{kind=link}

Following Donald Trump’s clear victory over Kamala Harris in the US presidential election, accompanied by a full Republican “Red Sweep” in Congress, US futures, Treasury yields, and the Dollar all surged sharply higher. Markets are responding favorably to expansionary fiscal policies, tax cuts, and a pro-growth agenda under the new administration. Major European indexes also rose, despite warnings from some analysts that Trump’s return may be an economic “nightmare” for Europe.

In currency markets, Dollar has jumped to a clear leadership position. Euro and Yen are currently the weakest performers, followed by Swiss Franc and Sterling. Loonie is holding second place, benefiting from its close economic ties with the US, while risk-on sentiment has kept both Kiwi and Aussie relatively resilient.

Attention now shifts to tomorrow’s rate decisions by BoE and Fed. Both central banks are widely expected to implement a 25 bps rate cut in response to softer inflationary pressures. BoE’s new economic projections, which will be released with the rate decision, could offer more clarity on the pace of policy easing going forward. For Fed, probability of another rate cut in December has slipped below 70%, as indicated by fed funds futures, reflecting increased market uncertainty.

Technically, USD/CNH also surged sharply higher today following broad based Dollar strength. Current development affirms the case that whole corrective fall from 7.3679 has completed with three waves down to 6.9709. Near term outlook will stay bullish as long as 7.0860 support holds. Next target is 7.3111 resistance. Extended weakness in offshore Yuan could exert some pressure on Chinese and Hong Kong stocks, with risk of dragging down Aussie and Kiwi.

In Europe, at the time of writing, FTSE is up 0.88%. DAX is up 0.41%. CAC is up 0.88%. UK 10-year yield is up 0.027 at 4.557. Germany 10-year yield is down -0.019 at 2.410. Earlier in Asia, Nikkei rose 2.61%. Hong Kong HSI fell -2.23%. China Shanghai SSE fell -0.09%. Singapore Strait Times rose 0.60%. Japan 10-year JGB yield rose 0.0516.

Eurozone PPI down -0.6% mom in Step, led by energy prices

Eurozone’s PPI decreased by -0.6% mom in September, slightly exceeding the expected decline of -0.5% mom. On an annual basis, PPI fell by -3.4% yoy, marginally less than the anticipated -3.5% yoy drop.

The monthly decline in Eurozone PPI was primarily driven by a significant -1.9% mom decrease in energy prices. Intermediate goods prices remained stable, while capital goods saw a slight decrease of -0.1% mom. In contrast, prices for both durable and non-durable consumer goods increased by 0.2% mom.

Across the broader EU, PPI also dropped by -0.6% mom and -3.3% yoy. Among member states, Estonia, Spain, and Romania led the monthly declines with falls of -3.6%, -2.4%, and -2.2%, respectively, while Ireland recorded a significant 4.8% increase, followed by Finland and Greece with more modest gains of 1.0% and 0.7%.

Eurozone PMI services finalized at 51.6, PMI composite at 50.0

Eurozone PMI Services for October was finalized at 51.6, up from September’s 51.4. PMI Composite also moved to 50.0 from 49.6, indicating stagnation rather than expansion across the region. The services sector continues to play a vital role in keeping Eurozone’s economy afloat, yet concerns of a Q4 contraction remain.

Spain topped the Eurozone with PMI Composite of 55.2, while Ireland followed at 52.. Italy’s index reached 51.0, a four-month high. Meanwhile, Germany’s reading improved to 48.6, still in contraction but at a three-month high. France recorded an eight-month low of 48.1.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, remarked, “The modest expansion of the services sector has been crucial in keeping the currency union out of recession.” He highlighted that declining inflation and higher wages are likely bolstering consumer spending, which sustains demand in services. However, de la Rubia pointed out that their GDP Nowcast for Q4 indicates a “slight contraction” in overall Eurozone output.

De la Rubia also noted that structural issues, such as labor shortages which exert upward wage pressures, continue to keep inflation elevated. “The ECB will find it “difficult, if not impossible”, to achieve the 2% inflation target in a sustainable manner in this environment,” he added.

BoJ minutes: Yen stabilization gives time to monitor global economic risks

Minutes from BoJ’s September meeting reveal a careful stance on monetary policy amid global economic uncertainties. At the meeting, BoJ kept its interest rate steady at 0.25%.

Regarding future direction of monetary policy, members broadly agreed that if Japan’s economic and inflation outlook aligns with their projections, the Bank would “continue to raise the policy interest rate” and gradually adjust its level of monetary accommodation.

The minutes also underscore the need for “high vigilance” given uncertainties in overseas economies, particularly in the US, and ongoing volatility in global financial markets.

Some members pointed out that recent retracements in Yen’s depreciation have moderated upside risk to inflation from import prices. Given this development, they noted that the Bank has “enough time” to evaluate the effects of global economic shifts and recent policy rate hikes before deciding on further moves.

Japan’s PMI services finalized at 49.7, first contraction since Jun

Japan’s services sector slipped into contraction in October, with PMI Services index finalized at 49.7, down from September’s 53.1 and marking its first contraction since June. PMI Composite also declined to 49.6 from 52.0, signaling a contraction in private sector activity for the first time in four months and the lowest reading since November 2023.

