{kind=link}

In relatively quiet market environment, Japanese Yen is coming under increasing pressure, with notable selloff driven by rising benchmark yields in the US and Europe. With major European stock indexes largely flat and the US and Canadian markets closed for a holiday, the Yen’s decline has gained momentum. Several Yen crosses have broken near term resistance levels, signaling that the currency’s weakness could extend further until markets fully reopen and liquidity improves tomorrow.

This week, while the spotlight remains on US non-farm payrolls report, significant attention will also be directed toward Switzerland’s economic data, including CPI and GDP figures set to be released tomorrow. These data points are crucial as SNB is expected to cut interest rates for the third consecutive meeting on September 26. However, the magnitude of this rate cut is uncertain and will heavily depend on whether the Swiss economy can sustain its growth momentum in the second quarter.

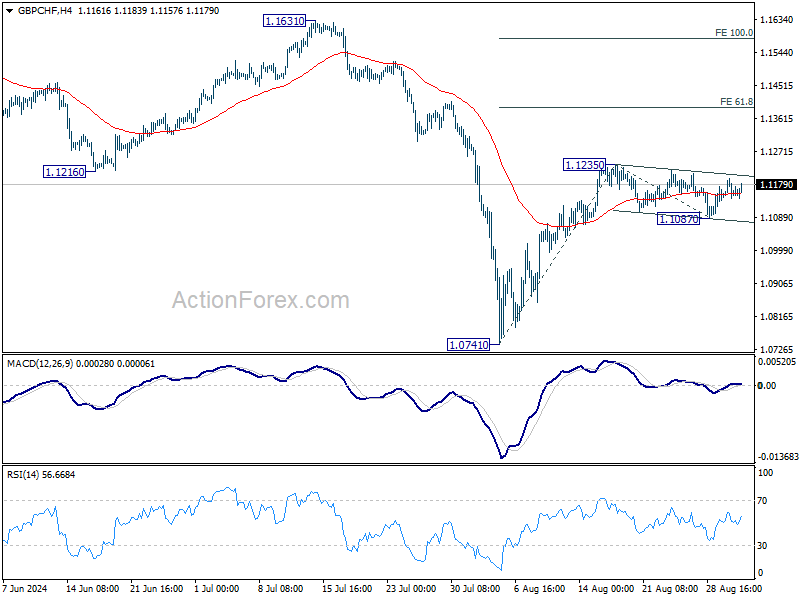

Technically, GBP/CHF’s price actions from 1.1235 are clearly corrective. It’s plausible that the pullback has completed with three waves down to 1.1087 already. Break of 1.1235 will resume the whole rebound from 1.0741 to 61.8% projection of 1.0741 to 1.1235 from 1.1087 at 1.1139 in the near term.

In Europe, at the time of writing, FTSE is down -0.07%. DAX is down -0.07%. CAC is down -0.03%. UK 10-year yield is up 0.020 at 4.028. Germany 10-year yield is up 0.029 at 2.332. Earlier in Asia, Nikkei rose 0.14%. Hong Kong HSI fell -1.65%. China Shanghai SSE fell -1.10%. Singapore Strait Times rose 0.59%. Japan 10-year JGB yield is up 0.0182 at 0.912.

UK PMI manufacturing finalized at 26-month high, strong domestic demand but export challenges persist

UK PMI Manufacturing was finalized at 52.5 in August, up from July’s 52.1, and 26-month high. Growth was broad-based across sectors, with strong domestic demand driving new contract wins. This domestic strength helped offset the continued decline in export orders, which have been falling steadily since early 2022.

Rob Dobson, Director at S&P Global Market Intelligence, noted that manufacturing remained a “positive contributor” to the UK economy, with solid growth in output, new orders, and the strongest job creation in over two years. The investment goods sector led the upturn.

However, the sector faces ongoing challenges in exports, with weaker demand from Europe and China, along with issues like freight delays, high shipping costs, and political uncertainty, hampering overseas sales.

These challenges are also disrupting supply chains, leading to longer delivery times and driving up input costs, which saw another sharp increase in August.

