{kind=link}

US financial markets basked in risk-on sentiment overnight, with S&P 500 and NASDAQ scaling new record highs. Bitcoin seized the momentum, surging past the psychologically significant $100K mark. Dubbed the “Trump Trade,” optimism over President-elect Donald Trump’s policies has returned in full force and is likely to persist, barring surprises from tomorrow’s pivotal non-farm payroll report.

Fed Chair Jerome Powell’s comments added to the upbeat tone, painting a positive picture of the economy. Additionally, the remarks suggested that he wouldn’t block another rate cut at this month’s meeting. While some Fed officials hinted at a pause in easing, a January timeframe appears more likely than December, keeping market participants optimistic about short-term monetary support.

In Asia, cautious remarks by BoJ board member Toyoaki Nakamura caused slight Yen volatility. However, as a known dove, Nakamura’s statements may not fully reflect the board’s collective stance. His clarification that he isn’t opposed to a rate hike but urges caution keeps the market’s expectations for a December or January hike split, with January remaining as the more probable choice.

Overall for the week so far, Dollar is currently the strongest performer, continuing the tight race with Yen, while Sterling ranks third. Conversely, Aussie and Kiwi lag behind, with the Euro not far ahead. The common currency was unfazed by France’s political turmoil after Prime Minister Michel Barnier’s government fell to a no-confidence vote. Swiss Franc and Loonie are steady in the middle.

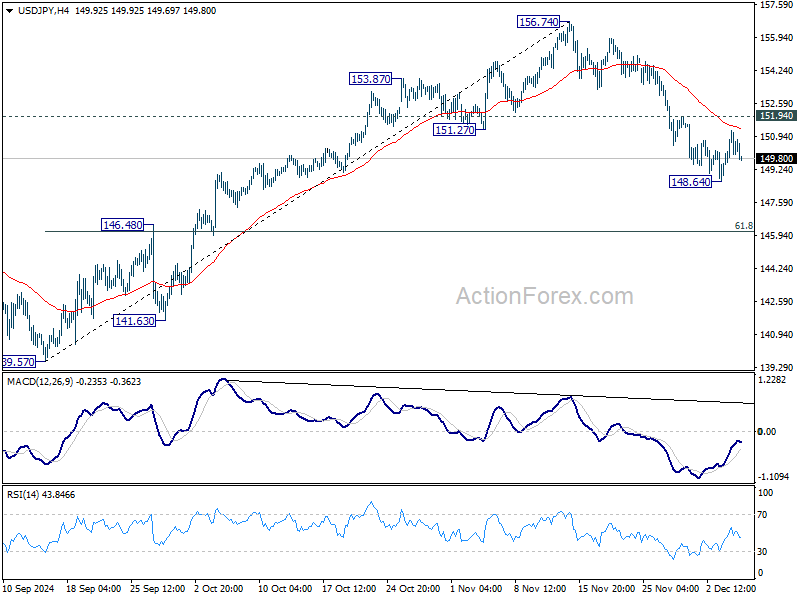

Technically, USD/JPY would be a focus for the rest of the week given the important of US NFP’s impact of stocks and yields, as well as Dollar. For now, fall from 156.74 is expected to continue as long as 151.94 resistance holds. Break of 148.64 will reinforce the view that rise from 139.57 has already completed at 156.754. Deeper fall should then be seen to 61.8% retracement of 139.57 to 156.74 at 146.12, and possibly further to retest 139.57 low. The next down move in USD/JPY, if realized, would also be used to validate the decline in other Yen pairs.

In Asia, Nikkeir rose 0.27%. Hong Kong HSI is down -1.21%. China Shanghai SSE is down -0.12%. Singapore Strait Times is up 0.53%. Japan 10-year JGB yield is up 0.0182 at 1.071. Overnight, DOW rose 0.69%. S&P 500 rose 0.61%. NASDAQ rose 1.30%. 10-year yield fell -0.043 to 4.180.

Bitcoin soars past 100k on SEC nominee optimism and Powell’s Gold comparison

Bitcoin has surged past the highly anticipated 100k milestone, riding on a wave of optimism fueled by a couple of bullish factors. In particular, with anticipation of favorable regulatory environment in the US ahead, Bitcoin could now be heading to next target at 120k.

A key driver behind Bitcoin’s leap was President-elect Donald Trump’s nomination of Paul Atkins as the next chair of the Securities and Exchange Commission. Known for his pro-crypto stance, Atkins has a track record of advocating for innovation within the financial sector and criticizing the SEC’s historically tough stance on digital asset firms. His nomination is widely seen as a signal of a more accommodative regulatory approach to cryptocurrencies.

Adding to the bullish momentum, Fed Chair Jerome Powell likened Bitcoin to gold, calling it “just like gold only it’s virtual.” He emphasized that Bitcoin is neither a primary form of payment nor a direct competitor to Dollar but rather serves as a speculative alternative to gold. While acknowledging Bitcoin’s volatility, Powell’s remarks underscored its growing legitimacy as a store of value.

The cryptocurrency’s rally also coincides with broader market strength, as NASDAQ hit fresh record highs. This parallel momentum between Bitcoin and equities highlights the increasing overlap in sentiment toward risk assets, driven by a mix of optimism around economic resilience.

Technically, near term outlook in Bitcoin will stay bullish as long as 93559 support holds. 100% projection of 24896 to 73812 from 52703 at 101619 taken out, the next target is 138.2% projection at 12304, which is slightly above 120k psychological level.

Fed’s Powell: Economy stronger than expected, allows cautious rate cuts

Fed Chair Jerome Powell expressed optimism about the US economy during an event overnight, stating it is in “very good shape” with “no reason for that not to continue.” He highlighted reduced downside risks in the labor market, stronger-than-expected growth, and inflation running slightly higher than previously anticipated.

