{kind=link}

Forex market activity was relatively subdued during European trading hours, with Euro recovering against both Sterling and Swiss Franc despite lower-than-expected inflation reading from Germany. However, the common currency continues to face resistance in breaking out of its range against Dollar. Markets will keep a close eye on ECB President Christine Lagarde, who is set to speak, though she is not expected to provide any new policy insights. Investors are likely to maintain their focus on Eurozone inflation data later in the week for further cues on ECB policy direction.

Meanwhile, Dollar is trading sluggishly with no high-impact economic data scheduled for release today. Federal Reserve Chair Jerome Powell and Governor Michelle Bowman are due to speak, with Powell expected to maintain a neutral stance, while Bowman is likely to express caution over further monetary easing. The market’s attention remains on key income data, with the ISM reports and non-farm payrolls later in the week being the most crucial indicators for Fed’s policy outlook.

In terms of currency performance, Australian Dollar is currently leading the market, followed by New Zealand Dollar and Euro. On the weaker side, Swiss Franc is the worst performer, followed by Japanese Yen and Canadian Dollar. US Dollar and British Pound are mixed, trading in the middle of the pack.

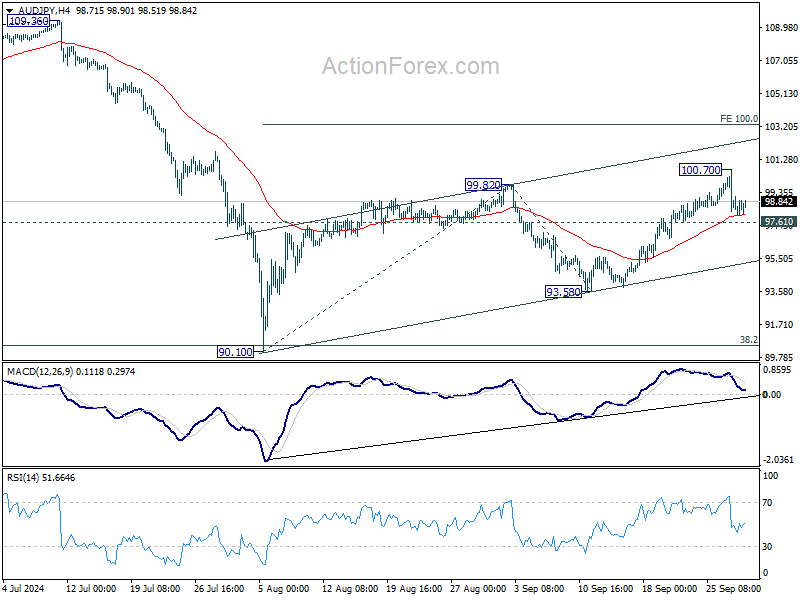

Looking ahead, AUD/JPY will be a key focus in the upcoming Asian session as BoJ releases its summary of opinions and the Tankan survey, while Australia is set to publish retail sales data. Technically, AUD/JPY’s retreat from 100.70 is contained above 97.67 minor support so far. Further rally remains in favor and break of 100.70 will resume the corrective rise from 90.10 to 100% projection of 90.10 to 99.82 from 93.58 at 103.30. However, firm break of 97.61 will suggest that the corrective rise has completed and bring deeper fall back to 93.58 support first.

In Europe, at the time of writing, FTSE is down -0.63%. DAX is down -0.75%. CAC is down -1.69%. UK 10-year yield is up 0.0316 at 4.011. Germany 10-year yield is up 0.021 at 2.157. Earlier in Asia, Nikkei fell -4.80%. Hong Kong HSI rose 2.43%. China Shanghai SSE rose 8.06%. Singapore Strait Times rose 0.33%. Japan 10-year JGB yield rose 0.0496 to 0.857.

Swiss KOF rises to 105.5, economy slowly working out of trough

Swiss KOF Economic Barometer edged higher in September, rising from 105.0 to 105.5, surpassing market expectations of 102.0. This modest increase reflects a slow but steady recovery in the Swiss economy, with KOF noting that “the Swiss economy is slowly working its way out of the trough.”

According to KOF, nearly all sectors show signs of a more favorable outlook. Manufacturing industry, in particular, has seen the most significant improvement, while financial and insurance services, construction, and other service sectors also show positive momentum.

