Dollar is losing some ground as markets enter into US session, as the initial support from US President-elect Donald Trump’s tariff announcement dissipated. Although the greenback softened broadly, it is still holding onto gains against Loonie and Aussie, with traders as Trump’s tariffs are targeting Canada, China, alongside Mexico.

Market focus now turns to FOMC minutes, with traders eager to gauge sentiment among policymakers ahead of December’s rate decision. Currently, Fed fund futures indicate a 60% probability of a 25bps rate cut, but recent commentary from Fed officials has left room for doubt. The minutes may provide insight into how aligned policymakers are on easing monetary policy further or maintaining caution.

In terms of currency performance, Yen leads as the strongest performer of the day. Sterling and Euro also showed some mild strength. Meanwhile, Loonie is the weakest, pressured by trade concerns, followed by Aussie and Dollar. Swiss Franc and Kiwi are holding relatively neutral positions.

Looking ahead, the Asian session will bring two key events: RBNZ rate decision and Australia’s monthly CPI release.

RBNZ is widely expected to implement another 50bps rate cut, bringing the policy rate to 4.25%. Traders will closely examine the updated economic projections, particularly regarding additional policy easing in 2025.

On the other hand, the expected rebound in October CPI reading in Australia could reinforce RBA’s stance to delay its first rate cut from February to May next year.

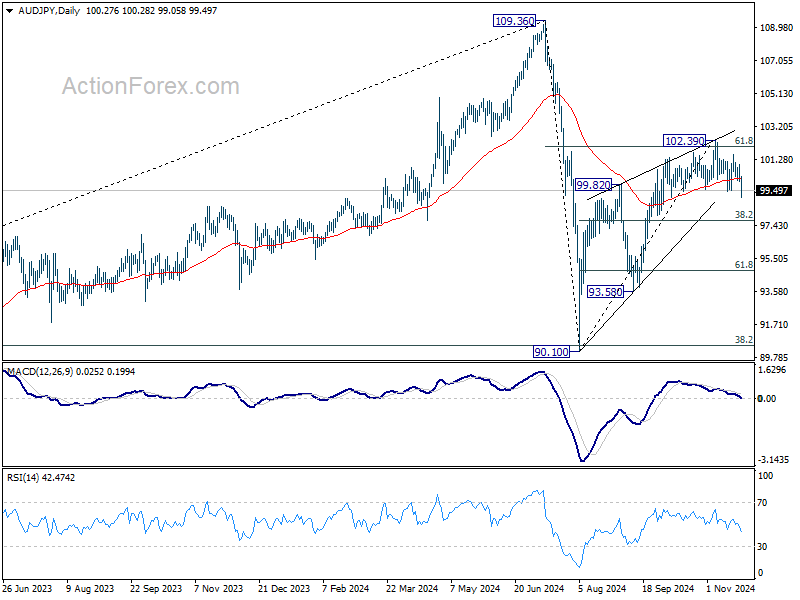

Technically, AUD/JPY’s strong break of 55 EMA should confirm short term topping at 102.39. Deeper decline is now in favor back to 38.2% retracement of 90.10 to 102.39 at 97.69. Firm break there should indicate that corrective rebound from 90.10 has completed with three waves up to 102.39. In this bearish case, deeper fall should be seen to 61.8% retracement at 94.79 and below.

In Europe, at the time of writing, FTSE is down -0.12%. DAX is down -0.27%. CAC is down -0.25%. CAC is down -0.26%. UK 10-year yield is up 0.004 at 4.351. Germany 10-year yield is down -0.011 at 2.200. Earlier in Asia, Nikkei fell -0.87%. Hong Kong HSI rose 0.04% China Shanghai SSE fell -0.12%. Singapore Strait Times fell -0.51%. Japan 10-year JGB yield fell -0.0038 to 1.070.

BoC’s Mendes signals further rate cuts, data-dependent approach

BoC Deputy Governor Rhys Mendes said in a speech today that “We no longer need interest rates to be as restrictive as they were,” which justified the larger rate reduction of 50 bps at this month’s meeting.

Inflation data for October came in at 2%, matching expectations, while preferred core inflation measures edged up to approximately 2.5%. Mendes noteds that key upcoming data points, including third-quarter GDP and November employment figures, will play a critical role in shaping the BoC’s December rate decision.

“If the economy evolves broadly in line with our forecast,” Mendes stated, “then it’s reasonable to expect further cuts to our policy rate.”

However, he emphasized that the timing and pace of any additional easing will depend on incoming data and its implications for the inflation outlook.

ECB’s de Guindos: Inflation easing, focus shifts to fragile growth

In an interview with Helsingin Sanomat, ECB Vice President Luis de Guindos acknowledged the shifting priorities of the ECB as inflation continues to decline.

Inflation is expected to return to the medium-term target of 2% by 2025. At the same time, economic growth remains very weak. So “concerns about high inflation have shifted to economic growth”. he said.

