{kind=link}

Dollar bears attempted to push the greenback lower following the release of much weaker-than-expected ADP employment data, but the downward momentum lacked conviction. Traders remain cautious, given that ADP data has not consistently aligned with non-farm payrolls, leaving room for surprises when the NFP is released tomorrow. Furthermore, today’s upcoming ISM services report could still turn market sentiment, adding to the uncertainty surrounding the Dollar’s immediate direction.

Meanwhile, the drop in benchmark treasury yields in both the US and Europe has become more pronounced. This has bolstered Yen, making it the strongest currency of the day so far The New Zealand Dollar is also performing well, followed by Euro, which managed to shake off negative sentiment from the weak German economic outlook highlighted by the ifo institute. At the other end of the spectrum, Canadian Dollar is the weakest performer so far, with Dollar and Australian Dollar not far behind. Meanwhile, British Pound and Swiss Franc are holding steady in the middle of the pack.

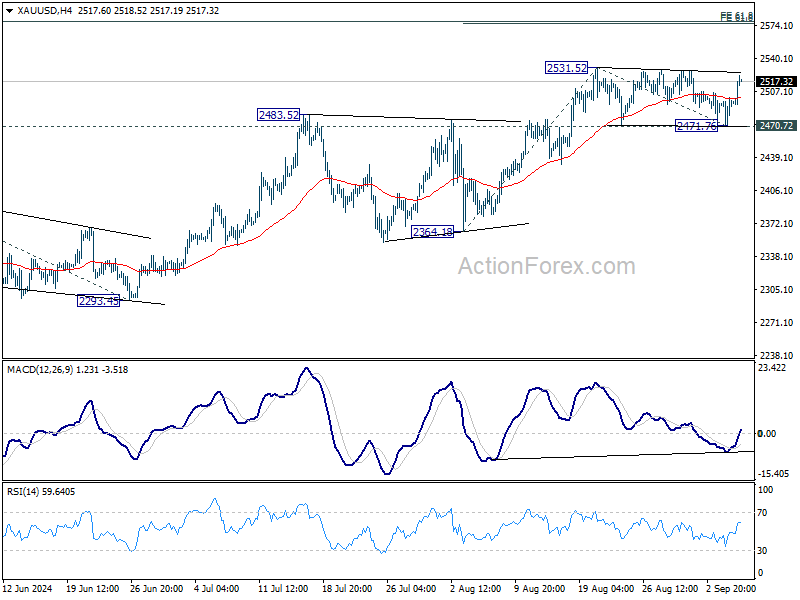

Technically, Gold’s strong bounce today is strengthening the case that consolidation from 2531.52 has completed at 2471.76. Focus is now on 2531.52 high. Firm break there will confirm up trend resumption for 61.8% projection of 2364.18 to 2531.52 from 2471.76 at 2575.17 next.

In Europe, at the time of writing, FTSE is down -0.07%. DAX is up 0.13%. CAC is down -0.62%. UK 10-year yield is down -0.0445 at 3.902. Germany 10-year yield is down -0.0297 at 2.198. Earlier in Asia, Nikkei fell -1.05%. Hong Kong HSI fell -0.07%. China Shanghai SSE rose 0.14%. Singapore Strait Times rose 0.50%. Japan 10-year JGB yield fell -0.0145 to 0.875.

US initial jobless claims falls to 227k vs exp 233k

US initial jobless claims fell -5k to 227k in the week ending August 31, lower than expectation of 233k. Four-week moving average of initial claims fell -2k to 230k.

Continuing claims fell -2k to 1838k in the week ending August 24. Four-week moving average of continuing claims fell -82k to 1853k.

US ADP employment misses expectations with only 99k jobs added in Aug

ADP report revealed that US private employment grew by 99k in August, falling short of the expected 150k. The job gains were spread unevenly across sectors, with goods-producing jobs rising by 27k and service-providing jobs adding 72k. Among establishment sizes, small businesses lost -9k jobs, while medium-sized companies added 68k, and large firms contributed 42k new positions.

Annual pay growth for workers staying in their jobs at 4.8% yoy and for job changers at 7.3% yoy, both unchanged from the previous month.

Nela Richardson, chief economist at ADP, commented, “The job market’s downward drift brought us to slower-than-normal hiring after two years of outsized growth.” She added that wage growth, which has begun to stabilize following a post-pandemic surge, will be the next key indicator to monitor.

ifo: German economy stuck in crisis, expected to stagnate in 2024

In its Autumn Economic Forecast, ifo stated that German economy remains in “stuck in crisis”, impacted by both economic and structural challenges. Following last year’s -0.3% contraction, the country’s price-adjusted GDP is expected to “only stagnate” in 2024.

