{kind=link}

The forex markets are generally staying in consolidation mode today with US on thanksgiving holiday. , and even Yen’s rally is losing some momentum. Nevertheless, the Japanese currency might find some renewed life with the Tokyo CPI data in the upcoming Asian session. BoJ Governing Kazuo Ueda has recently kept the option for a rate hike in December open his comments. But all would depend on incoming data. Any stronger than expected acceleration in Tokyo CPI core would, at least, revive the speculations on BoJ.

At this point, Yen remains the strongest one for the week, followed by Swiss Franc and then Euro. The latter two will look into tomorrow’s Swiss Franc and Eurozone CPI flash to decide their final positions at the end of the week. Canadian Dollar and Australian Dollar are staying as the bottom two, followed by Dollar. Meanwhile, Kiwi and Sterling are positioning in the middle.

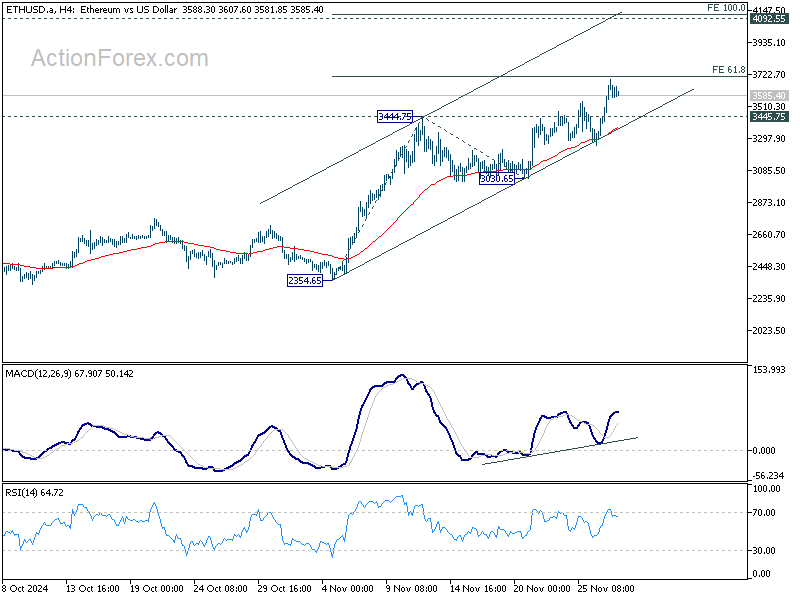

Technically, Ethereum’s near term rally resumed today and it’s now eyeing 61.8% projection of 2354.65 to 3444.75 from 3030.65 at 3704.33. Decisive break there could bring upside re-acceleration to 100% projection at 4120.785, which is slightly above 4092.55 record high. However, break of 3444.75 resistance turned support will indicate first rejection by 3700 mark, and bring pullback. Ethereum’s performance could offer clues about Bitcoin’s ability to sustain its rally and power through the key psychological 100k mark.

In Europe, at the time of writing, FTSE is up 0.11%. DAX is up 0.71%. CAC is up 0.60%. UK 10-year yield is up 0.0008 at 4.298. Germany 10-year yield is down -0.0028 at 2.137. Earlier in Asia, Nikkei rose 0.56%. Hong Kong HSI fell -1.20%. China Shanghai SSE fell -0.43%. Singapore Strait Times rose 0.79%. Japan 10-year JGB yield fell -0.0178 to 1.057.

ECB’s Lagarde advocates cheque book strategy to handle Trump’s tariff threats

In an interview with the Financial Times, ECB President Christine Lagarde proposed a measured approach to handling U.S. President-elect Donald Trump’s tariff threats, favoring a “cheque book strategy” over outright retaliation.

Trump has outlined plans for sweeping tariffs, including a 60% levy on Chinese goods and a 10-20% range on imports from other countries, including Europe. Lagarde interpreted the range as a negotiating tactic, suggesting Trump is “open to discussion.”

Lagarde expressed preference for a “cheque book strategy” over a “pure retaliation strategy.” She explained that Europe could offer to purchase certain US goods and signal readiness for constructive dialogue.