Hospitality industry continues to maintain above-average prospects, with little change compared to prior months. On the demand side, consumer demand indicators remain stable and point to further growth. However, KOF highlighted that indicators for future foreign demand have weakened, suggesting potential challenges for Swiss exports going forward.

China’s PMI data points to continued manufacturing contraction and weakening services sector

China’s economic data for September painted a mixed picture, with manufacturing remaining in contraction and services sector losing steam.

Official NBS Manufacturing PMI edged up slightly from 49.1 in August to 49.7, above expectations of 49.5 but still below the 50-mark, signaling contraction for the fifth consecutive month. Export orders continued to weaken, with the new manufacturing export order subindex dropping from 48.7 to 47.5.

Meanwhile, NBS Non-Manufacturing PMI fell from 50.3 to 50.0, marking the end of 20 straight months of expansion. Within the non-manufacturing sectors, construction showed a marginal improvement, with its subindex rising to 50.7, but services dipped into contraction territory, falling from 50.2 to 49.9.

NBS PMI Composite rose modestly from 50.1 to 50.4. According to the NBS, extreme weather events like typhoons and the conclusion of the summer travel season significantly impacted transport, culture, and entertainment sectors.

Caixin Manufacturing PMI told a similar story, dropping from 50.4 to 49.3, the lowest reading since July 2023, while Caixin Services PMI also underperformed, falling from 51.6 to 50.3, a 12-month low. Caixin’s Composite PMI slipped from 51.2 to 50.3, reflecting broad weakness in both manufacturing and services.

Wang Zhe, senior economist at Caixin Insight Group, noted, “market conditions in the manufacturing sector worsened in September, marked by a limited expansion in supply and a significant contraction in demand.” Business confidence also fell to its “lowest level in recent years”.

NZ ANZ business confidence soars to 60.9, raising concerns of overreaction to RBNZ rate cuts

New Zealand’s ANZ Business Confidence Index saw a significant rise in September, jumping from 50.6 to 60.9, reflecting growing optimism in the business sector.

Key components of the survey also painted a positive picture. The own activity outlook rose from 37.1 to 45.3, while profit expectations surged from 8.0 to 22.2, suggesting a more upbeat economic environment.

Although cost expectations fell slightly from 68.3 to 66.8, wage expectations edged up from 75.1 to 76.4. Pricing intentions also increased from 41.0 to 42.8, while inflation expectations remained unchanged at 2.92%, marking the second consecutive month below 3%.

ANZ highlighted that this survey underscores ” the risk that the economy’s response to lower interest rates could be more vigorous than is generally expected.”

Inflation remains a concern. Firms are planning to raise prices by an average of 1.6% over the next three months, a notable increase from the June low of 1.2%. While wage growth has moderated from 4% in April to 3% now, and cost expectations have eased to 2.4%, inflationary pressures still require careful monitoring by RBNZ to ensure price stability.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1124; (P) 1.1164; (R1) 1.1202; More….

