{kind=link}

Yen’s rally accelerates again in Asian session today, driven by stronger-than-expected PMI services data, which bolsters the argument for a BoJ rate hike next week. While opinions vary on the exact timing of the rate move, with some economists forecasting a move in September or October, all would agree that an early hike this month is a distinct possibility. Reports indicate that the BoJ board might delay the decision until the last minute, contingent on retail sales data scheduled on the same day to confirm if this year’s substantial wage hikes are boosting consumption.

The broader currency markets reflect a risk-off sentiment. Dollar, following Yen, ranks as the second strongest currency for the week, while Swiss Franc holds the third position. In contrast, Australian Dollar remains the weakest, followed by New Zealand Dollar and Canadian Dollar, which awaits today’s BoC rate cut decision. Euro and Sterling are positioned in the middle.

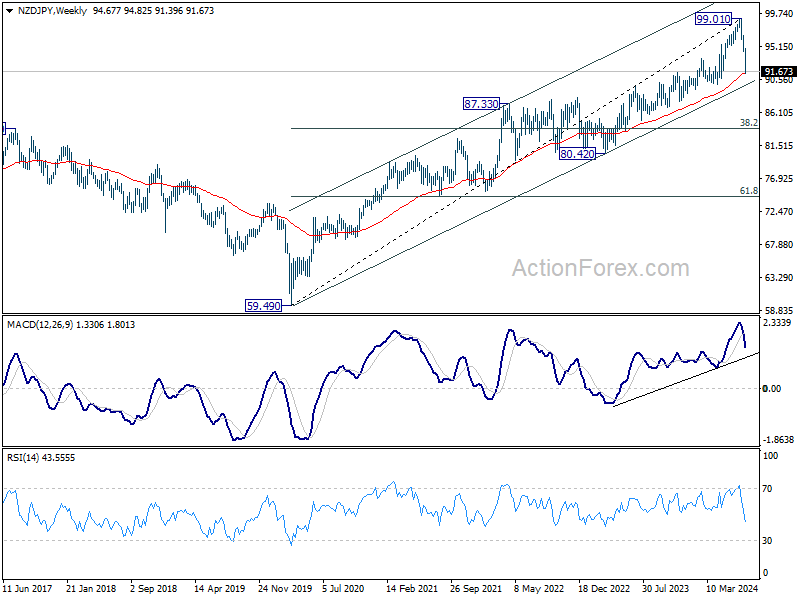

Technically, NZD/JPY is pressing 55 W EMA (now at 91.40) as the fall from 99.01 accelerates this week. Downside potential could be limited as the cross will also approach long term channel support (now at around 89.77). A bounce on oversold condition in daily chart should be due shortly. However, decisive break of 90 psychological level would signal that NZD/JPY is at least correcting whole up trend from 59.49 (2020 low), with risk of bearish reversal. That would set up deeper fall to 38.2% retracement of 59.49 to 99.01 at 83.91 in medium term.

In Asia, at the time of writing, Nikkei is down -0.94%. Hong Kong HSI is down -0.64%. China Shanghai SSE is down -0.17%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is up 0.0062 at 1.069. Overnight, DOW fell -0.14%. S&P 500 fell -0.16%. NASDAQ fell -0.06%. 10-year yield fell -0.021 to 4.239.

Australia’s PMI composite dips to 50.8, no major slowdown with continued inflation pressures

Australia’s PMI Manufacturing saw a marginal improvement in July, rising slightly from 47.2 to 47.4. Conversely, PMI Services dropped to a six-month low, moving from 51.2 to 50.8. PMI Composite also decreased from 50.7 to 50.2, the lowest in six months.

Warren Hogan, Chief Economic Advisor at Judo Bank, highlighted that despite a further moderation in the composite output index, “there are no signs of a significant slowdown in Australian business activity in 2024.” He noted that while manufacturing continues to struggle, services sector is still experiencing better activity compared to the end of 2023.

Hogan also mentioned that the impact of recent tax cuts and cost-of-living support measures has yet to fully manifest in the business conditions and should positively affect consumer spending in future months. Insights from the upcoming final PMIs for July and the reports for August are expected to provide a clearer picture of these effects.

Despite softer activity levels, inflation pressures have not eased significantly. The services sector saw a notable increase in input costs, which rose four points to 63.3—the highest since November 2023. In contrast, manufacturing input costs rose only slightly and are near their lowest in four years. The composite output price index nudged up to 54.1 in July, indicating a small increase but suggesting that inflation is likely stabilizing around an annualized rate of 4% as of mid-2024.

Japan’s PMI services surges to 53.9 while manufacturing back in contraction

Japan’s PMI Manufacturing declined from 50.0 to 49.2, underperforming against expectations of 50.5, indicating contraction. In contrast, PMI Services experienced a robust increase, rising sharply from 49.4 to 53.9, signaling a strong expansion and the highest activity level in three months. PMI Composite also rose from 49.7 to 52.6.

