{kind=link}

Global markets are showing mixed performance as sentiment diverges across regions. In the US, stocks closed lower with traders displaying increased caution. ISM manufacturing report indicated continuation of the prolonged recession in the sector, though without any sharp deterioration. Attention is now focused on upcoming key economic data, including tomorrow’s ISM services report and Friday’s non-farm payrolls, both of which will help shape market sentiment. Meanwhile, the escalating tensions in the Middle East are also being closely monitored for their impact on oil prices, global supply chains, and inflationary pressures.

In contrast, Hong Kong’s market continues to rally strongly, trading up over 5% in its morning session. The city’s benchmark index has surged nearly 20% since China unexpectedly introduced a significant stimulus package last week, adding more than USD 770B in market valuation to local stocks. However, this investor optimism hasn’t spread evenly across the region. While China remains on holiday, Japan’s Nikkei index is trading lower, reflecting a more subdued regional outlook.

In the currency markets, Canadian Dollar has rebounded notably, fueled by the rise in oil prices as Middle East tensions intensify. Loonie is now the strongest performer for the week, overtaking Aussie, which has also been supported by the ongoing strength in Hong Kong’s stock market. Dollar is in third place, as traders await further direction from upcoming economic data releases.

On the other side, Yen remains the weakest performer, struggling to find momentum for a rebound. Euro follows as the second weakest currency, with more ECB officials suggesting the possibility of another 25bps rate cut this month. Swiss Franc is the third weakest, following comments from the new SNB chair indicating further rate cuts is on the horizon.

Kiwi is lagging behind other commodity-linked currencies, positioned in the middle of the pack, as economists increasingly call for a 50 bps rate cut by RBNZ next week. Sterling is trading mixed, with little notable news coming out of the UK to influence its movement.

Technically, Hong Kong HSI broke through 100% projection of 14794.16 to 19706.12 from 16964.27 at 21876.24 today with strong upside acceleration. A weekly close above this level would set the stage for further rally to 161.8% projection 24911.83. While trades appears to be reluctant to take profit at this stage, 25k handle would be very tempting, and thus a near term top could be formed there, to the the rally into a consolidation phase.

In Asia, at the time of writing, Nikkei is down -1.65%. Hong Kong HSI is up 5.99%. China is on holiday. Singapore Strait Times is up 0.34%. Japan 10-year JGB yield is down -0.0162 at 0.836. Overnight, DOW fell -0.41%. S&P 500 fell -0.93%. NASDAQ fell -1.53%. 10-year yield fell -0.59 to 3.743.