According to Usamah Bhatti, Economist at S&P Global Market Intelligence, the services sector’s performance “came to an abrupt halt” at the start of Q4. While the decline was modest, it was driven by a notable slowdown in new business inflows, particularly in export orders. Despite the dip, businesses maintained a positive outlook, though optimism weakened to its lowest in over two-and-a-half years, with companies citing concerns over labor shortages as a key factor.

The services sector slowdown, combined with a continuing contraction in manufacturing, contributed to the steepest private sector contraction in nearly a year. New order inflows stagnated, particularly impacted by weakened demand in manufacturing order books. Business sentiment, overall, has also softened, with optimism now at its lowest since January 2021.

NZ employment falls -0.5% in Q3, unemployment rate rises to 4.8%

New Zealand’s labor market showed signs of cooling in Q3, with employment falling by -0.5% qoq, in line with expectations. Unemployment rate rose from 4.6 to 4.8%, slightly better than the anticipated 5.0%, but still indicative of softening labor conditions.

Labor force participation rate also declined, dropping from 71.7% to 71.2%, while the employment rate slipped from 68.4% to 67.8%, reflecting fewer people actively engaged in the workforce.

On the wage front, growth showed deceleration. The labor cost index, which includes salary and wage rates with overtime, rose by 3.8% yoy, down from the previous quarter’s 4.3% yoy increase.

The slowdown in wage growth suggests some relief in wage-driven inflation pressures, which could factor into RBNZ’s upcoming rate cut.

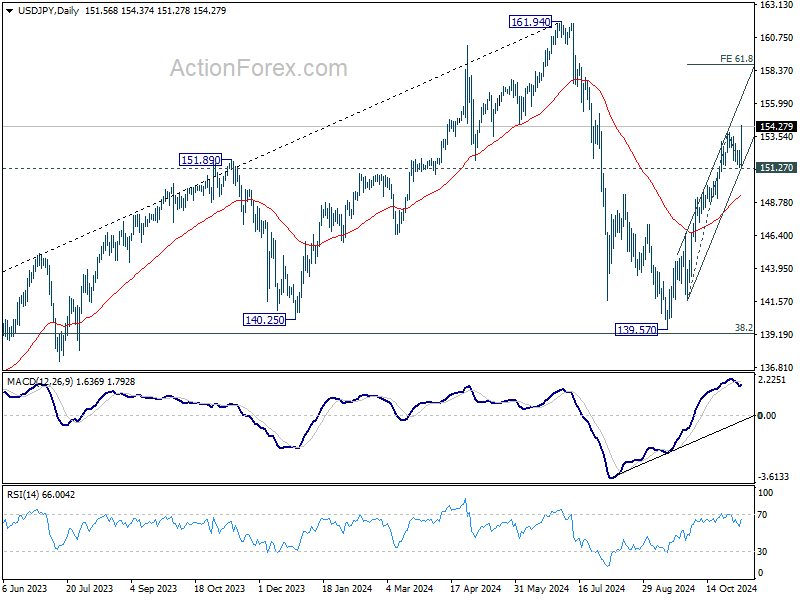

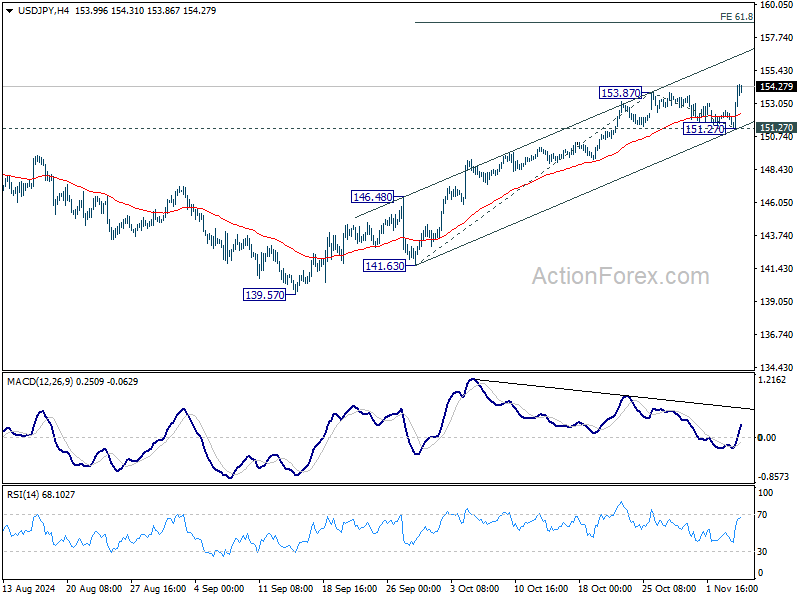

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.12; (P) 151.83; (R1) 152.32; More…

Intraday bias in USD/JPY remains on the upside for the moment. Current rally from 139.57 should target 61.8% projection of 141.63 to 153.87 from 151.27 at 158.83. For now, outlook will remain bullish as long as 151.27 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.