“This is a better scenario than a pure retaliation strategy, which can lead to a tit-for-tat process where no one is really a winner,” she stated.

On the inflationary effects of tariffs, Lagarde admitted the outcome remains uncertain. She explained that the net impact on inflation would depend on various factors, including GDP shifts, currency movements, the specific goods targeted, and the duration of the tariffs.

“If anything, maybe it’s a little net inflationary in the short term,” she remarked, but emphasized the difficulty of forming a conclusive view without further details.

Eurozone economic sentiment tick up to 95.8 in Nov, EU rises to 96.5

Eurozone Economic Sentiment Indicator (ESI) edged higher in November, ticking up from 95.7 to 95.8, reflecting a marginal improvement in overall sentiment. However, underlying components presented a mixed picture. Employment Expectations Indicator (EEI) declined from 99.2 to 98.9, and Economic Uncertainty Indicator (EUI) dropped from 19.0 to 18.5.

Eurozone Industrial confidence improved, rising from -12.6 to -11.1, while services confidence weakened, falling from 6.8 to 5.3. Consumer confidence also slipped, dropping from -12.5 to -13.7, while retail trade confidence improved significantly from -7.2 to -4.4. Construction confidence remained unchanged at -4.8.

Across the broader European Union, ESI rose slightly from 96.3 to 96.5, though declines were seen in key metrics like EEI, which fell from 100.1 to 99.6, and EUI, which dipped from 18.2 to 17.9. Among major EU economies, sentiment improved in France (+3.0), Spain (+2.1), the Netherlands (+1.5), and Poland (+0.7). However, Germany experienced a decline (-1.3), and Italy saw a marginal dip (-0.3).

RBA’s Bullock: Inflation to take longer to settle due to unusually tight labor market

In a speech today, RBA Governor Michele Bullock highlighted Australia’s “unusually tight” labor market. She noted that the combination of labor market pressures and demand exceeding supply across the economy would likely mean it will “take a little longer for inflation to settle at target” in Australia.

RBA staff projections anticipate inflation returning sustainably to the midpoint of the 2-3% target range, at 2.5%, by late 2026. This outlook assumes that restrictive financial conditions will gradually balance the economy and the labor market. Governor Bullock remarked, “We still think we are on the narrow path,” referencing the delicate balance required to manage inflation without derailing economic growth.

The forecast is based on market-implied cash rate expectations from the November Statement on Monetary Policy, which suggested the rate would remain steady over the near term. However, Bullock clarified, “This is not the Board’s forecast for interest rates,” but rather a “conditioning assumption” consistent with RBA’s inflation timeline.

Bullock also acknowledged uncertainties, emphasizing that the inflation forecast includes “substantial bands of error” and is subject to change as new data emerges.

RBNZ’s Silk signals slower easing path with potential pauses ahead

Assistant Governor Karen Silk indicated that RBNZ is likely to slow the pace of monetary easing and incorporate pauses into its rate cycle after February.

“There could be pauses built in, but it is definitely a slower track after February,” she noted in an interview with Bloomberg. This aligns with the bank’s updated projections released yesteday.

Silk highlighted the importance of maintaining “mildly restrictive” monetary policy to manage inflationary pressures, particularly as inflation is projected to rise to 2.5% next year.

Looking further ahead, Silk noted that RBNZ expects to be “a little closer” to the long-term neutral rate by the end of 2025. However, she emphasized that current projections do not indicate rates falling “below neutral” at any point during the forecast period.

NZ ANZ business confidence eases to 64.9, outlook continues to brighten

New Zealand’s ANZ Business Confidence dipped marginally in November, falling from 65.7 to 64.9, but it remains at what ANZ describes as an “impressive high” level. Own Activity Outlook, a key forward indicator, rose to a decade high of 48.0 from 45.9, reinforcing optimism about future economic conditions

Inflation related metrics also showed broad improvement, with cost expectations down from 64.2 to 62.9, wage expectations easing from 77.0 to 75.5, and pricing intentions falling from 44.2 to 42.2, marking the first decline in four months. Notably, inflation expectations dropped significantly from 2.83% to 2.53%.

