{kind=link}

Dollar has strengthened against commodity currencies this week but remains range-bound against Euro and Pound, as markets await Fed’s rate decision to gauge the next move. While a 25bps rate cut is fully expected in with no chance of deviation, the focus is on how hawkish Fed’s messaging will be. Key questions include the likelihood of a pause in January, the projected pace of easing in 2025, and any adjustments to the neutral rate. The answers to these will shape the direction of Dollar, yields, and broader markets, at least for the near term.

British Pound showed little reaction to today’s UK CPI data, which confirmed persistent inflationary pressure. Services inflation remains elevated at 5%, with no clear signs of easing materially. Coupled with yesterday’s wage growth data, this is more than enough for BoE to hold rates steady this week. Markets maintain a base case of four rate cuts in 2025, with little expectation for a shift unless BoE delivers unexpectedly drastic signals during its upcoming meeting.

For the week so far, the Pound leads as the strongest performer, followed by Yen and then Dollar. Australian Dollar is the weakest, trailed by Canadian Dollar and New Zealand Dollar, while Euro and Swiss Franc are mixed in the middle.

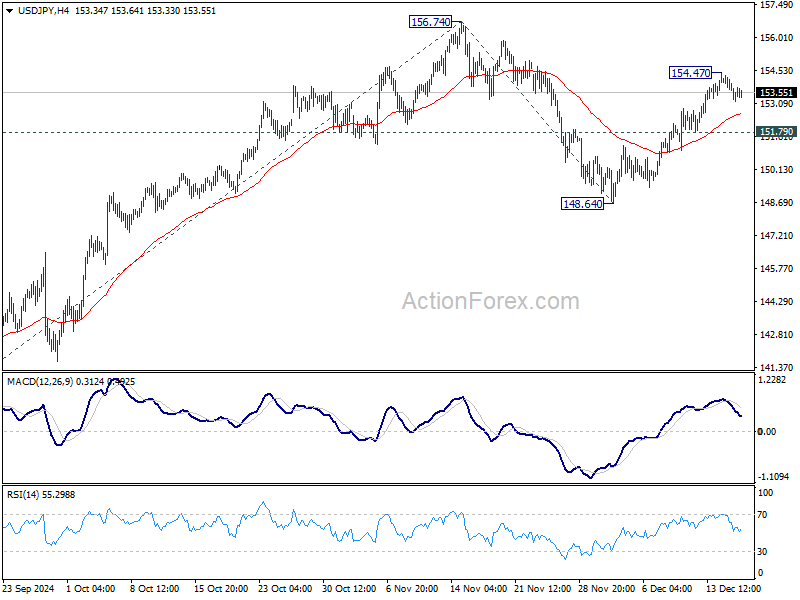

Technically, USD/JPY’s rally from 148.64 is losing some momentum as see in 4H MACD. Another rise is in favor for now. But real near term hurdle lies in 156.74 resistance. Break of 4.5% handle in 10-year yield is probably needed to push USD/JPY through 156.74 to resume the rally from 139.57. Otherwise, the pair could engage in range trading between 148.64/156.74 for longer, with risk of another fall before completing the corrective pattern from 156.74.

Looking ahead, Eurozone CPI final will be released in European session. US will release building permits and housing starts, current account later in the day. But main focuses will be on FOMC rate decisions.

Key FOMC Questions: Pause in January, Easing Path in 2025, and Neutral Rate

FOMC rate decision takes center stage today, with a 25bps rate cut widely anticipated, lowering the federal funds rate to 4.25–4.50%. Markets see virtually no chance of a different outcome, making the focus squarely on Fed Chair Jerome Powell’s statement and the updated economic projections. Expectations are for Fed to signal a slower pace of easing in 2025, aligning with signs of a resilient economy and sticky inflation.

Three key questions arise from today’s new projections.

First, the possibility of a pause in January is in focus. With markets pricing an 84% probability of no rate change at the next meeting, the voting split within the FOMC could hint at how close policymakers are to a pause in the easing cycle.

Second, attention will shift to the pace of easing in 2025. Fed’s prior projections and dot plot suggested a median rate of 3.4% by the end of next year. Markets are currently pricing in a 33% chance of rates falling to 3.75–4.00% by December 2025. A significant upward revision in Fed’s median forecast would signal caution about inflation persistence and align with tighter-than-expected monetary policy.

