{kind=link}

New Zealand Dollar plunged sharply after RBNZ’s more dovish than expected statement caught the market off guard. RBNZ’s indication of potential future rate cuts was unexpected, even though it’s not a hint on an imminent move.

The central bank’s timing of this shift in tone is puzzling, as Q2 CPI data will only be available next week and updated economic forecasts are expected in August. There is no apparent urgency for RBNZ to tweak the statement at this meeting.

Traders quickly adjusted their expectations, now betting on rate cuts later this year. While August might be too soon, November now appears to be a more probable timeframe for the first reduction.

In the broader currency markets, Yen is also suffering, continuing its recent selloff. Dollar is the third worst performer today at this point. Markets showed little reaction to Fed Chair Jerome Powell’s first day of semiannual testimony overnight, instead turning their focus to the upcoming US CPI release tomorrow. Swiss Franc leads the gains for the day, followed by Euro and Sterling, with Australian Dollar and Canadian Dollar trading in the middle.

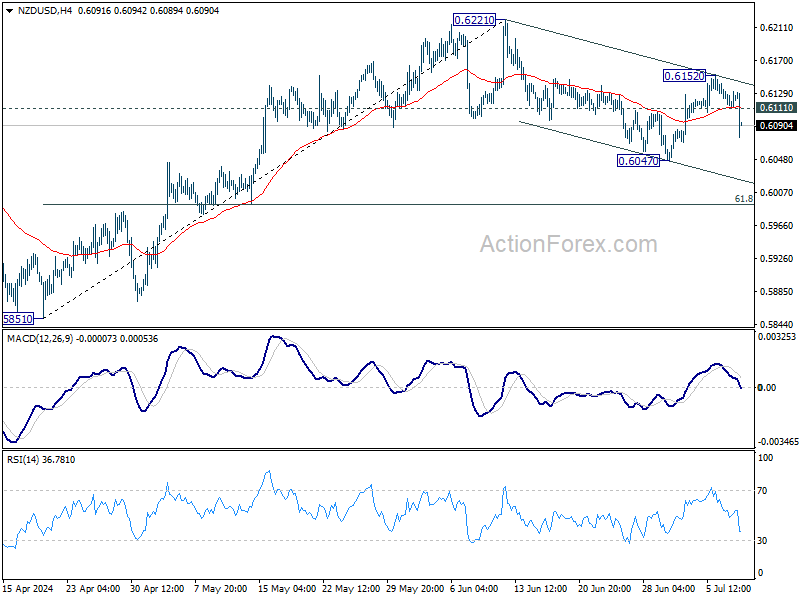

Technically, NZD/USD’s steep fall suggests that recovery from 0.6047 has completed at 0.6152 already. Corrective decline from 0.6221 might be ready to resume. Deeper fall is expected as long as 0.6111 minor resistance holds. Break of 0.6047 will target 61.8% retracement of 0.5851 to 0.6221 at 0.5992.

In Asia, at the time of writing, Nikkei is up 0.43%. Hong Kong HSI is down -0.07%. China Shanghai SSE is down -0.50%. Singapore Strait Times is up 0.62%. Japan 10-year JGB yield is up 0.012 at 1.088. Overnight, DOW fell -0.13%. S&P 500 rose 0.07%. NASDAQ rose 0.14%. 10-year yield rose 0.031 to 4.300.

RBNZ holds rates at 5.50%, softens hawkish tone

RBNZ left OCR unchanged at 5.50%, as widely expected. The central bank softened its hawkish stance in the accompanying statement, indicating that the extent of monetary restriction “will be tempered over time consistent with the expected decline in inflation pressures.” Markets interpreted this as a signal that RBNZ is moving closer to lowering interest rates.

RBNZ also acknowledged that its restrictive monetary policy has “significantly reduced consumer price inflation,” with headline inflation expected to return to the 1-3% target band “in the second half of this year.” This decline in inflation reflects both receding domestic pricing pressures and lower inflation for imported goods and services. Additionally, labor market pressures have eased.

While domestically generated price pressures “remain strong,” RBNZ said there are signs that “inflation persistence will ease in line with the fall in capacity pressures and business pricing intentions.”

