{kind=link}

As US session commences, Dollar is showing a more notable downturn following a rather uneventful day. In the background risk sentiment is steady, with investors and traders largely holding their positions in anticipation of key economic data releases. The upcoming PCE inflation data on Thursday and ISM manufacturing data on Friday are particularly crucial. These datasets are expected to play a significant role in shaping the current narrative of falling inflation and a stabilizing economy, which is hoped to lead to soft landing.

However, it’s also important to note that both Canadian Dollar and Euro are having some struggles too in their respective crosses. Euro, in particular, is looking vulnerable against Sterling and Australian Dollar. Important economic data releases are on the horizon for these currencies as well, including Canadian employment figures and Eurozone PMI flash data later in the week.

Australian Dollar and Japanese Yen are showing strength today. For Aussie, there is some focus on retail sales data due tomorrow, but Wednesday’s monthly CPI is likely to be a more significant driver. As for Yen, significant developments to watch include China’s PMI data and the Yuan’s impact, given the recent parallel trends between the two.

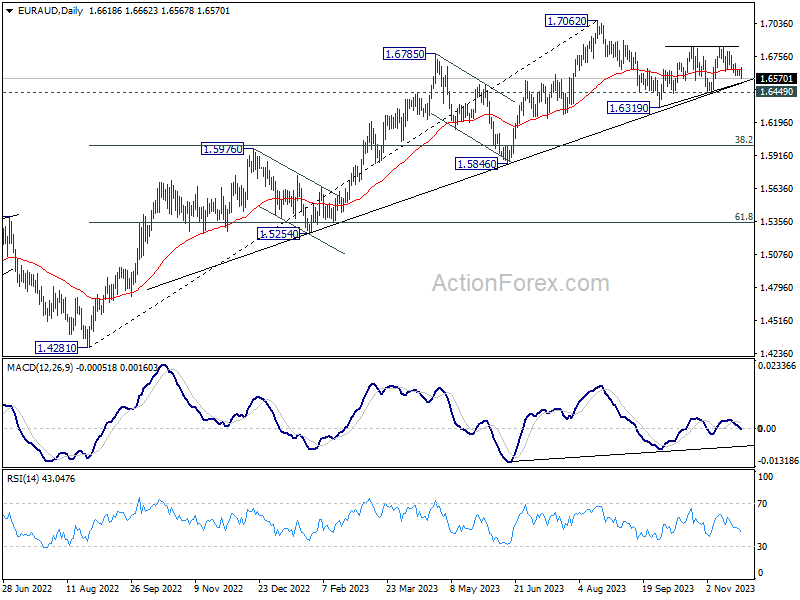

From a technical perspective, the next few days could be critical for EUR/AUD, as it’s now heading back to medium term trendline support. Sustained break there, followed by firm break of 1.6449 support will argue that fall from 1.7062 is already corrective whole up trend from 1.4281 (2022 low). In this case, near term outlook will be turned bearish with prospect of falling to 1.5846 support before a sustainable bounce.

In European session, at the time of writing, FTSE is down -0.26%. DAX is down -0.14%. CAC is down -0.03%. Germany 10-year yield is down -0.058 at 2.588. Earlier in Asia, Nikkei fell -0.53%. Hong Kong HSI fell -0.20%. China Shanghai SSE fell -0.30%. Singapore Strait Times fell -0.27%. Japan 10-year JGB yield fell -0.0026 to 0.776.

BoE’s Bailey: Too soon to have discussion on rate cuts

In an interview with ChronicleLive, BoE Governor Andrew Bailey pointed out that the recent decline in inflation is largely attributed to the unwinding of last year’s surge in energy prices.

He highlighted two important phases in the inflation reduction process. He anticipates that by the end of the first quarter next year, inflation may fall to just “under 4%”, leaving an additional 2% reduction to reach the BoE’s target.

This remaining gap, Bailey noted, is the challenging part, emphasizing that “the second half, from there to two, is hard work.”

Moreover, Bailey explicitly pushes back against assumptions of imminent interest rate cuts, stating it’s “too soon to have that discussion.”

BoJ’s Ueda repeats uncertainty on stably achieving inflation target

In today’s address to the parliament, BoJ Governor Kazuo Ueda provided note that the economy is “recovering moderately,” which is further evidenced by the narrowing of the output gap to “near zero”.

