{kind=link}

Sterling rallied broadly today, driven by BoE’s Monthly Decision Maker Panel survey, which underscored a complex economic outlook that reinforces the central bank’s cautious approach to policy easing. The survey revealed a mixed picture of inflationary and deflationary pressures. Notably, 54% of businesses anticipate raising prices in response to National Insurance contribution hikes outlined in the new government’s first budget. However, an equal proportion also expects to reduce staffing levels, signaling growing concerns about employment.

Additionally, 38% of firms indicated plans to pay lower wages than previously intended, contributing to a deceleration in expected pay growth to 3.8% from 4.1%. Meanwhile, inflation expectations among businesses ticked higher, with consumer price inflation projected at 2.7% for the year ahead, up from 2.6% in October. For November alone, inflation expectations jumped to 2.8% from 2.5%, suggesting persistent cost pressures despite softening wage growth. These mixed signals present a challenging picture for BoE as it deliberates its next steps.

Overall for the day, though, Euro led gains among major currencies, as markets digest the latest developments in France’s political sphere. Prime Minister Michel Barnier has resigned following a no-confidence vote against his government, with President Emmanuel Macron expected to address the nation later today. Sterling ranks as the second strongest currency of the day, followed by the Swiss Franc, marking a rebound for European currencies after recent underperformance. On the other hand, Yen is underperforming, followed by the Dollar. Commodity-linked currencies, including Aussie, Kiwi and Loonie, are positioning in the middle.

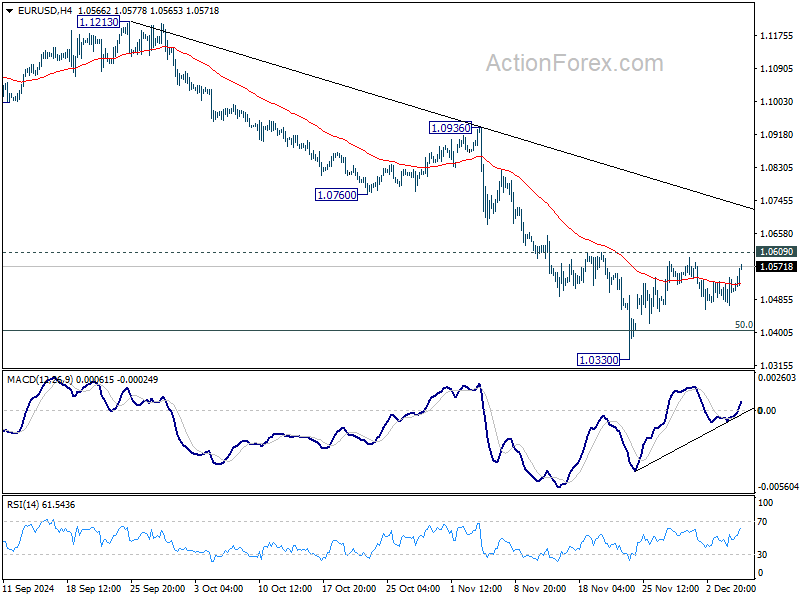

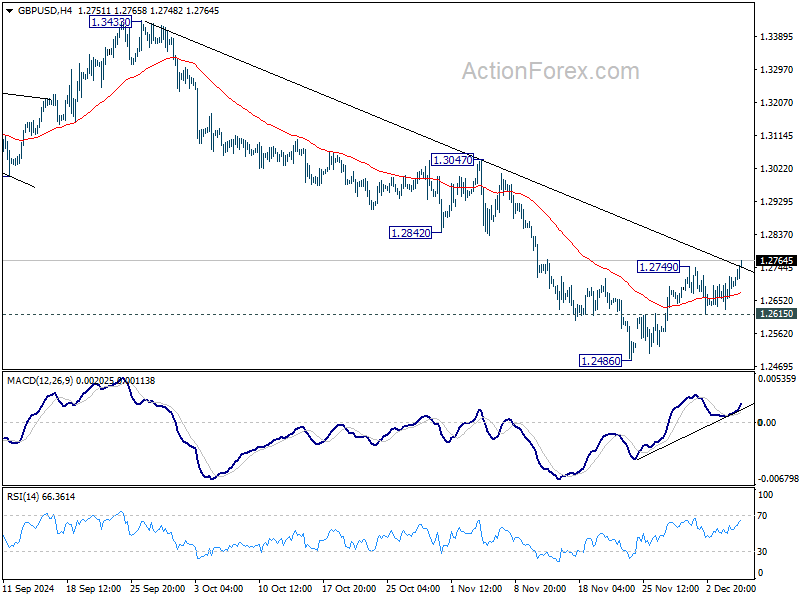

Technically, GBP/USD’s break of 1.2749 resistance is a sign that Dollar’s near term pullback is resuming, at least against Europeans. Focus will now be on 1.0609 resistance in EUR/USD and 0.8800 support in USD/CHF. Firm break of these levels should confirm that deeper decline in the greenback is underway. But still, the next big move would still be subject to tomorrow’s US non-farm payroll report.

