{kind=link}

Global financial markets lack clear direction today. Major European stock indexes are trading slightly lower, while US futures indicate a modestly higher open. Investors are unfazed by the assassination attempt on former US President Donald Trump, maintaining a calm stance. Focuses are turning to Fed Chair Jerome Powell’s upcoming speech, where the market hopes to gauge his views on the faster-than-expected disinflation trend in the US. Key questions include whether a September rate cut by Fed is now realistic and if a second rate cut this year is back on the radar.

In the currency markets, Dollar is currently the strongest performer, followed by Euro and the Swiss Franc. New Zealand dollar is the weakest, further weighed down by poor New Zealand services data. Sterling is the second weakest, followed by Australian Dollar, while Yen and Canadian dollar are positioned in the middle.

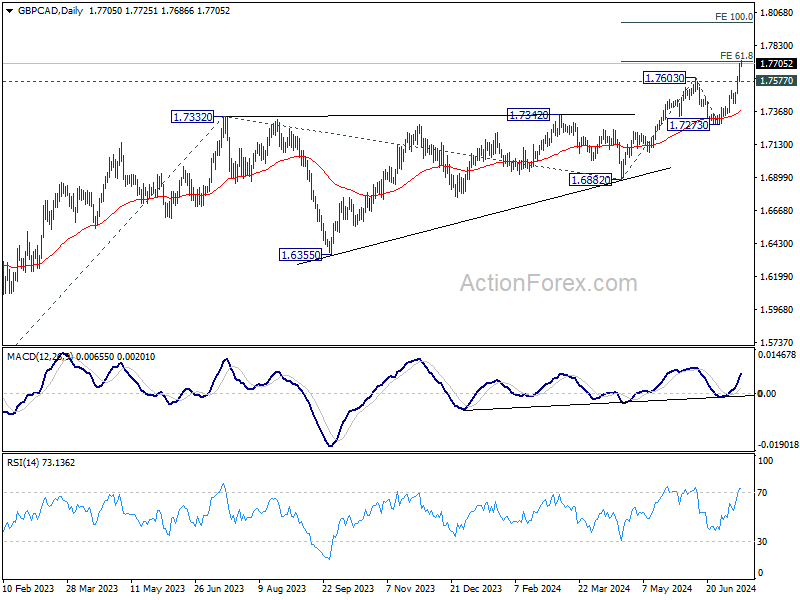

Technically, GBP/CAD’s up trend resumed last week by powering through 1.7603 resistance, but it’s currently struggling at 61.8% projection of 1.6882 to 1.7603 from 1.7273 at 1.7719. Still, further rally is expected as long as 1.7577 support holds. Firm break of 1.7719 would prompt upside acceleration to 100% projection at 1.7994 next. This week’s CPI data from Canada and the UK have the potential to trigger the next move.

In the Europe, at the time of writing, FTSE is down -0.41%. DAX is down -0.46%. CAC is down -0.73%. UK 10-year yield is up 0.017 at 4.129. Germany 10-year yield is up 0.003 at 2.503. Earlier in Asia, Japan was on holiday; Hong Kong HSI fell -1.52%. China Shanghai SSE rose 0.09%. Singapore Strait Times rose 0.06%.

Eurozone industrial productions falls -0.6% mom in May, EU down -0.8% mom

Eurozone industrial production fell -0.6% mom in May, better than expectation of -1.0% mom. Production decreased by -1.0% for intermediate goods, 1.2% for capital goods, and 1.8% for durable consumer goods. Production increased by 0.8% for energy, and 1.6% for non-durable consumer goods.

EU industrial production fell -0.8% mom. The largest monthly decreases were recorded in Slovenia (-7.3%), Romania (-6.2%) and Denmark (-4.9%). The highest increases were observed in Ireland (+6.7%), Luxembourg (+3.9%) and Estonia (+3.8%).

BoE’s Dhingra advocates for rate normalization now

In a podcast today, BoE MPC member Swati Dhingra emphasized that “now is the time” to start normalizing interest rates and to “stop squeezing living standards” as the central bank has been doing to curb inflation.