Additionally, he highlighted the rising challenges posed by “geopolitical risks” and uncertainty surrounding US. trade and fiscal policies, which could have broader implications for the Eurozone economy.

Looking ahead, ECB’s December projections will offer further clarity, but De Guindos reiterated that if current forecasts hold, the central bank will “continue making our monetary policy stance less restrictive.”

De Guindos stressed the importance of a cautious, data-driven approach in such uncertain conditions, noting that “it’s difficult to make predictions about the specific number and size of rate cuts.” However, with inflation moving closer to the medium-term target, ECB appears set to maintain its easing bias.

ECB’s Villeroy expects limited inflation impact in Europe from Trump policies

French ECB Governing Council member Francois Villeroy de Galhau highlighted the global economic risks stemming from US President-elect Donald Trump’s plans to increase tariffs and implement tax cuts. Speaking at a retail investor conference in Paris, Villeroy noted that these policies could raise inflation in the US while dampening growth internationally.

While Villeroy acknowledged that the inflationary impact on Europe would likely be “relatively limited,” he emphasized the influence on European long-term interest rates.

“Long-term interest rates set by the market have a certain tendency to cross the Atlantic,” he remarked, suggesting that US policy changes could indirectly affect Eurozone markets.

“I don’t think it changes much for European short-term rates, but long-term rates could see a transition effect,” he noted.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 153.58; (P) 154.15; (R1) 154.75; More…

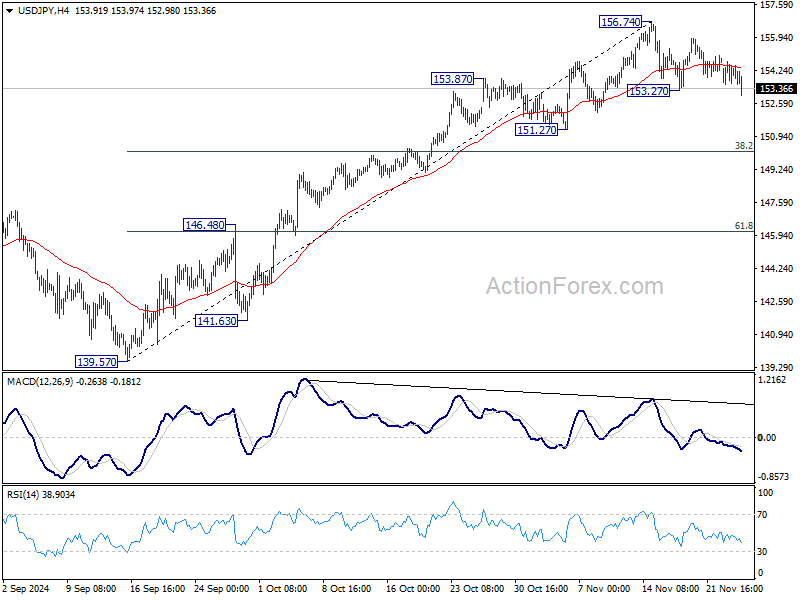

USD/JPY’s break of 153.27 minor support suggests that correction from 156.74 is extending lower. Intraday bias is back on the downside for 38.2% retracement of 139.57 to 156.74 at 150.18. For now, risk will stay on the downside as long as 156.74 resistance holds, in case of recovery.

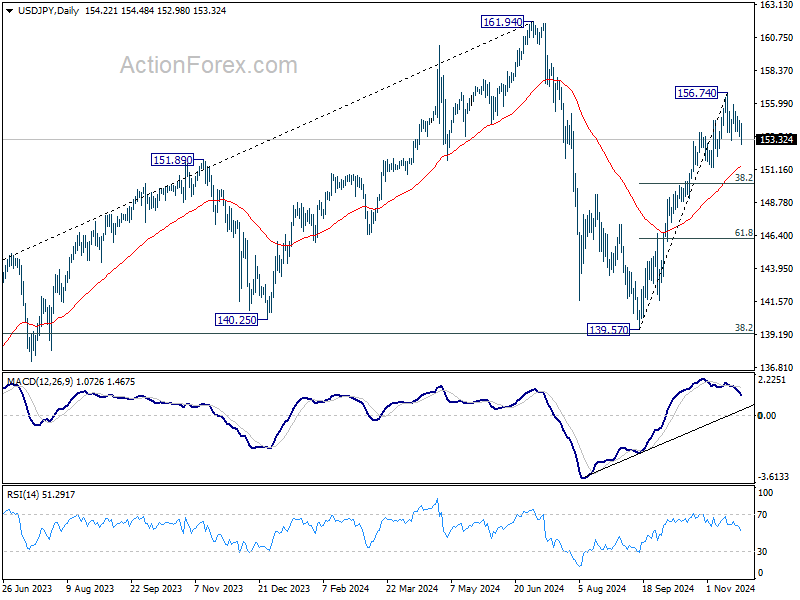

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Eco Calendar Obviously Loses Relevance in Anticipation of Tariff Announcement")

{kind=link}