{kind=link}

Swiss Franc is currently the worst performer today, plummeting after SNB delivered a rate cut for the second consecutive meeting. In addition to the rate reduction, SNB lowered its inflation forecast across the board. Nevertheless, Franc’s selloff has been relatively restrained.

Notably, SNB did not mention the recent sharp appreciation of the Franc in its press release, suggesting that it wasn’t a primary driver for the rate cut. Additionally, SNB Chair Thomas Jordan emphasized that currency market interventions could be executed in both directions. This suggests that SNB might tolerate further appreciation of the Franc for now, especially if driven by political instability in the EU.

Sterling also saw broad weakening, becoming the second worst performer after BoE decided to keep interest rates unchanged, as widely expected. While the decision itself was anticipated, the accompanying statement pointed to the August economic forecasts for a more comprehensive assessment of inflation.

Within the Monetary Policy Committee, some members expressed concern over the persistent high services inflation and its implications for overall inflation persistence. However, other members believed that this did not significantly alter the economy’s current disinflationary path. All in all, the statement suggested that a rate cut in August is still on the table.

In the broader currency markets, Australian Dollar, New Zealand Dollar, Dollar have been rotating as the strongest currencies, primarily benefiting from the selloff in European majors. Euro is currently the third weakest currency, as dragged down by the selloff in Swiss Franc and Sterling. Meanwhile, Japanese Yen, despite breaking lower against Dollar, is trading in the middle along with Canadian Dollar.

Technically, a temporary low was formed at 0.8825 in USD/CHF with today’s recovery. Some consolidations would be seen first, but outlook will stay bearish as long as 0.8992 resistance holds. Break of 0.8825 is extended later to resume whole decline from 0.9223. However, considering bullish convergence condition in 4H MACD, firm break of 0.8992 will argue that the fall from 0.9223 has completed as a corrective move. Further rally would then be seen back to retest 0.9223 high.

In Europe, at the time of writing, FTSE is up 0.31%. DAX is up 0.41%. CAC is up 0.78%. UK 10-year yield is down -0.0017 at 4.067. Germany 10-year yield is up 0.034 at 2.442. Earlier in Asia, Nikkei rose 0.16%. Hong Kong HSI fell -0.52%. China Shanghai SSE fell -0.42%. Singapore Strait Times fell -0.12%. Japan 10-year JGB yield rose 0.0199 to 0.956.

US initial jobless claims falls to 238k vs exp 240k

US initial jobless claims fell -5k to 238k in the week ending June 15, slightly lower than expectation of 240k. Four-week moving average of initial claims rose 5.5k to 233k.

Continuing claims rose 15k to 1828k in the week ending June 8. Four-week moving average of continuing claims rose 10k to 1806k.

BoE maintains rate, eyes August forecasts for inflation assessment

BoE left Bank Rate unchanged at 5.25%, as widely anticipated, with a 7-2 vote among the Monetary Policy Committee members. Swati Dhingra and Dave Ramsden again voted for a 25 bos cut to 5.00%.

The central bank stated that, as part of the August forecast round, the Committee will review all available information to assess whether the risks from persistent inflation are receding. Based on this assessment, the Committee will determine how long the Bank Rate should be maintained at its current level.

While CPI fell to 2% in May, BoE expects it to “rise slightly” in the second half of the year due to the base effects from last year’s energy price declines. Additionally, BoE noted that services inflation at 5.7% was “somewhat higher” than projected in the May monetary policy report.

On the growth front, GDP appears to have “grown more strongly than expected” during the first half of the year but remains consistent with a growth rate of around 0.25% per quarter.

SNB cuts 25bps, lowers inflation forecasts slightly

SNB lowered the policy rate by 25bps to 1.25% and maintained the willingness to be active in the foreign exchange markets as necessary.

In the accompanying statement, SNB said “underlying inflationary pressure has decreased again”. The central will continue to monitor the development of inflation closely, and will “adjust its monetary policy if necessary.

Taking into account today’s policy rate cut, the new conditional inflation forecast were lowered slightly to 1.3% in 2024 (prior 1.4%), 1.1% in 2025 (prior 1.2%), and then 1.0% in 2026 (prior 1.1%).

Growth is likely to remain “moderate” in Switzerland in the coming quarters. SNB anticipates GDP growth of around 1% this year, and 1.5% in 2025.

Ifo upgrades German GDP forecasts, slowly working its way out of crisis

The Ifo Institute upgraded its growth forecasts for German economy, indicating that it is “slowly working its way out of the crisis.” GDP is now expected to grow by 0.4% in 2024, up from March forecast of 0.2%. Growth is projected to further accelerate to 1.5% in 2025, maintaining the previous forecast. Inflation is expected to decrease significantly, from 5.9% in 2023 to 2.2% in 2024, and further down to 1.7% in 2025.

The institute anticipates that the overall economic recovery will gain momentum throughout the rest of the year as consumer spending normalizes. Purchasing power of private households is expected to strengthen, leading to a gradual recovery in the demand for goods and services.

Moreover, the Ifo Institute expects ECB’s interest rate cut in June is likely to be followed by two more cuts this year. These lower interest rates, coupled with a stable labor market and robust income growth, are expected to boost the consumer economy and aid in the gradual recovery of the construction sector.

New Zealand GDP grows 0.2% qoq, pulls out of recession despite per capita decline

New Zealand’s GDP grew by 0.2% qoq in Q1, surpassing the expected 0.1% growth and pulling the economy out of a technical recession following consecutive declines in the last half of 2023. On an annual basis, GDP growth was also 0.2% yoy. The primary industries experienced a modest growth of 0.2% qoq, while goods-producing industries contracted by -1.3% qoq, and services industries saw a slight decline of -0.1% qoq.