Usama Bhatti, Economist at S&P Global Market Intelligence, stating the reading was “indicative of solid growth,” driven primarily by the services sector. Manufacturing saw a “renewed reduction in output,” though the decline was marginal.

Additionally, the PMI report highlighted increasing operational challenges, with a “renewed increase in capacity pressures” across the private sector. For the first time in three months, there was a rise in the level of outstanding business, suggesting that firms are facing more backlog in their operations.

The report also underscored persistent cost pressures, particularly in manufacturing, where input prices rose sharply, marking the steepest increase since April 2023.

BoC to cut rates again; USD/CAD set for further gains

BoC is widely anticipated to cut its interest rate by 25bps to 4.50% today, the second reduction in a row. This expectation is strongly backed by financial markets, which are pricing in nearly a 93% probability. While the decision itself seems almost certain, the market’s attention will be on BoC’s guidance regarding the pace of future monetary easing.

A recent Reuters survey sheds light on the expected path of rate cuts. Out of 30 economists surveyed, 16 foresee two additional rate cuts this year, likely in October and December, which would bring the rate down to 4.00%. Ten economists predict just one more cut to 4.25%, while four expect a total of three additional cuts, taking the rate to 3.75%.

USD/CAD has been surging this week, driven in part by the broad selloff in commodity currencies, including Loonie. Additionally, there is backdrop of expectations that Fed will cut rates twice this year. Additionally, the potential return of Donald Trump to US presidency raises prospects of slower policy easing next year. In contrast, BoC is anticipated to ease policy more quick and deeper than Fed, while it has already commenced its cycle of rate cuts.

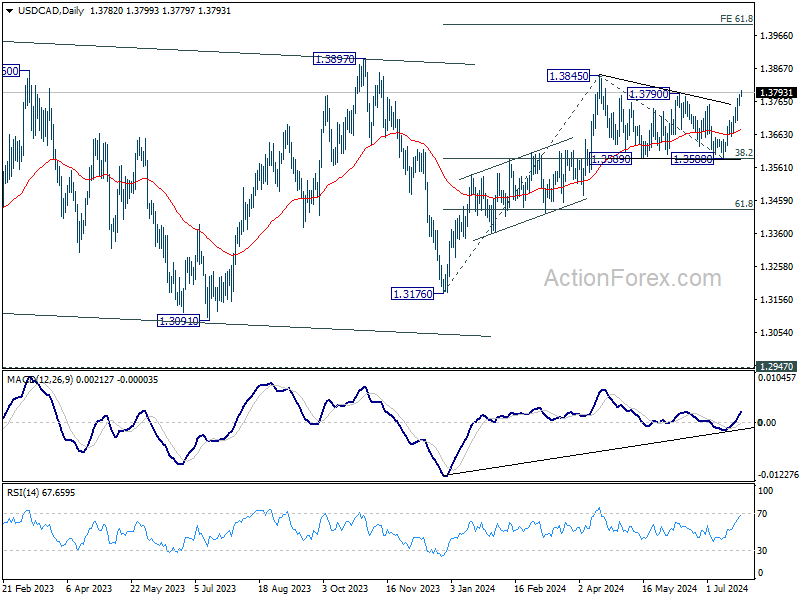

Technically, USD/CAD’s break of 1.3790 resistance solidify the case that consolidation from 1.3845 has completed with three waves down to 1.3588. Retest of 1.3845 high should be seen next. Firm break there will resume whole rally from 1.3176 and target 61.8% projection of 1.3176 to 1.3845 from 1.3588 at 1.4025.

Elsewhere

Germany Gfk consumer sentiment, Eurozone PMIs and UK PMIs will be released in European session. Later in the day, US will release goods trade balance, PMIs, and new home sales.

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.06; (P) 156.08; (R1) 156.60; More…