Third, the neutral rate will be scrutinized. The previous projection of a longer-run rate was 2.9%, slightly higher than 2.8% in June. A move toward or above 3% could be psychologically significant, signaling higher baseline expectations for economic growth and inflation stability in the post-tightening environment.

In terms of market reactions, Fed’s “hawkish cut” could lift both the 10-year Yield and Dollar Index. However, breaking out of current ranges will require more than today’s decision.

For the DXY, resistance at 108.07 must be cleared to confirm underlying bullish momentum, which would likely need support from a 10-year yield break above 4.505%. These breakouts would likely hinge on clarity around fiscal and trade policies from the incoming administration.

UK CPI accelerates to 2.6% in Nov, core CPI up to 3.5%

UK CPI accelerated from 2.3% yoy to 2.6% yoy in November, matched expectations. Core CPI, (excluding energy, food, alcohol and tobacco), accelerated from 3.3% yoy to 3.5% yoy, below expectation of 3.6% yoy. CPI goods annual rate rose from -0.3% yoy to 0.4% yoy , while CPI services annual rate was unchanged at 5.0% yoy.

Japan’s export rises 3.8% yoy in Nov, while import falls -3.8% yoy

Japan’s exports rose 3.8% yoy in November to JPY 9.152T, supported by increased shipments of chip-making equipment to Taiwan and nonferrous metals to China, marking the second consecutive month of export growth. Imports, however, fell -3.8% yoy to JPY 9.270T, marking their first decline in eight months due to reduced demand for crude oil from Saudi Arabia and electronics parts from Taiwan.

The overall trade deficit stood at JPY -117.6B, extending its red streak to five months. On a seasonally adjusted basis, the deficit widened to JPY -384B from JPY -229B in October, as imports increased 1.9% mom, outpacing the 0.2% mom rise in exports.

Trade with key partners highlighted persistent imbalances. Japan recorded a JPY 664.03B trade surplus with the US, despite exports falling -8.0% yoy, while imports dipped slightly by -0.6% yoy.

Conversely, its trade deficit with China expanded to JPY 682B, as exports grew 4.1% yoy, and imports rose 4.2% yoy.

The trade gap with the EUR remained significant at JPY 210.19B, with exports plunging -12.5% yoy, while imports decreased -5.4% yoy.

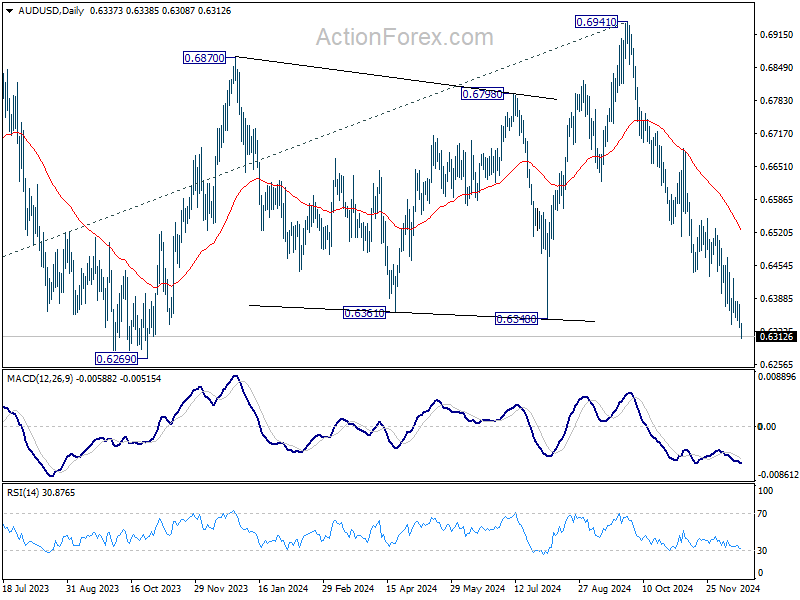

AUD/USD Daily Report

Daily Pivots: (S1) 0.6319; (P) 0.6349; (R1) 0.6365; More...

AUD/USD’s decline resumed by breaking through 0.6336 temporary low and intraday bias is back on the downside. Current fall from 0.6941 should target 0.6269 support next. On the upside, above 0.6382 minor resistance will turn intraday bias neutral and bring consolidations again, before staging another fall.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.