Dhingra pointed out that demand in the UK is too weak for inflation to surge again, noting that inflation returned to 2% in May. She stated, “I don’t see some kind of consumption boom and if we’re going to start moderating from the very high level of interest rate that we are at now… it is going to take some time for that to happen, for us to moderate it as well as for that to then feed into the real economy.”

Known as a dove within the MPC, Dhingra has consistently voted since February to cut the Bank Rate from its 16-year high of 5.25%.

NZ BNZ services falls to 40.2, weakness accelerating

New Zealand BusinessNZ Performance of Services Index fell from 42.6 to 40.2 in June, marking the lowest level for the sector outside a COVID lockdown month since the survey began in 2007.

BusinessNZ chief executive Kirk Hope noted that after a poor May result, June’s figures “simply got worse”. Activity/Sales dropped to 35.6 and New Orders/Business fell to 38.3, both hitting record lows for non-lockdown months. Employment decreased to 45.6, the lowest since February 2022, while Supplier Deliveries declined to 41.6, the lowest since March 2022.

Negative comments rose to 67.0% in June, up from 65.4% in May and 66.3% in April, with respondents citing recessionary pressures.

BNZ Senior Economist Doug Steel observed, “The Performance of Services Index has been well below average for more than a year. Moreover, the weakness appears to be accelerating.”

China’s Q2 GDP growth slows to 4.7% amid weak domestic demand

China’s GDP grew 4.7% yoy in Q2, down from 5.3% in Q1 and missing expectations of 5.1%. For the first half of the year, GDP growth stood at 5% year-on-year.

The National Bureau of Statistics noted, “The current external environment is complicated, while domestic demand remains insufficient. We still need to consolidate the foundation for economic recovery.”

June’s industrial production increased by 5.3% yoy, exceeding expectations of 5.0% yoy. However, retail sales grew only 2.0% yoy, well below the forecasted 3.3% yoy.

Fixed asset investment in the first six months rose by 3.9% ytd yoy, meeting expectations. Property investment saw a -10.1% yoy decline, consistent with May’s fall. Additionally, home sales by floor area dropped by -19.0% yoy.

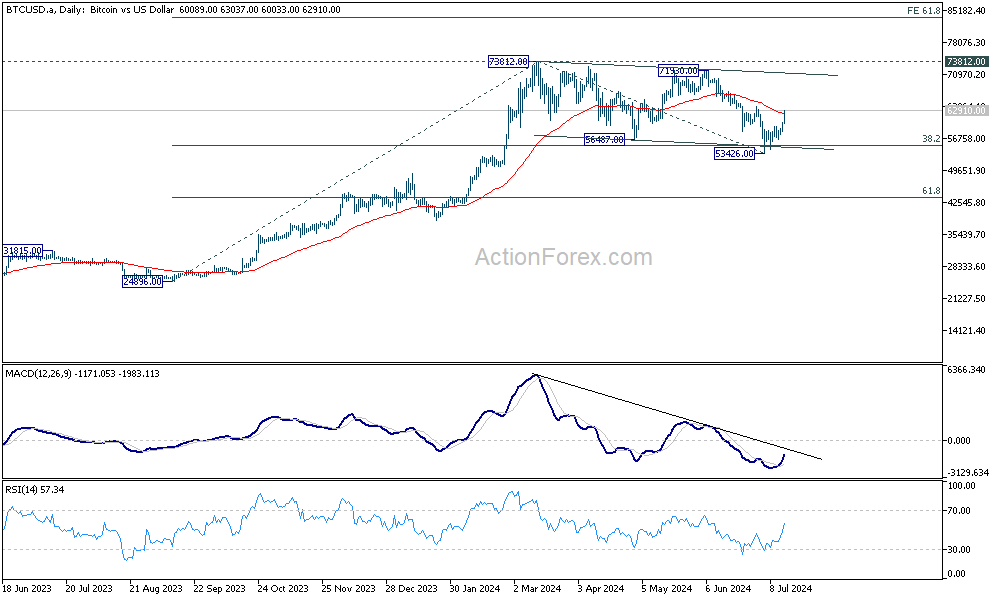

Bitcoin ready for new record high, Ethereum following

Bitcoin jumps sharply higher today as rebound from 53426 extended. The break of 55 D EMA (now at 62400) is taken as a sign that corrective pattern from 73812 has completed with three waves down to 53426. That came after hitting 38.2% retracement of 24896 to 73812 at 55126.

