{kind=link}

The Japanese Yen has taken a significant hit today, losing ground against all major currencies after BoJ refrained from detailing an immediate plan to taper its bond purchases. In the lead-up to the announcement, expectations were high among traders and investors that BoJ would begin tapering soon, fueled by multiple media reports. However, the central bank only indicated an intention to taper, deferring detailed discussions until its July meeting.

BoJ’s cautious stance underscores its strategy to wait for the new economic outlook and projections due in July before making any firm decisions. And that’s understandable. However, this delay has left the market in a state of uncertainty and unease, prompting speculation on whether there will eventually be a definitive cut in purchase amounts…

Simultaneously, Dollar is continuing to rebound and reverse the losses incurred after the recent CPI data release. Canadian Dollar is emerging as the day’s second strongest performer at this point, followed by Euro and Swiss Franc. In contrast, New Zealand and Australian Dollars are underperforming, marginally better than Yen, with British Pound also showing some weakness.

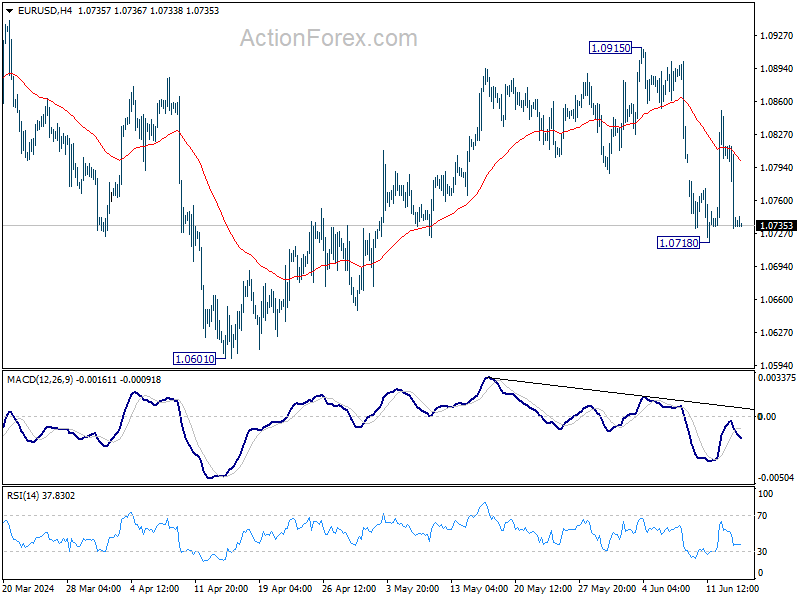

Technically, Euro is a focus today as the near term decline in both EUR/GBP and EUR/CHF resumed after brief recovery. Now, break of 1.0718 support in EUR/USD will also indicate resumption of fall from 1.0915. That would strengthen the case that whole rise from 1.0601 has completed at 1.0915, and bring retest of this low.

In Asia, at the time of writing, Nikkei is up 0.39%. Hong Kong HSI is down -0.47%. China Shanghai SSE is up 0.06%. Singapore Strait Times is down -0.49%. Japan 10-year JGB yield is down -0.034 at 0.937. Overnight, DOW fell -0.17%. S&P 500 rose 0.23%. NASDAQ rose 0.34%. 10-year yield fell -0.057 to 4.238.

BoJ holds interest rates, prepares for bond purchase reduction plan in next month

BoJ left uncollateralized overnight call rate unchanged at 0-0.10% as widely expected. In addition, BoJ will continue its asset purchase program until the end of June. The central bank, by an 8-1 majority vote, has also decided to reduce its JBG purchase amounts afterward.

The detailed plan for the reduction in JGB purchases, which will cover the next one to two years, is set to be determined by at next meeting. Apparently, BoJ would likely to have access to the new economic and price output report before laying out the plan.

BoJ is optimistic about Japan’s economic prospects, projecting that the economy will grow at a rate above its potential growth rate. Core CPI is expected to increase through fiscal 2025 due to factors such as the waning effects of government economic measures. Furthermore, underlying inflation is predicted to gradually rise as the output gap improves and medium-to long-term inflation expectations climb.