Ueda also highlighted “We’re seeing some positive signs in wages and inflation”. However, he tempered this optimism by acknowledging the “high uncertainty on whether this cycle will strengthen”

A key point in Ueda’s commentary was BoJ’s stance on inflation. Despite the positive signs, he stated that the central bank cannot yet assert with confidence that inflation will sustainably and stably achieve its 2% target.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2548; (P) 1.2581; (R1) 1.2638; More…

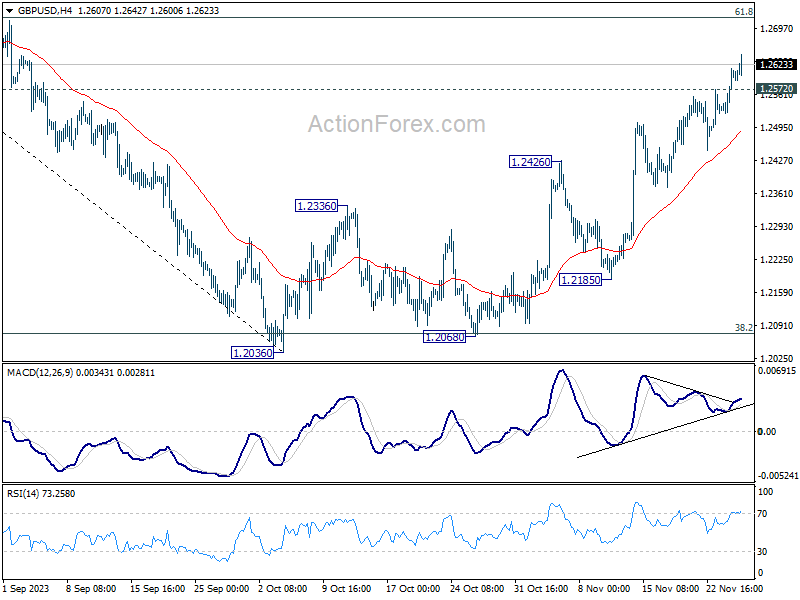

GBP/USD hits as high as 1.2642 so far as rise from 1.2036 continues today. Intraday bias stays on the upside at this point. Next target is 61.8% retracement of 1.3141 to 1.2036 at 1.2716. On the downside, below 1.2572 minor support will turn intraday bias neutral first. But further rally will now remain in favor as long as 1.2426 resistance turned support holds.

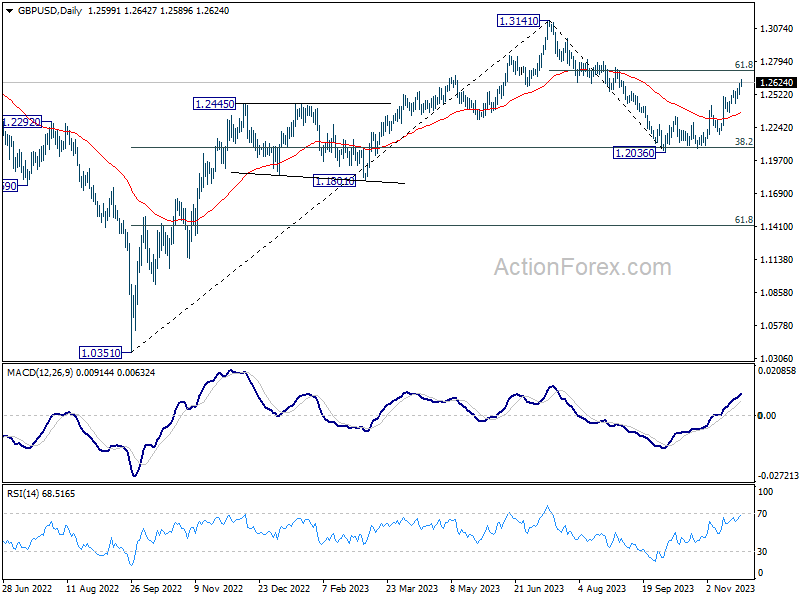

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 suggests that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Oct | 2.30% | 2.10% | 2.10% | |

| 15:00 | USD | New Home Sales M/M Oct | 725K | 759K |