In Europe, at the time of writing, FTSE i down -0.01%. DAX is up 0.37%. CAC is up 0.18%. UK 10-year yield is up 0.0231 at 4.273. Germany 10-year yield is up 0.055 at 2.116. Earlier in Asia, Nikkei rose 0.30%. Hong Kong HSI fell -0.92%. China Shanghai SSE rose 0.12%. Singapore Strait Times rose 0.60%. Japan 10-year JGB yield rose 0.0198 to 1.073.

US initial jobless claims rises 9k to 224k, vs exp 215k

US initial jobless claims rose 9k to 224k in the week ending November 30, above expectation of 215k. Four-week moving average of initial claims rose 750 to 218k.

Continuing claims fell -25k to 1871k in the week ending November 23. Four-week moving average of continuing claims fell -3k to 1884k.

Canada’s trade deficit narrows to CAD – 0.9B as exports rebound in October

Canada’s merchandise trade deficit with the world narrowed to CAD -0.9B in October from September’s CAD -1.3B, driven by a 1.1% mom rise in exports. This marks a rebound following three consecutive monthly declines. Imports also increased, albeit at a slower pace, rising 0.5% mom.

Despite the headline growth in exports, declines were recorded in 8 of the 11 product sections. The increase was partly attributed to higher prices, with export volumes rising modestly by 0.4% mom in real terms.

Eurozone retail sales fall -0.5%Q mom in Oct, EU down -0.3% mom

Eurozone retail sales volume declined by -0.5% mom in October, underperforming expectations of a -0.4% mom contraction. Breaking down the data, sales for food, drinks, and tobacco edged up 0.1% mom, while non-food products (excluding automotive fuel) slumped -0.9% mom, and automotive fuel sales in specialized stores dropped -0.3% mom.

Across the broader European Union, retail sales volume fell by -0.3% mom. Among member states, the sharpest monthly declines were seen in Belgium (-1.7%), Germany (-1.4%), and Denmark and Cyprus (both -1.1%). Conversely, Luxembourg led with a strong 2.4% increase, followed by Poland at 2.2% and Lithuania at 1.5%.

BoJ’s Nakamura skeptical on wage and inflation sustainability

BoJ board member Toyoaki Nakamura expressed a cautious stance on monetary policy adjustments, emphasizing the need for careful calibration aligned with Japan’s economic recovery.

“We are at a state where it’s important to adjust the degree of monetary easing carefully in accordance with the economic recovery by assessing a broad array of data,” Nakamura said.

As a known dove on the BoJ board, Nakamura raised doubts about the durability of current wage hikes, saying he is “not confident” about their sustainability. He also flagged concerns about inflation, noting the possibility that the annual rate “may not reach 2% from fiscal 2025 onwards.”

In a related development, a Jiji Press report indicated growing hesitation within BoJ regarding a premature rate increase. Market expectations for a December rate hike have fallen sharply, with traders now pricing in only a 36% chance, down from 66% at the end of last week.

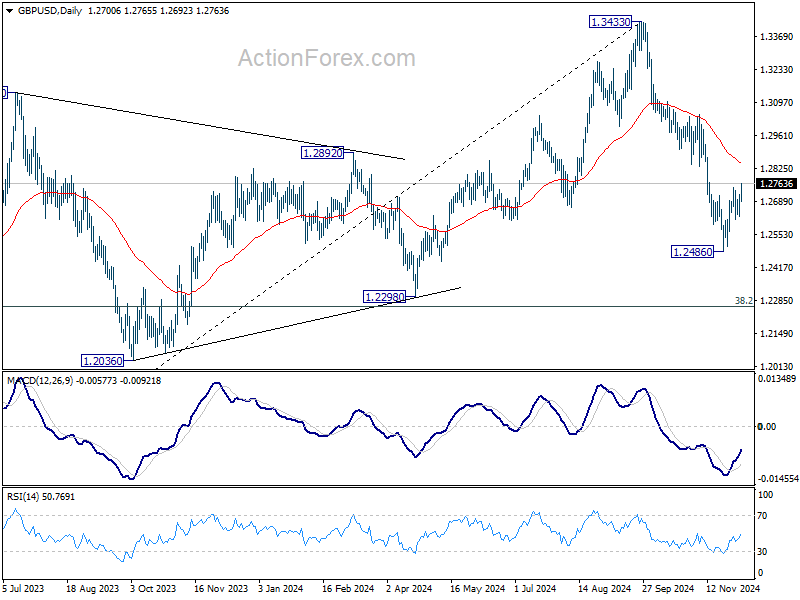

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2646; (P) 1.2684; (R1) 1.2737; More…

GBP/USD’s rebound from 1.2486 resumes by breaking 1.2749 resistance today. Intraday bias is back on the upside for stronger rally to 55 D EMA (now at 1.2853). Strong resistance is expected there to limit upside, and bring resumption of whole fall from 1.3433. On the downside, below 1.2615 minor support will bring retest of 1.2486 low first. However, sustained break of 55 D EMA will argue that the near term trend has reversed, and targets 1.3047 resistance for confirmation.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2853) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.