NZ BNZ manufacturing falls to 47.2 in 15th month of contraction

New Zealand’s BusinessNZ Performance of Manufacturing Index dropped from 48.8 to 47.2 in May, marking the sector’s 15th consecutive month of contraction.

Looking as some details, production plummeted from 50.3 to 44.5, indicating a sharp return to contraction. Employment showed a slight decline from 50.9 to 50.6. New orders fell further from 45.4 to 44.4, maintaining their contraction for the 21st straight month. Finished stocks rose from 50.7 to 52.4, but deliveries fell from 48.1 to 45.2.

Despite the decline in the overall index, the proportion of negative comments decreased to 63.5% from 69% in April and 65% in March. Most negative feedback highlighted the general economic slowdown and the current recessionary pressures.

Looking ahead

Eurozone trade balance will be released in Euroepan session. Later in the data, Canada manufacturing sales and wholesale sales, and US import prices and U of Michigan consumer sentiment will be published.

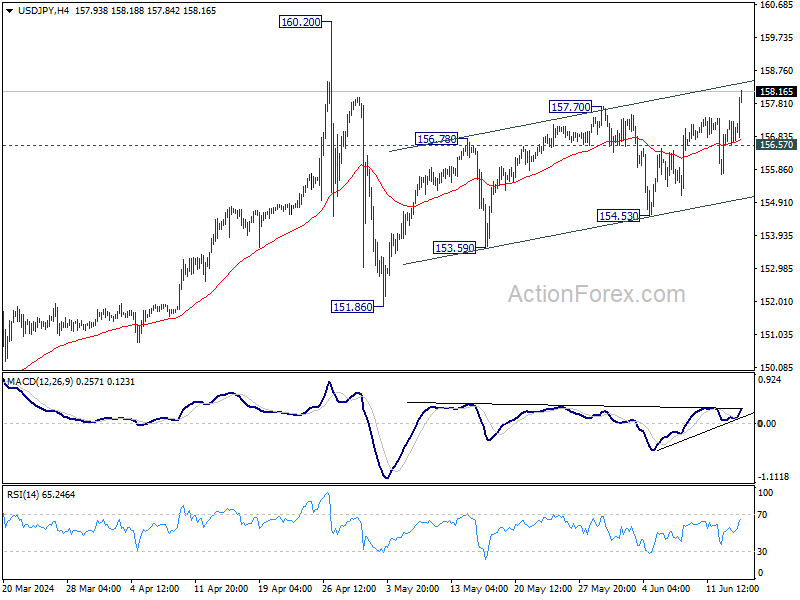

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.62; (P) 156.97; (R1) 157.35; More…

USD/JPY’s choppy rise from 151.86 resumed by breaking through 157.70 resistance and intraday bias back on the upside. Further rise should be seen to retest 160.20 high but strong resistance could be seen there to limit upside. On the downside, below 156.57 minor support will turn intraday bias neutral first.

In the bigger picture, a medium term top should be formed at 160.20. As long as 55 W EMA (now at 147.77) holds, fall from 160.20 is seen as correcting the rise from 140.25 only. However, sustained break of 55 W EMA will argue that larger correction is possibly underway, and target 146.47 support next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI May | 47.2 | 48.9 | 48.8 | |

| 03:23 | JPY | BoJ Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 04:30 | JPY | Tertiary Industry Index M/M Apr | 1.90% | 0.40% | -2.40% | -2.30% |

| 04:30 | JPY | Industrial Production M/M Apr F | -0.90% | -0.10% | -0.10% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Apr | 17.0B | 17.3B | ||

| 12:30 | CAD | Manufacturing Sales M/M Apr | 1.30% | -2.10% | ||

| 12:30 | CAD | Wholesale Sales M/M Apr | 2.50% | -1.10% | ||

| 12:30 | USD | Import Price Index M/M May | 0.10% | 0.90% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jun P | 73 | 69.1 |