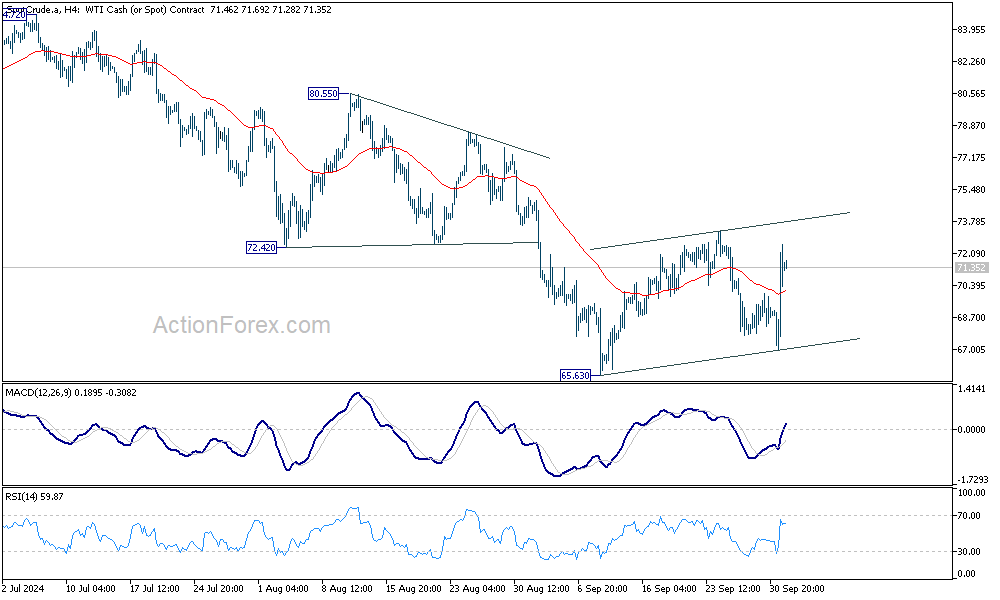

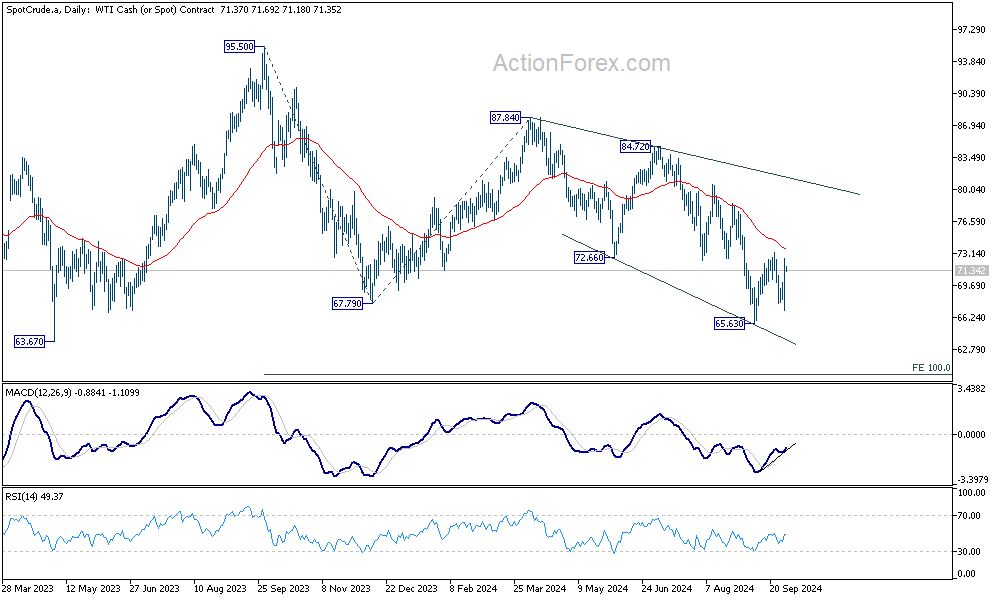

WTI surges on Middle East Conflict, but viewed as corrective move

Oil prices surged overnight, with WTI crude breaking back above 70 as tensions in the Middle East escalated. Iran launched a retaliatory strike on Israel in response to the recent killing of Hezbollah leader Hassan Nasrallah and an Iranian commander in Lebanon. This has fueled concerns that Israeli retaliation could target Iran’s oil infrastructure, posing a significant risk to global oil supplies.

As Israel shifts its focus from Gaza to Lebanon and Iran, the conflict is entering a phase with greater implications for energy markets. The prospect of disruptions in one of the world’s most critical oil-producing regions has led to heightened market anxiety, with fears of further price increases if the conflict intensifies.

Technically, despite the rebound, WTI is seen as extending the near term consolidations pattern from 65.53 only. While further rise cannot be ruled out, outlook will stay bearish as long as 55 D EMA (now at 73.72) holds. Larger down trend is still expected to extend through 65.53 to 63.67 (2023 low) at a later stage. Tentatively, the medium term target is 100% projection of 95.50 to 67.79 from 87.84 at 60.13.

However, sustained break of 55 D EMA will argue that a medium bottom was already from, and stronger rebound would be seen back towards 80 psychological level.

SNB’s Schlegel: Prepared for more rate cuts as inflation downside risks outweigh upside

At an event overnight, new SNB Chair Martin Schlegel indicated that the central bank is prepared to continue easing monetary policy if necessary to maintain medium-term price stability, and the central bank “can’t rule out negative rates either.”

Schlegel emphasized that SNB sees “downward risks to Swiss inflation as bigger than upward risks,” suggesting that deflationary pressures are a significant concern for the Swiss economy.

He also acknowledged the challenges posed by the strong Swiss franc for exporters. However, he pointed out that the primary issue facing Swiss companies is “weak foreign demand,” rather than currency strength alone.

Markets are currently pricing in an 85% probability that SNB will lower rates further by 25bps to 0.75% at its December meeting.

ECB’s Kazaks: Recent data clearly points towards Oct rate cut

ECB Governing Council member Martins Kazaks indicated that recent data “clearly point in the direction of a cut” in interest rates at the upcoming October meeting. Kazaks highlighted the increasing risks to the Eurozone economy, noting that the balance between stubborn inflation, particularly in services, and weak growth is tilting toward the latter.

He emphasized that even after another 25bps cut, which would bring the deposit rate to 3.25%, the rate would still “restricts economic activity” and curb inflation in the services sector.