A “gradual recovery” is anticipated over the next two years, with growth projected at 0.9% in 2025 and 1.5% in 2026. However, these figures mark a significant downgrade from the ifo Economic Forecast Summer 2024, with growth estimates cut by -0.4% for this year and by -0.6% for 2025.

Despite initial hopes for improvement, both industrial activity and consumer spending are emerging “very slowly from their stagnation,” according to the report.

Eurozone retail sales rises 0.1% mom in Jul, EU up 0.2% mom

In July, Eurozone retail sales volumes rose by 0.1% mom, in line with market expectations. The growth was primarily supported by a 0.4% rise in sales of food, drinks, and tobacco, alongside a 0.1% uptick in non-food products, excluding automotive fuel. However, automotive fuel sales in specialized stores declined by -1.0%, offsetting some of the overall growth.

Across the broader EU, retail sales increased by 0.2% mom in July. Among EU member states, Croatia saw the highest monthly gain in retail trade volume, up 2.9%, followed by Austria and Slovakia at +1.8%, and Slovenia at +1.6%. On the other hand, Luxembourg recorded the largest drop in retail sales, down -2.1%, with Romania (-1.8%) and Cyprus (-1.1%) also posting significant declines.

Real wages rise for second month in Japan, boosted by summer bonuses

Japan’s real wages rose by 0.4% yoy in July, down from June’s 1.1% yoy, but still marking the second consecutive month of growth after 27 months of decline.

Nominal wages increased by 3.6% yoy, surpassing expectations of 3.1%, but slowing from June’s 4.5% yoy. Regular pay, which rose 2.7% yoy, achieved its fastest growth in nearly 32 years. However, overtime pay, often seen as a gauge of corporate strength, dipped slightly by -0.1% yoy.

Special payments, such as bonuses, played a significant role in lifting wage growth during the summer, with a 6.2% yoy increase in July, following a 7.8% yoy rise in June.

A labor ministry official noted, “From August and thereafter, monthly wages will be a deciding factor” in sustaining real wage growth, as the contribution from special payments will diminish in the coming months.

BoJ board member Hajime Takata said in a speech today:

If inflation moves roughly in line with forecasts, and companies continue to boost spending, wages and pass on costs through price hikes, then “we need to adjust the degree of monetary easing further,”

While US and European central banks are moving toward rate cuts, the effect of their past aggressive monetary tightening could appear with a lag and weigh on Japan’s economy, Takata said.

The difference in monetary policy stance between that of the BOJ and other central banks could also cause market turbulence, Takata said. “As such, we must carefully monitor domestic and overseas developments,” he said.

The stock and currency market saw big volatility in early August and “the fallout continues”. As such, we need to scrutinise market developments and their impact.

RBA’s Bullock reiterates no rate cuts soon, stresses vigilance on inflation risks

In a speech today, RBA Governor Michele Bullock reaffirmed that the central bank is unlikely to cut interest rates in the near term, provided the economy evolves as anticipated.

Bullock emphasized that the Board remains “vigilant to upside risks to inflation” and that monetary policy will need to stay “sufficiently restrictive” until there is clear evidence that inflation is moving sustainably towards the target range.

Although inflation has fallen significantly from its peak, it remains above the midpoint of RBA’s 2–3% target range, with underlying inflation, as measured by the trimmed mean, still at 3.9% in June.

RBA aims to bring inflation back to target without jeopardizing the labor market gains made in recent years, navigating what Bullock described as the “narrow path.”

The central bank’s August forecast anticipates underlying inflation returning to the target range by the end of 2025, a “slightly slower” timeline than previously projected. While the labor market remains relatively tight, Bullock noted that it is expected to “ease gradually” over the next few years as the economy adjusts.