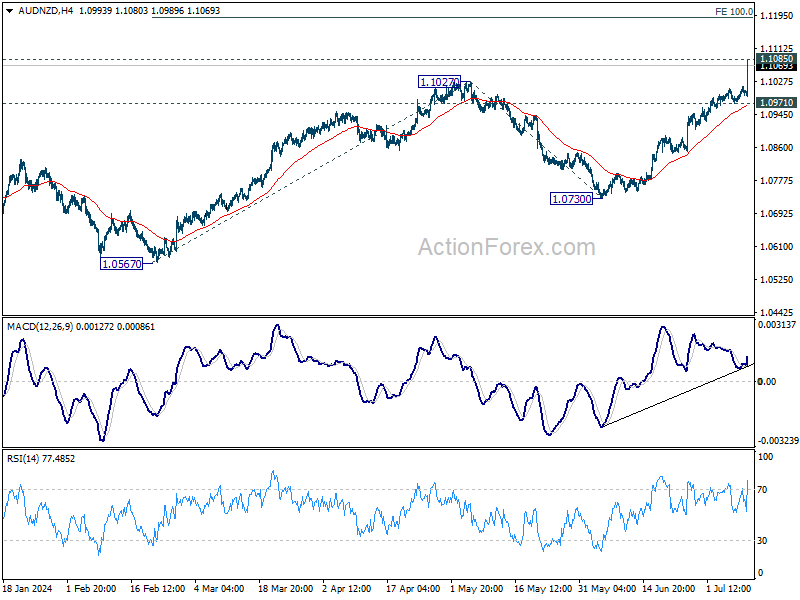

AUD/NZD soars after RBNZ, more upside if policy diverges with RBA

AUD/NZD soars sharply higher after RBNZ softened its hawkish stance, incorporating language in its latest statement that suggests a shift towards monetary easing. This change has created prospects for stronger rally in the cross, driven by policy divergence between RBNZ and RBA.

In particular, if RBNZ moves to cut interest rates sooner than previously projected, while RBA raises rates in response to strong Q2 Australian inflation data, AUD/NZD could see even more significant gains in the medium term.

Technically, immediate focus is now on 1.1085 key medium term resistance (2023 high). Firm break there will confirm whole rebound from 1.0469 (2022 low). Next target will be 100% projection of 1.0567 to 1.1027 from 1.0730 at 1.1190.

Strong break of 1.1190 would bring upside acceleration to 161.8% projection at 1.1474 in the medium term. In any case, near term outlook will stay bullish as long as 1.0971 support holds for now.

China’s CPI slows to 0.2% in Jun, PPI negative for 21st month

China’s CPI slowed to 0.2% yoy in June, down from 0.3% yoy in May, missing expectations of a 0.4% yoy increase. Core CPI, which excludes volatile food and energy prices, rose by 0.6% yoy, unchanged from May, but slightly slower than the 0.7% increase observed in the first half of the year.

On a month-on-month basis, inflation remained negative in June, with CPI falling by -0.2%, following a -0.1% decrease in May. This continued negative trend reflects ongoing deflationary pressures in the economy.

PPI fell by -0.8% yoy, improving from the prior month’s -1.4% yoy decline and matching market expectations. Despite the slight improvement, PPI has remained negative for the 21st consecutive month, indicating persistent weakness in industrial prices.

Looking ahead

Italy industrial production will be released in European session. US will release wholesale inventories final, and crude oil inventories. That’s it for economic data. Nevertheless, some focuses could be put on BoE Chief Economist Huw Pill’s speech as well as Fed Chair Jerome Powell’s testimony day 2.