ANZ attributed the robust activity outlook to the impact of interest rate cuts, which are “changing actual behavior, not just expectations.” While the economy remains fragile, ANZ highlighted that “things are starting to turn higher,” with improving activity suggesting early signs of recovery.

RBNZ is likely to take comfort in these trends, as “sufficient domestic disinflation pressure” appears to be in the pipeline, even if growth rebounds faster than expected. However, the survey tempered expectations for aggressive rate cuts, indicating that “large emergency cuts” may not be necessary.

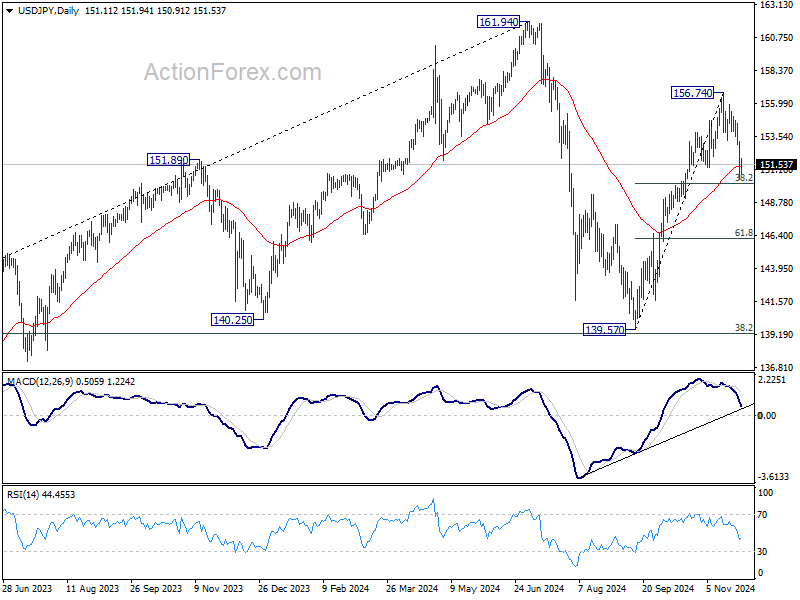

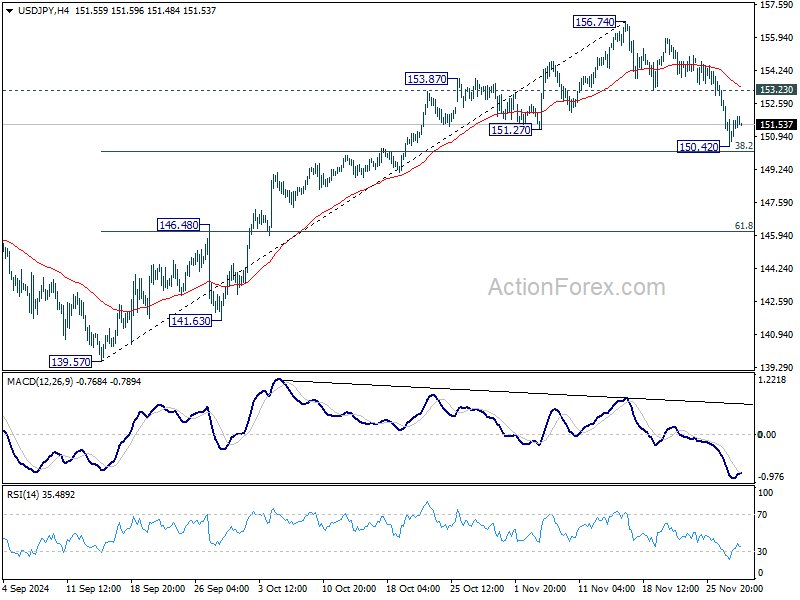

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.97; (P) 151.60; (R1) 152.75; More…

Intraday bias in USD/JPY is turned neutral with loss of momentum as seen in 4H MACD. Strong support could be seen from 38.2% retracement of 139.57 to 156.74 at 150.18 to complete the corrective fall from 156.74. On the upside, break of 153.23 support turned resistance will turn intraday bias to the upside for retesting 156.74 high. However, decisive break of 150.18 will argue that whole rise from 139.57 could have completed, and bring deeper fall to 61.8% retracement at 146.12 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.