Eurozone PMI manufacturing finalized at 45.8, decline persists with rising prices adding pressure on ECB

Eurozone’s manufacturing sector remains entrenched in contraction, with PMI Manufacturing index finalized at 45.8 in August, unchanged from July’s reading. This marks the third consecutive month of significant decline, indicating that the sector is still mired in a prolonged downturn. Despite a continued drop in new orders, both domestic and international, goods prices have risen for the first time since April 2023, adding to the growing challenges faced by ECB.

Country-specific PMI data reveals mixed performance. Greece led the pack with a PMI of 52.9, although this marked an eight-month low. Spain and Ireland managed to stay slightly above the neutral 50.0 mark, with readings of 50.5 and 50.4, respectively, but both hit multi-month lows. On the other hand, Italy’s PMI improved to 49.4, its highest in five months, although it remains in contraction. France reported a 7-month low of 43.9 while Germany recorded a PMI of 42.4, a 5-month low.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted the worsening conditions, stating, “Things are going downhill, and fast.” The manufacturing sector has now been in recession for a grueling 26 months, with no immediate signs of recovery. The persistent decline in new orders has dashed hopes of a near-term rebound, while the recent uptick in input prices since June suggests that the deflationary phase in the goods sector may be ending.

For the first time since April 2023, selling prices in the manufacturing sector have risen, driven by increases in countries like France, the Netherlands, Greece, and Italy. This development could complicate ECB’s efforts to control inflation, as the central bank has been relying on falling manufacturing prices to offset persistent inflationary pressures in the services sector.

Japan’s PMI manufacturing finalized at 49.8, close to stabilization amid rising cost burdens

Japan’s Manufacturing PMI for August was finalized at 49.8, showing a slight improvement from July’s 49.1, but still indicating a marginal contraction. S&P Global noted that the sector is moving closer to stabilization, with a renewed rise in production. This marks the first increase in purchasing activity in two years.

According to Usamah Bhatti at S&P Global Market Intelligence, the latest figures paint a “mixed picture” as the sector hovers near stabilization. The renewed rise in production and a softer decline in new orders have encouraged firms to increase staffing levels, while the pace of destocking has slowed. Additionally, there have been signs of improved supplier performance, particularly in the availability of inputs like electrical components.

However, the data also pointed to significant cost pressures, with the strongest rise in input costs since April 2023. Despite this, companies have been reluctant to pass these higher costs onto customers fully, leading to the slowest rate of charge inflation since mid-2021.

China’s Caxin PMI manufacturing rises to 50.4, modest return to expansion

China’s Caixin PMI Manufacturing rose slightly in August, reaching 50.4 from July’s 49.8, signaling a modest return to expansion. The improvement reflects faster output growth and stabilization in employment after an 11-month decline. Meanwhile, average selling prices and input costs continued to decline, indicating ongoing deflationary pressures within the sector.

Wang Zhe, Senior Economist at Caixin Insight Group, noted that while PMI manufacturing returned to expansionary territory, the growth remains “limited”. He highlighted the significant challenges China faces in stabilizing its economic growth, particularly given the government’s ambitious annual targets. Key issues include weak domestic demand, uncertainties in external demand, and low market optimism, all of which could hinder sustained growth.

In contrast, the official NBS data released over the weekend painted a more subdued picture. NBS PMI Manufacturing fell from 49.5 to 49.1 in August, indicating a deeper contraction in the sector. While PMI Non-Manufacturing ticked up slightly from 50.1 to 50.3, the PMI Composite dropped for the fifth consecutive month, landing at 50.1—the lowest since December 2022.

NBS statistician Zhao Qinghe attributed the decline in manufacturing to several factors, including extreme weather, off-season production in certain industries, insufficient demand, and fluctuations in commodity prices.