Kazaks expressed concern over the “worrying” state of the economy, especially the potential for a sudden weakening of the job market. “If corporates start to shed labor, this snowball may start rolling,” he cautioned, warning of the risks of a tipping point that could exacerbate economic decline.

Looking ahead

Eurozone unemployment rate is the only feature in European session. Later in the day, US will release ADP employment.

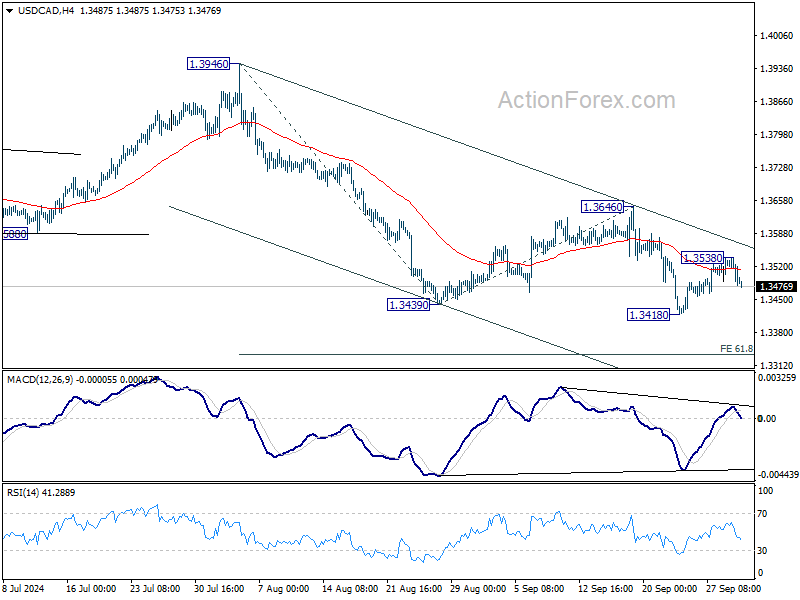

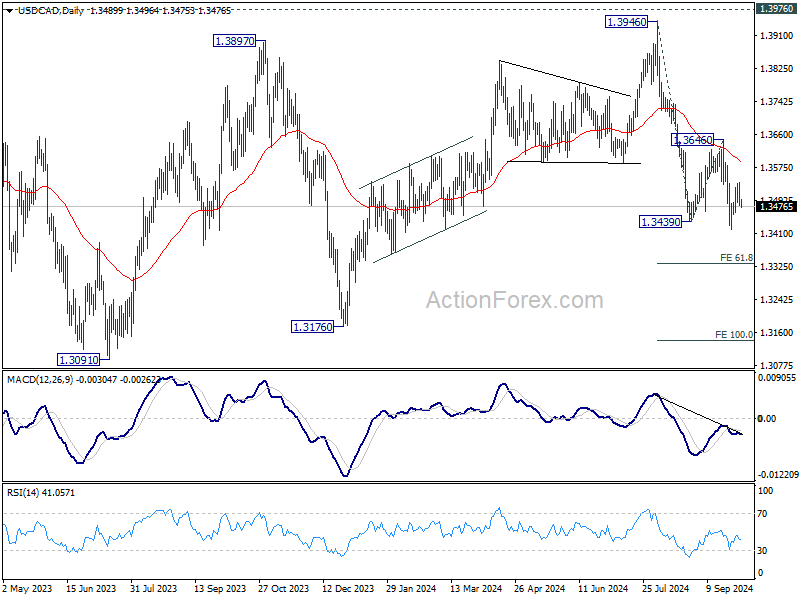

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3467; (P) 1.3504; (R1) 1.3526; More…

USD/CAD’s recovery lost momentum after breaching 55 4H EMA (now at 1.3514). But intraday bias stays neutral first, as more consolidations could be seen above 1.3418. Nevertheless, outlook will remain bearish as long as 1.3646 resistance holds. Firm break of 1.3416 will resume the fall from 1.3946 to 61.8% projection of 1.3946 to 1.3439 from 1.3646 at 1.3333.

In the bigger picture, corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Sep | -0.10% | 0.80% | 0.60% | |

| 05:00 | JPY | Consumer Confidence Sep | 37.1 | 36.7 | ||

| 09:00 | EUR | Eurozone Unemployment Rate Aug | 6.40% | 6.40% | ||

| 12:15 | USD | ADP Employment Change Sep | 120K | 99K | ||

| 14:30 | USD | Crude Oil Inventories | -1.5M | -4.5M |