{kind=link}

Dollar weakened broadly overnight, particularly against European majors, following disappointing US manufacturing data that also pressured benchmark Treasury yields lower. This data not only pushed benchmark Treasury yields lower but also triggered the greenback’s downturn. Despite these movements, the stock markets closed mixed, suggesting that the market reactions were not entirely aligned with the negative data impact. Investors now turn their attention to upcoming economic indicators, such as ISM services data non-farm payroll, hoping these will provide the Dollar with some support.

In the broader currency market, Canadian Dollar is currently the weakest performer for the week at this point, followed by Dollar. Australian Dollar is also underperforming, suggesting that the market mood is not decisively risk-on. Conversely, New Zealand Dollar has been the strongest so far, followed by Swiss Franc and Japanese Yen, with Euro and British Pound holding middle ground.

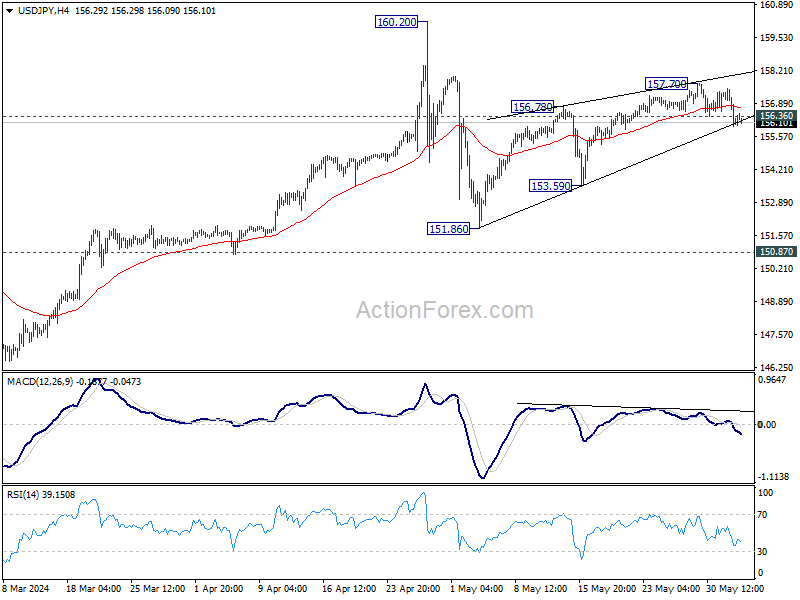

Technically, USD/JPY’s break of 156.36 minor support is taken as the first sign that rebound from 151.86 has completed with three waves up to 157.70. Deeper fall will is in favor back to 153.59 support first. Firm break there will likely resume the whole pattern from 160.20 through 151.86 support.

If realized, however, this movement raises a critical question: Will this potential fall in USD/JPY be part of a wider Dollar selloff or could it herald a more extensive rebound in Yen across other currency pairs?

In Asia, at the time of writing, Nikkei is down -0.22%. Hong Kong HSI is up 0.27%. China Shanghai SSE is down -0.14%. Singapore Strait Times is down -0.15%. Japan 10-year JGB yield is down -0.0196 at 1.049. Overnight, DOW fell -0.30%. S&P 500 rose 0.11%. NASDAQ rose 0.56%. 10-year yield fell -0.112 to 4.402.

BoJ’s Ueda: Monetary policy adjustments possible if inflation rises

BoJ Governor Kazuo Ueda addressed the parliament today, indicating that the central bank is prepared to adjust its level of monetary support if underlying inflation accelerates as forecasted. Ueda added, “If our economic and price outlook, or risks, change, that will also be reason to change the level of interest rates.”

Discussing long-term interest rates, Ueda mentioned that the central bank’s fundamental approach is to allow market forces to determine these rates. However, he also emphasized that BoJ would conduct “nimble” market operations if long-term interest rates were to spike, highlighting the bank’s readiness to increase bond buying when necessary.

Japan’s Suzuki confirms impact of market intervention to support yen

Japan’s Finance Minister Shunichi Suzuki confirmed today that recent interventions in the currency market had a notable impact on stabilizing Yen. During a press conference following a regular cabinet meeting, Suzuki explained that the interventions at the end of April and early May were specifically targeted to counteract excessive currency market movements.

According to data released by the Ministry of Finance last Friday, Japan spent JPY 9.79T over the past month to bolster Yen. This data confirmed traders’ and analysts’ suspicions that Tokyo conducted significant dollar-selling interventions.

These interventions occurred shortly after Yen plummeted to a 34-year low of 160.245 per dollar on April 29 and again in the early hours of May 2 in Tokyo.

US 10-year yield plunges as Fed cut expectations heighten slightly

US 10-year Treasury yield dropped significantly overnight, marking its most substantial one-day decline since last December. This sharp fall was triggered by disappointing economic data, revealing contraction in manufacturing activity for the second consecutive month. This indication of a cooling economy lifted optimism among investors slightly, as Fed would still be on track for monetary policy easing this year.