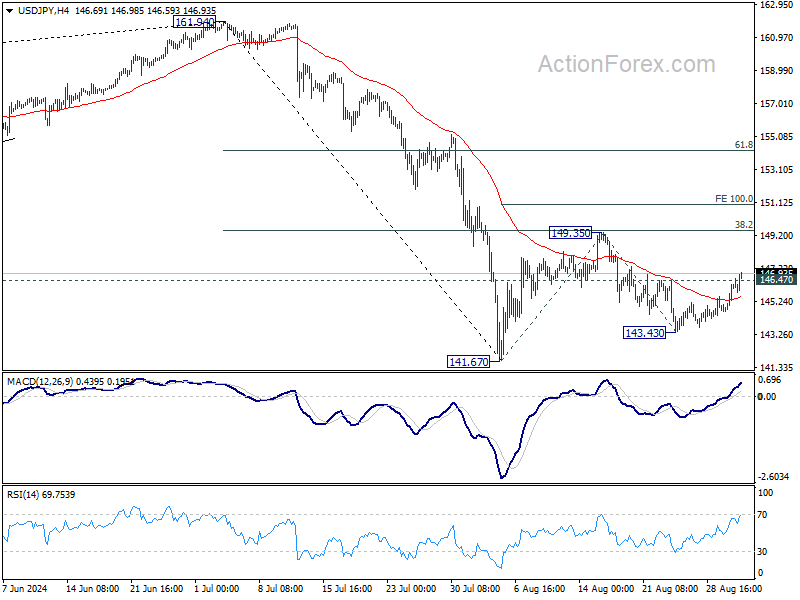

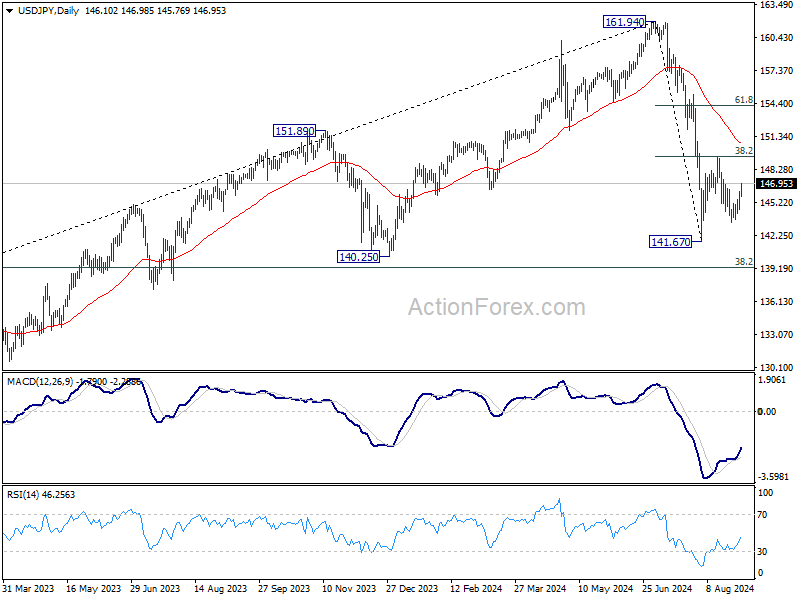

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.13; (P) 145.69; (R1) 146.72; More…

USD/JPY’s break of 146.47 resistance suggests that pull back from 149.35 has already completed at 143.43. More importantly, rebound from 141.67 could be ready to resume. Intraday bias is back on the upside for 149.35 resistance first. Firm break there will target 100% projection of 141.67 to 149.35 from 143.43 at 151.11, as the second leg of the corrective pattern from 161.94 high. For now, risk will stay on the upside as long as 143.43 support holds, in case of retreat.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.47) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Capital Spending Q2 | 7.40% | 9.90% | 6.80% | |

| 00:30 | JPY | Manufacturing PMI Aug F | 49.8 | 49.5 | 49.5 | |

| 01:30 | AUD | Company Gross Operating Profits Q/Q Q2 | -5.30% | -0.40% | -2.50% | |

| 01:30 | AUD | Building Permits M/M Jul | 10.40% | 2.40% | -6.50% | -6.40% |

| 01:45 | CNY | Caixin Manufacturing PMI Aug | 50.4 | 50 | 49.8 | |

| 06:30 | CHF | Retail Sales Y/Y Jul | 2.70% | -0.20% | -2.20% | -2.60% |

| 07:30 | CHF | Manufacturing PMI Aug | 49.0 | 43.7 | 43.5 | |

| 07:50 | EUR | France Manufacturing PMI Aug F | 43.9 | 42.1 | 42.1 | |

| 07:55 | EUR | Germany Manufacturing PMI Aug F | 42.4 | 42.1 | 42.1 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Aug F | 45.8 | 45.6 | 45.6 | |

| 08:30 | GBP | Manufacturing PMI Aug F | 52.5 | 52.5 | 52.5 |