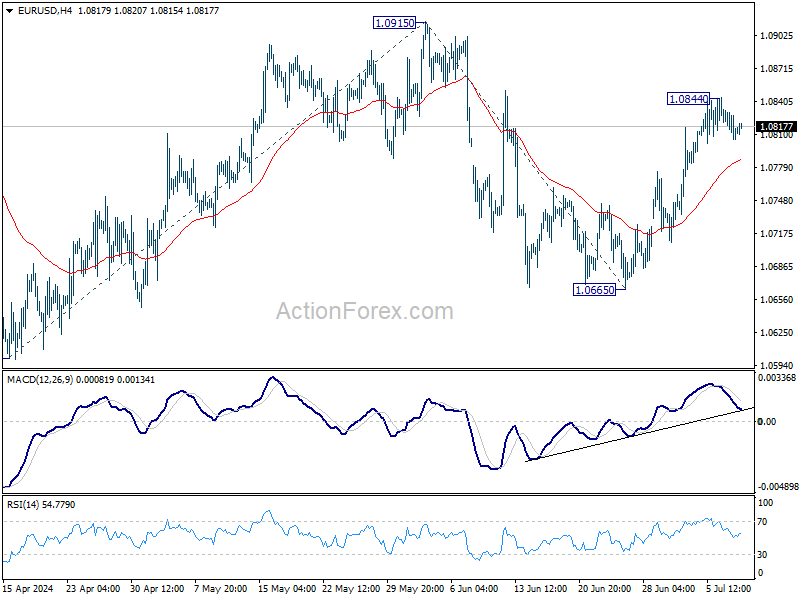

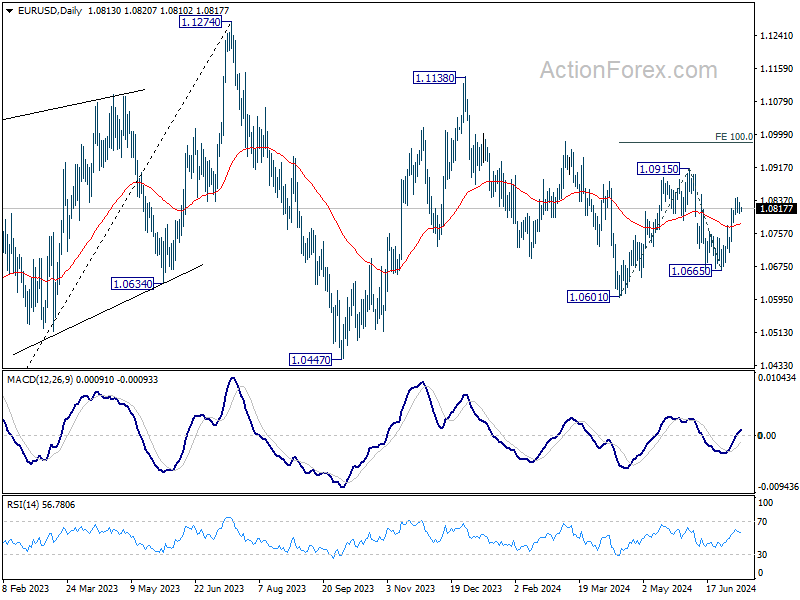

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0802; (P) 1.0824; (R1) 1.0845; More….

EUR/USD is extending consolidation below 1.0844 temporary top, and intraday bias remains neutral for the moment. Further rally is in favor as long as 55 4H EMA (now at 1.0786) holds. On the upside, above 1.0844 will resume the rebound from 1.0665 to retest 1.0915 resistance. Firm break there will target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0919 next. However, sustained break of 55 4H EMA will bring deeper fall back to 1.0665 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that’s still in progress. Break of 1.0601 will target 1.0447 support and possibly below. On the upside, firm break of 1.0915 resistance will start another rising leg back to 1.1138 resistance instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Jun | 2.90% | 2.90% | 2.40% | 2.60% |

| 01:30 | CNY | CPI Y/Y Jun | 0.20% | 0.40% | 0.30% | |

| 01:30 | CNY | PPI Y/Y Jun | -0.80% | -0.80% | -1.40% | |

| 02:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% | 5.50% | |

| 08:00 | EUR | Italy Industrial Output M/M May | 0.20% | -1.00% | ||

| 14:00 | USD | Wholesale Inventories May F | 0.60% | 0.60% | ||

| 14:30 | USD | Crude Oil Inventories | 0.7M | -12.2M | ||

| 18:00 | USD | Fed’s Beige Book |