Given these developments, Powell suggested the Fed could “afford to be a little more cautious” in its approach to cutting interest rates as it works toward a neutral policy stance.

Reflecting on Fed’s 50bos cut in September, Powell noted it was intended as “a strong signal” of support for a potentially weakening labor market. However, subsequent data revisions revealed that the economy was “even stronger than we thought”.

Fed’s Daly: No urgency as Fed calibrate policy carefully

San Francisco Fed President Mary Daly emphasized a measured approach to interest rate adjustments during a PBS News Hour interview.

She noted there’s “no sense of urgency” to lower rates quickly but highlighted the need to “carefully calibrate our policy” to align with current and expected economic conditions.

Daly added that policymakers will deliberate on the best path forward at the upcoming December 17–18 FOMC meeting.

Despite signs of economic resilience, she stressed that “there’s a lot more work for us to do” to achieve the 2% inflation target while supporting durable economic growth. Inflation remains the top challenge for many Americans.

BoJ’s Nakamura skeptical on wage and inflation sustainability

BoJ board member Toyoaki Nakamura expressed a cautious stance on monetary policy adjustments, emphasizing the need for careful calibration aligned with Japan’s economic recovery.

“We are at a state where it’s important to adjust the degree of monetary easing carefully in accordance with the economic recovery by assessing a broad array of data,” Nakamura said.

As a known dove on the BoJ board, Nakamura raised doubts about the durability of current wage hikes, saying he is “not confident” about their sustainability. He also flagged concerns about inflation, noting the possibility that the annual rate “may not reach 2% from fiscal 2025 onwards.”

In a related development, a Jiji Press report indicated growing hesitation within BoJ regarding a premature rate increase. Market expectations for a December rate hike have fallen sharply, with traders now pricing in only a 36% chance, down from 66% at the end of last week.

Looking ahead

Swiss unemployment rate, German factory orders, French industrial production, UK construction PMI, and Eurozone retail sales will be released in European session.

Later in the day, Canada will publish trade balance and Ivey PMI. US will release trade balance and jobless claims.

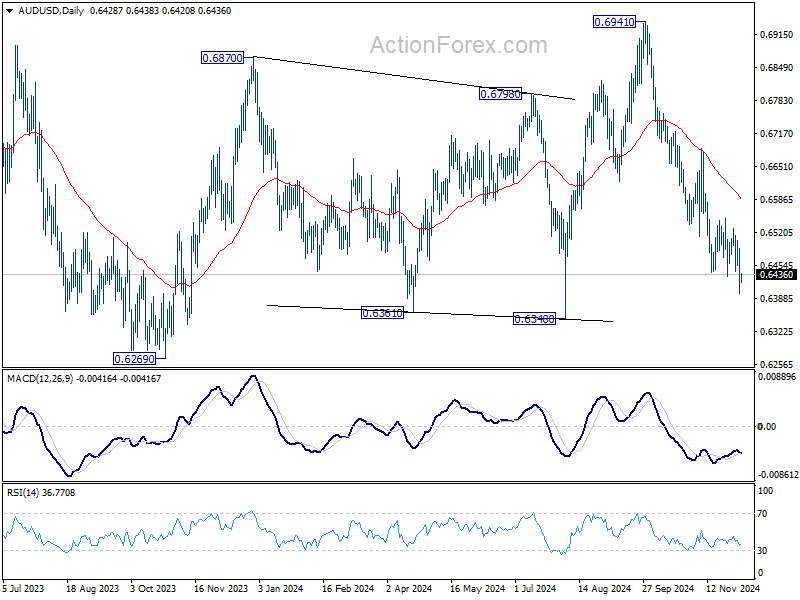

AUD/USD Daily Report

Daily Pivots: (S1) 0.6390; (P) 0.6439; (R1) 0.6479; More...

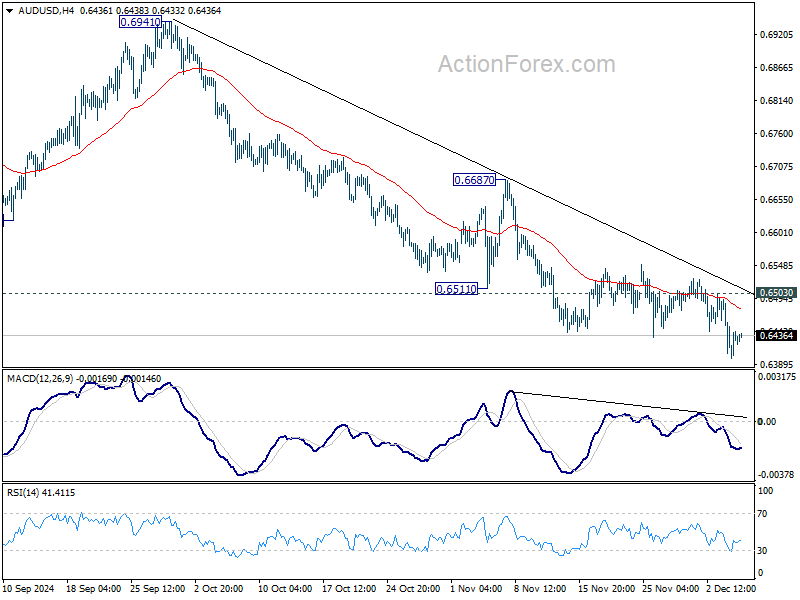

Intraday bias in AUD/USD remains on the downside for the moment. Fall from 0.6941 is in progress for 0.6348 support. Break there will target 0.6269 low next. On the upside, above 0.6503 minor resistance will turn intraday bias neutral again first.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.