by growth in real estate and rental and leasing, which saw its fifth consecutive month of expansion.

However, preliminary data for November suggests a -0.1% mom contraction in real GDP, with declines in mining, quarrying, and oil and gas extraction, as well as transportation, warehousing, and finance and insurance. These losses were partly offset by gains in accommodation and food services and continued strength in real estate and rental and leasing.

ECB’s Lagarde: Inflation target within reach, services inflation still stubborn

In an interview with the Financial Times, ECB President Christine Lagarde expressed optimism about nearing the inflation target.

She remarked that ECB is “very close” to declaring that inflation has been “sustainably” brought back to its 2% medium-term target.

The latest inflation reading of 2.2% reflects the success of ECB’s restrictive monetary policy. However, she highlighted persistent concerns in the services sector, where inflation remains high at 3.9%, describing it as “not budging much” despite showing slight signs of decline.

On the topic of US tariff threats, Lagarde emphasized the economic risks of retaliatory trade measures, stating, “Retaliation was a bad approach.” She warned that tit-for-tat trade conflicts could harm the global economy.

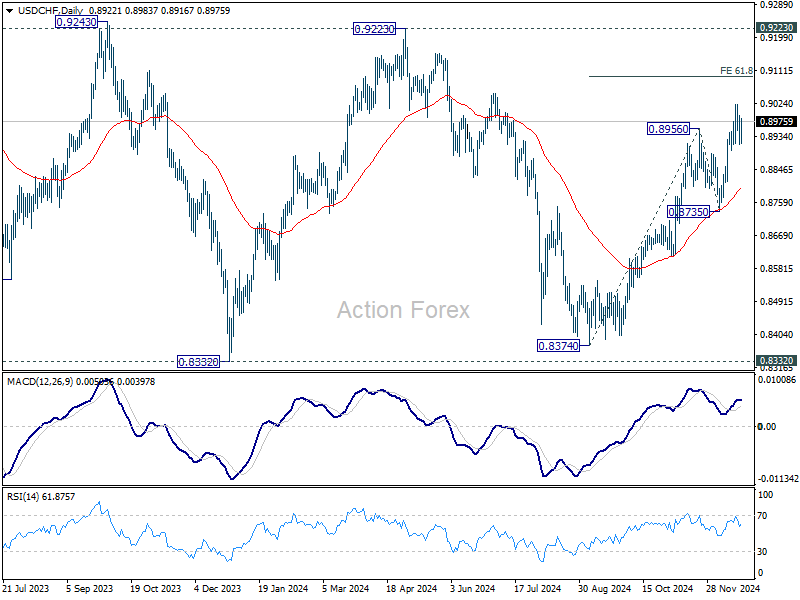

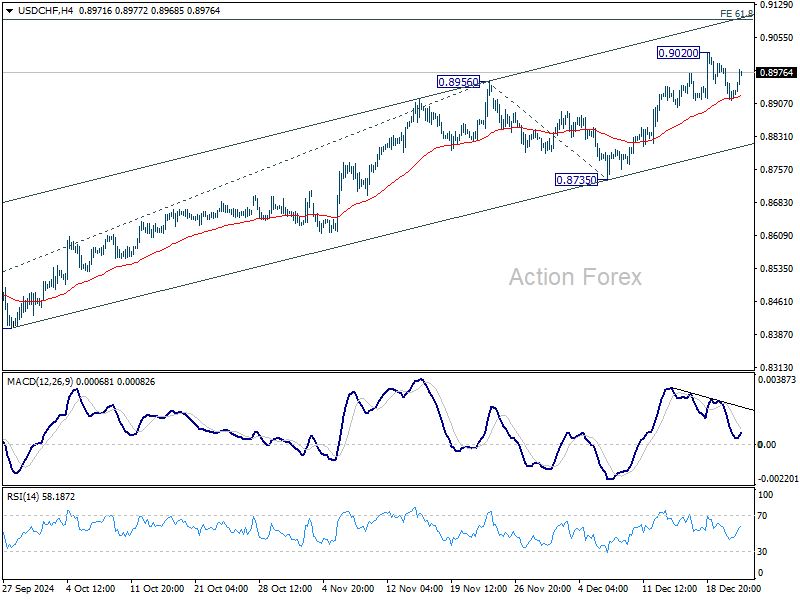

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8898; (P) 0.8946; (R1) 0.8979; More…

USD/CHF bounces after drawing support from 55 4H EMA, but stays below 0.9020 temporary top. Intraday bias remains neutral at this point. While deeper pull back might be seen, downside should be contained above 0.8735 support to bring another rally. Above 0.9020 will resume the rise from 0.8374 and target 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.