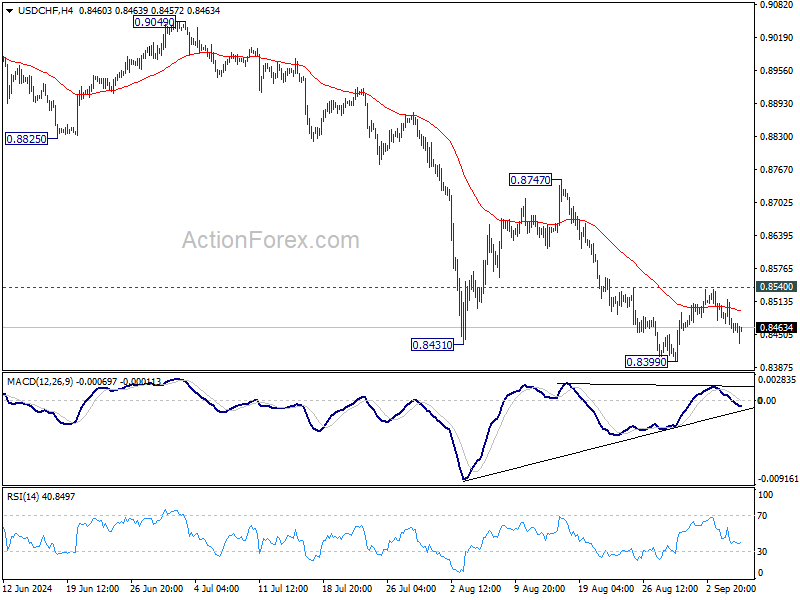

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8446; (P) 0.8482; (R1) 0.8502; More…

USD/CHF is still holding in range above 0.8399 despite today’s decline. Intraday bias stays neutral for the moment. With 0.8540 resistance intact, further decline is expected. On the downside, break of 0.8339 will resume the fall from 0.9223 and target 0.8332 low. However, considering bullish convergence condition in 4H MACD, firm break of 0.8540 will confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance instead.

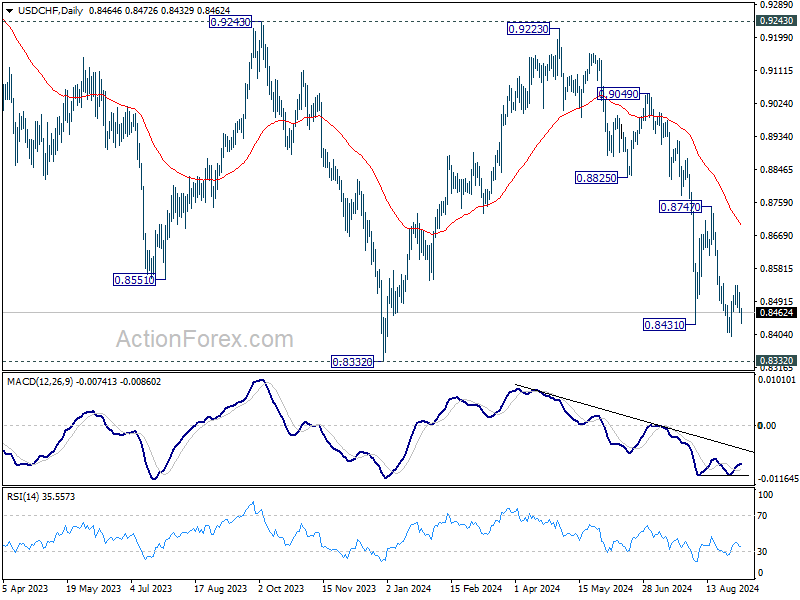

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Jul | 3.60% | 3.10% | 4.50% | |

| 01:30 | AUD | Trade Balance (AUD) Jul | 6.01B | 4.95B | 5.59B | 5.43B |

| 05:45 | CHF | Unemployment Rate Aug | 2.50% | 2.50% | 2.50% | |

| 06:00 | EUR | Germany Factory Orders M/M Jul | 2.90% | -1.50% | 3.90% | |

| 08:30 | GBP | Construction PMI Aug | 53.6 | 54.4 | 55.3 | |

| 09:00 | EUR | Eurozone Retail Sales M/M Jul | 0.10% | 0.10% | -0.30% | |

| 11:30 | USD | Challenger Job Cuts Y/Y Aug | 1.00% | 9.20% | ||

| 12:15 | USD | ADP Employment Change Aug | 99K | 150K | 122K | 111K |

| 12:30 | USD | Initial Jobless Claims (Aug 30) | 227K | 233K | 231K | 232K |

| 12:30 | USD | Nonfarm Productivity Q2 | 2.50% | 2.30% | 2.30% | |

| 12:30 | USD | Unit Labor Costs Q2 | 0.40% | 0.90% | 0.90% | |

| 13:45 | USD | Services PMI Aug F | 55.2 | 55.2 | ||

| 14:00 | USD | ISM Services PMI Aug | 51.5 | 51.4 | ||

| 14:30 | USD | Natural Gas Storage | 26B | 35B | ||

| 15:00 | USD | Crude Oil Inventories | -0.6M | -0.8M |