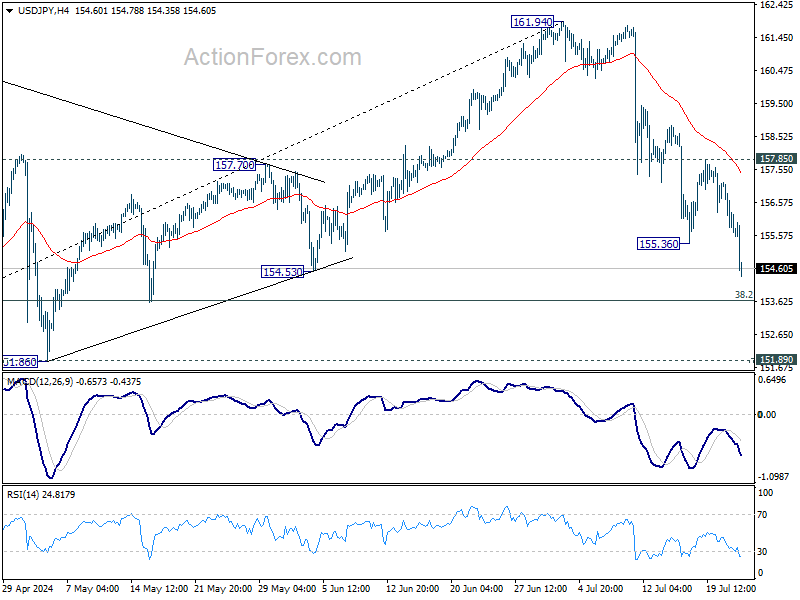

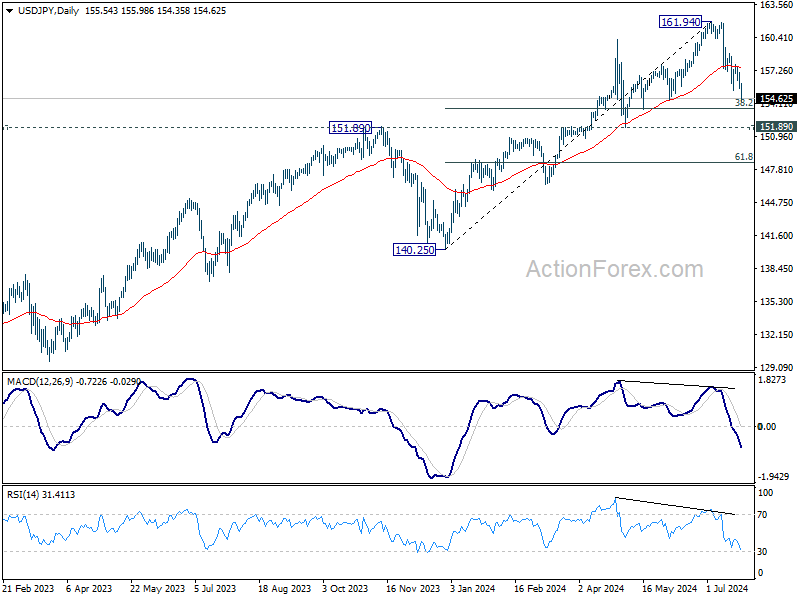

USD/JPY’s fall from 161.94 resumed by breaking through 155.36 today and intraday bias is back on the downside. Further decline should be seen to 38.2% retracement of 140.25 to 161.94 at 153.65. Some support could be seen there to bring rebound, at least on first attempt. Risk will now stay on the downside as long as 157.85 resistance holds, even in case of strong recovery.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Jul P | 47.4 | 47.2 | ||

| 23:00 | AUD | Services PMI Jul P | 50.8 | 51.2 | ||

| 00:30 | JPY | Manufacturing PMI Jul P | 49.2 | 50.5 | 50 | |

| 00:30 | JPY | Services PMI Jul P | 53.9 | 49.4 | ||

| 06:00 | EUR | Germany GfK Consumer Confidence Aug | -21.1 | -21.8 | ||

| 07:15 | EUR | France Manufacturing PMI Jul P | 45.9 | 45.4 | ||

| 07:15 | EUR | France Services PMI Jul P | 49.7 | 49.6 | ||

| 07:30 | EUR | Germany Manufacturing PMI Jul P | 44.5 | 43.5 | ||

| 07:30 | EUR | Germany Services PMI Jul P | 53.5 | 53.1 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jul P | 46.3 | 45.8 | ||

| 08:00 | EUR | Eurozone Services PMI Jul P | 52.9 | 52.8 | ||

| 08:30 | GBP | Manufacturing PMI Jul P | 51.1 | 50.9 | ||

| 08:30 | GBP | Services PMI Jul P | 52.5 | 52.1 | ||

| 12:30 | CAD | New Housing Price Index M/M Jun | 0.10% | 0.20% | ||

| 12:30 | USD | Goods Trade Balance (USD) Jun P | -98.0B | -99.4B | ||

| 12:30 | USD | Wholesale Inventories Jun P | 0.50% | 0.60% | ||

| 13:45 | CAD | BoC Interest Rate Decision | 4.50% | 4.75% | ||

| 13:45 | USD | Manufacturing PMI Jul P | 51.5 | 51.6 | ||

| 13:45 | USD | Services PMI Jul P | 54.5 | 55.3 | ||

| 14:00 | USD | New Home Sales M/M Jun | 643K | 619K | ||

| 14:30 | CAD | BoC Press Conference | ||||

| 14:30 | USD | Crude Oil Inventories | -2.6M | -4.9M |