Currently, the probability of an initial rate cut in September has climbed to nearly 60%, according to Fed fund futures. Furthermore, expectations for a total of two rate cuts by year-end have also increased, now standing at 52.8%. However, these speculations could see dramatic shifts depending on the outcomes of upcoming economic reports, including ISM services data and non-farm payroll figures later this week.

Technically, as long as 4.318 support holds, 10-year yield’s rebound from 3.780 is still in favor to extend through 4.730 at a later stage. However, as this rise is seen as the second leg of the corrective pattern from 4.997, strong resistance should be seen below there to limit upside. Sustained break of 4.318 will indicate near term reversal, and turn outlook bearish.

Looking ahead

Swiss CPI and Germany unemployment rate featured in European session. Later in the day, US will release factory orders.

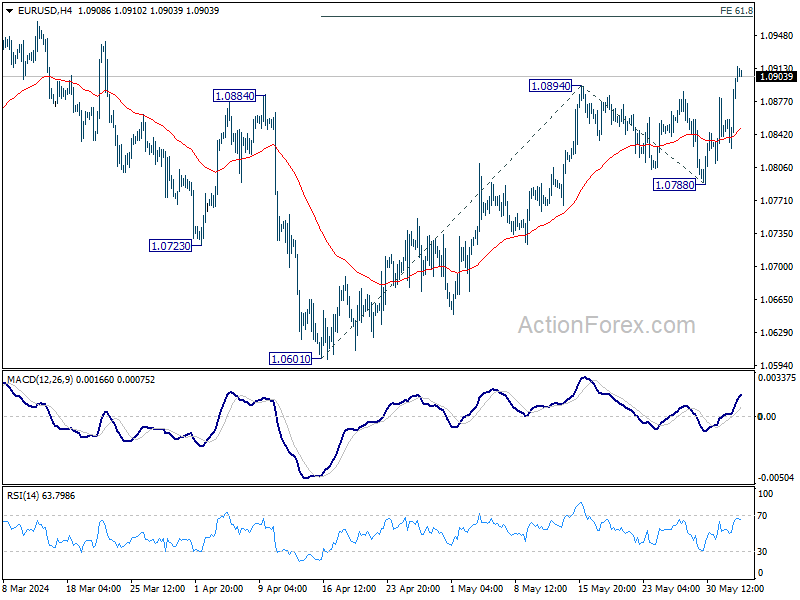

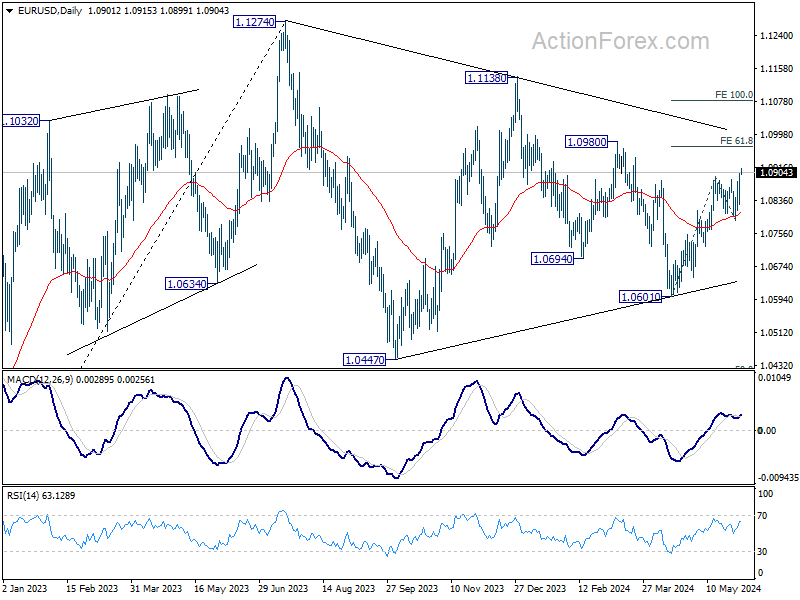

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0854; (P) 1.0879; (R1) 1.0931; More….

EUR/USD’s rally from 1.0601 resumed by break through 1.0894 resistance. Intraday bias is back on the upside for t .8% projection of 1.0601 to 1.0894 from 1.0788 at 1.0969. For now, risk will stay on the upside as long as 1.0788 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0788 support will extend the corrective pattern instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y May | 0.90% | 2.20% | 2.10% | |

| 01:30 | AUD | Current Account Balance (AUD) Q1 | -4.9B | 5.9B | 11.8B | 2.7B |

| 06:30 | CHF | CPI M/M May | 0.40% | 0.30% | ||

| 06:30 | CHF | CPI Y/Y May | 1.40% | |||

| 07:55 | EUR | Germany Unemployment Change May | 7K | 10K | ||

| 07:55 | EUR | Germany Unemployment Rate May | 5.90% | 5.90% | ||

| 14:00 | USD | Factory Orders M/M Apr | 0.70% | 1.60% |