Despite the overall GDP growth, GDP per capita fell by -0.3% qoq, marking the sixth consecutive quarterly decline, with an annual decrease of -2.4% yoy. This indicates that while the economy as a whole is recovering, the average economic output per person continues to decline.

“There were a range of results at industry level, with 8 of the 16 industries rising this quarter,” noted Ruvani Ratnayake, senior manager of national accounts industry and production. This mixed performance across different sectors highlights the uneven nature of the economic recovery.

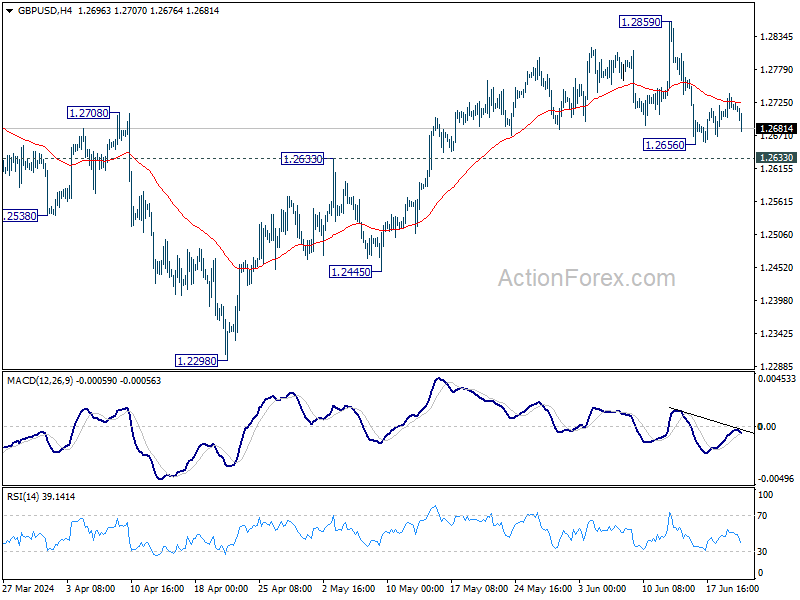

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2695; (P) 1.2717; (R1) 1.2742; More…

GBP/USD weakens after rejection by 55 4H EMA but stays above 1.2656 temporary low. Intraday bias remains neutral first. While another recovery cannot be ruled out, risk will stay on the downside as long as 1.2859 resistance holds. Firm break of 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

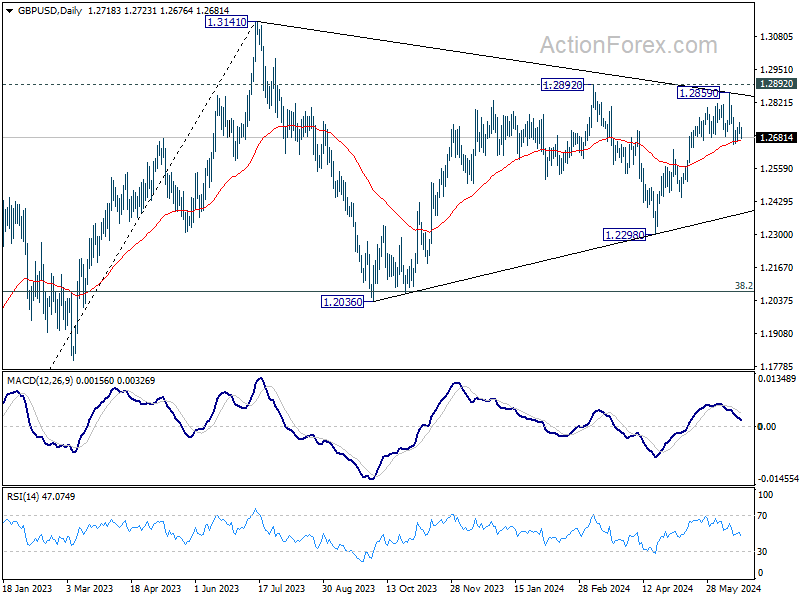

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q1 | 0.20% | 0.10% | -0.10% | |

| 01:15 | CNY | 1-y Loan Prime Rate | 3.45% | 3.45% | 3.45% | |

| 01:15 | CNY | 5-y Loan Prime Rate | 3.95% | 3.95% | 3.95% | |

| 06:00 | CHF | Trade Balance (CHF) May | 5.81B | 3.84B | 4.32B | 4.34B |

| 06:00 | EUR | Germany PPI M/M May | 0.00% | 0.10% | 0.20% | |

| 06:00 | EUR | Germany PPI Y/Y May | -2.20% | -2.00% | -3.30% | |

| 07:30 | CHF | SNB Interest Rate Decision | 1.25% | 1.50% | 1.50% | |

| 08:00 | CHF | SNB Press Conference | ||||

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 11:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% | 5.25% | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 0–2–7 | 0–2–7 | 0–2–7 | |

| 12:30 | CAD | New Housing Price Index M/M May | 0.20% | 0.20% | 0.20% | |

| 12:30 | USD | Building Permits May | 1.39M | 1.46M | 1.44M | |

| 12:30 | USD | Housing Starts May | 1.28M | 1.38M | 1.36M | |

| 12:30 | USD | Current Account (USD) Q1 | -238B | -206B | -195B | |

| 12:30 | USD | Initial Jobless Claims (Jun 14) | 238K | 240K | 242K | 243K |

| 12:30 | USD | Philadelphia Fed Survey Jun | 1.3 | 4.5 | 4.5 | |

| 14:00 | EUR | Eurozone Consumer Confidence Jun P | -14 | -14 | ||

| 15:00 | USD | Crude Oil Inventories | -2.8M | 3.7M |