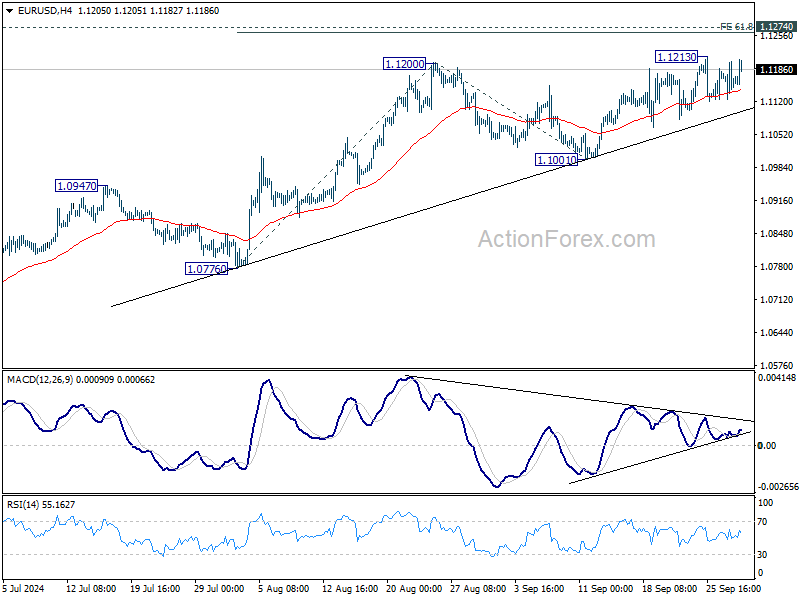

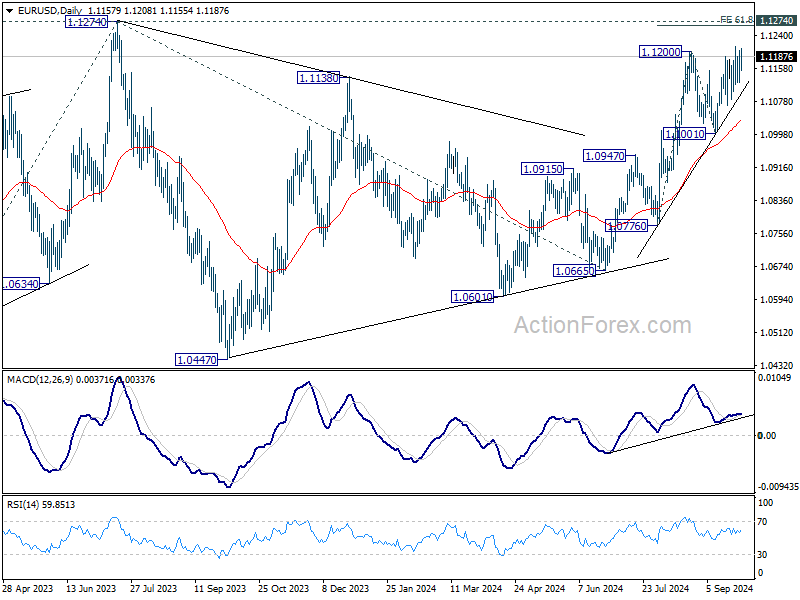

EUR/USD recovers mildly today but stays in range below 1.1213. Intraday bias remains neutral and more consolidations could still be seen. But further rally is expected as long as 1.1001 support holds. Above 1.1213 will resume the rise from 1.0665 to 1.1274 high. Firm break there will resume larger up trend. Next near term target will be 100% projection of 1.0776 to 1.1200 from 1.1001 at 1.1425.

In the bigger picture, corrective pattern from 1.1274 should have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.1001 support holds.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Aug P | -3.30% | -0.50% | 3.10% | |

| 23:50 | JPY | Retail Trade Y/Y Aug | 2.80% | 2.60% | 2.60% | |

| 01:00 | NZD | ANZ Business Confidence Sep | 60.9 | 50.6 | ||

| 01:30 | AUD | Private Sector Credit M/M Aug | 0.50% | 0.50% | 0.50% | |

| 01:30 | CNY | NBS Manufacturing PMI Sep | 49.8 | 49.5 | 49.1 | |

| 01:30 | CNY | NBS Non-Manufacturing PMI Sep | 50 | 50.4 | 50.3 | |

| 01:45 | CNY | Caixin Manufacturing PMI Sep | 49.3 | 50.5 | 50.4 | |

| 01:45 | CNY | Caixin Services PMI Sep | 50.3 | 51.5 | 51.6 | |

| 05:00 | JPY | Housing Starts Y/Y Aug | -5.10% | -3.00% | -0.20% | |

| 06:00 | EUR | Germany Import Price Index M/M Aug | -0.40% | -0.30% | -0.40% | |

| 06:00 | GBP | GDP Q/Q Q2 F | 0.50% | 0.60% | 0.60% | |

| 07:00 | CHF | KOF Economic Barometer Sep | 105.5 | 102 | 101.6 | 105 |

| 08:30 | GBP | M4 Money Supply M/M Aug | -0.10% | 0.20% | 0.30% | |

| 08:30 | GBP | Mortgage Approvals Aug | 65K | 64K | 62K | |

| 12:00 | EUR | Germany CPI M/M Sep P | 0.00% | 0.10% | -0.10% | |

| 12:00 | EUR | Germany CPI Y/Y Sep P | 1.80% | 1.90% | 1.90% | |

| 13:45 | USD | Chicago PMI Sep | 46.5 | 46.1 |