Sustained trading above 55 D EMA will strengthen this bullish case. Bitcoin should then target 73812 record high, and then 61.8% projection of 24896 to 73812 from 53426 at 83656.

Similarly, Ethereum’s corrective pattern from 4092.55 could have finished with three waves to 2797.60, after hitting 50% retracement of 1519.15 to 4092.55 at 2805.85. Sustained trading above 55 D EMA (now at 3333.45) would solidify this bullish case. Ethereum should then target 4092.55 high and then 61.8% projection of 1519.15 to 4092.55 from 2797.60 at 4387.96.

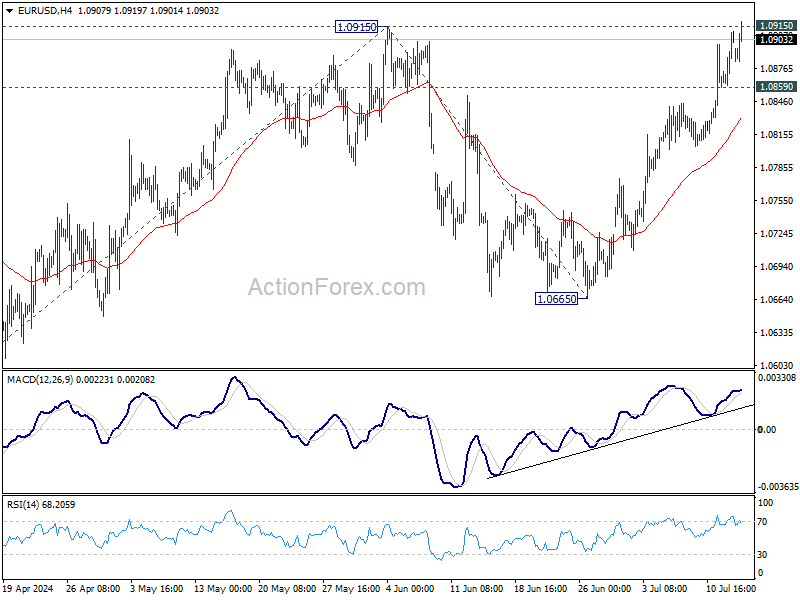

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0876; (P) 1.0893; (R1) 1.0925; More….

No change in EUR/USD’s outlook and intraday bias remains on the upside for the moment. Decisive break of 1.0915 resistance will resume whole rise from 1.0601 to 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. On the downside, below 1.0859 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that’s still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Jun | 40.2 | 43 | 42.6 | |

| 23:01 | GBP | Rightmove House Price Index M/M Jul | -0.40% | 0.00% | ||

| 02:00 | CNY | GDP Y/Y Q2 | 4.70% | 5.10% | 5.30% | |

| 02:00 | CNY | Industrial Production Y/Y Jun | 5.30% | 5.00% | 5.60% | |

| 02:00 | CNY | Retail Sales Y/Y Jun | 2.00% | 3.30% | 3.70% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jun | 3.90% | 3.90% | 4.00% | |

| 06:30 | CHF | PPI M/M Jun | 0.00% | 0.10% | -0.30% | |

| 06:30 | CHF | PPI Y/Y Jun | -1.90% | -1.80% | ||

| 09:00 | EUR | Eurozone Industrial Production M/M May | -0.60% | -1.00% | -0.10% | |

| 12:30 | USD | Empire State Manufacturing Index Jul | -6.6 | -5.5 | -6.0 | |

| 12:30 | CAD | Manufacturing Sales M/M May | 0.40% | 0.20% | 1.10% | |

| 12:30 | CAD | Wholesale Sales M/M May | -0.80% | 2.00% | 2.40% | |

| 14:30 | CAD | BoC Business Outlook Survey |