{kind=link}

Forex markets today are leaning towards mild risk-off sentiment, with traders cautiously awaiting comments from leading central bankers at the ECB forum. This cautious sentiment, interestingly, does not seem to be having a substantial effect on the stock or bond markets yet.

British Pound is experiencing fresh selling, despite expectations of hawkish messages from the head of BoE. Meanwhile, Australian and New Zealand dollars are faring even worse, as they continue to suffer from the aftermath of disappointing Australian CPI data.

On the other hand, Dollar is showing signs of strength at present. Yen is trying to recovery, but still lacks convincing momentum. Euro and Swiss Franc lag slightly behind the greenback and Yen. Let’s see how much the picture would change after the central bankers’ speeches.

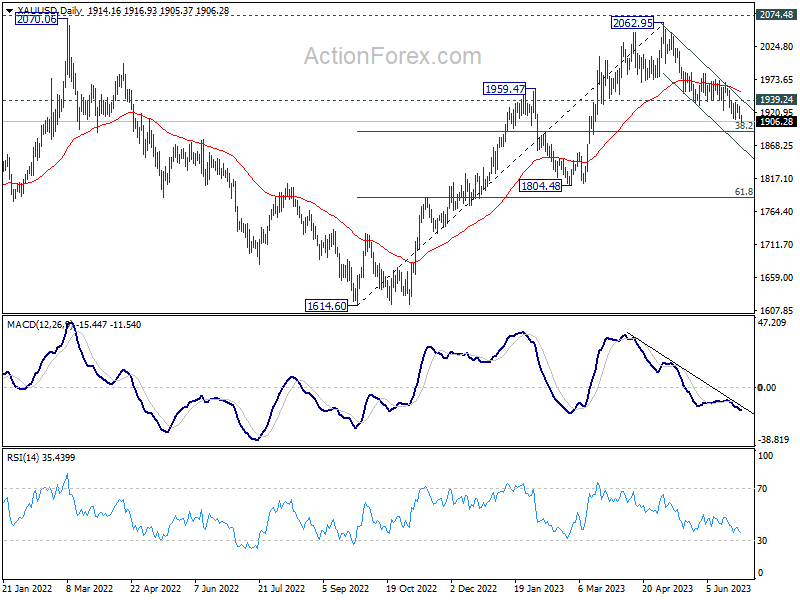

Technically, Gold’s fall from 2062.95 is also extending lower today, on the back of Dollar’s recovery. Next focus will be on whether there is enough support from 38.2% retracement of 1614.60 to 2062.95 at 1891.68 to bring rebound. Break of 1939.24 minor resistance will be the first sign of bottoming. However, sustained break of 1891.68 would open up deeper fall to 1804.48, and possibly to 61.8% retracement at 1785.86.

In Europe, at the time of writing, FTSE is up 0.71%. DAX is up 0.70%. CAC is up 0.77%. Germany 10-year yield is down -0.035 at 2.325. Earlier in Asia, Nikkei rose 2.02%. Hong Kong HSI rose 0.12%. China Shanghai SSE closed flat. Singapore Strait Times rose 0.06%. Japan 10-year JGB yield rose 0.138 to 0.388.

US goods exports down -7.5% yoy in May, imports down -8.8% yoy

US goods exports dropped -7.5% yoy to USD 162.84B in May. Goods imports dropped -8.8% yoy to USD 253.98B. Goods trade deficit came in at USD -91.1B, versus expectation of USD -92.3B.

Wholesale inventories fell -0.1% mom to USD 912.9B. Retail inventories rose 0.8% mom to USD 787.7B.

ECB de Guindos: July a hike fait acommpli, September open

ECB Vice President Luis de Guindos has provided a somber outlook for the Eurozone’s economic performance, emphasizing both stubborn inflation pressures and slower economic growth in an interview with Bloomberg TV in Sintra, Portugal.

When discussing the ECB’s potential interest rate policy moves, de Guindos indicated that the decision to hike rates in July seems to be a “fait accompli”, while the situation for September is “open”.

De Guindos voiced his concerns about underlying inflation, which he expects to prove more stubborn than currently anticipated. The Vice President linked these persistent pressures to a potentially strong summer tourist season that could drive services costs higher.

Regarding the economy, “the data that we are receiving about growth are not very good,” he confessed, adding that “some of these downside risks have started to materialize and are becoming much more visible.”

ECB Vasle: Burden of proof for Sep in non-necessity of more hike

ECB Governing Council member Bostjan Vasle has emphasized the need for further monetary tightening in the face of persistent inflation, speaking on the sidelines of the ECB Forum.

“Given the persistence of inflation, we need to keep tightening monetary policy at our next meeting,” Vasle stated.

Beyond July, the decision to further hike rates will be “data-dependent”. However, Vasle conveyed that the “burden of proof” lies in data indicating “further rate hike is not needed instead that it is needed.”

Vasle dismissed arguments that weaker growth readings might ease the ECB’s fight against inflation. He asserted, “All these suggest that growth developments are not significantly different than our most recent projections.”

The ECB official also expressed concerns over expectations that corporate profit margins might decline and absorb the impact of wage hikes, terming such a prospect as bearing significant risks.

“The labour market is strong and consumption is resilient. So firms might continue to enjoy pricing power, especially because demand is too strong to push down margins,” he said.

Germany Gfk consumer sentiment fell to -25.4, first setback after eight increases

German Gfk Consumer Sentiment for July fell from -24.4 to -25.4, below expectation of 23.0. In June, economic expectations fell from 12.3 to 3.7. Income expectations fell from -8.2 to -10.6. Propensity to buy improved from -16.1 to -14.6.

“The current development in consumer sentiment indicates that consumers are once again more uncertain. This is reflected in the fact that the propensity to save increased again this month,” explains Rolf Bürkl, GfK consumer expert.

“After eight consecutive increases, the consumer sentiment must suffer a first setback. Continued high inflation rates, currently at around six percent, are noticeably eroding the purchasing power of households and preventing private consumption from making a positive contribution.”

Australia CPI slowed to 5.6% yoy in May, lowest in more than a year

Australia monthly CPI slowed notably from 6.8% yoy to 5.6% yoy in May, below expectation of 6.1% yoy. That’s also the lowest reading in more than a year since April 2022. Excluding volatile items and travel, CPI also ticked down from 6.5% yoy to 6.4% yoy.

The most significant contributors to the annual increase in the monthly CPI indicator in May were Housing (+8.4 per cent), Food and non-alcoholic beverages (+7.9 per cent), and Furniture, household equipment and services (+6.0 per cent). Partly offsetting the rise was a fall in Automotive fuel (-8.0 per cent).

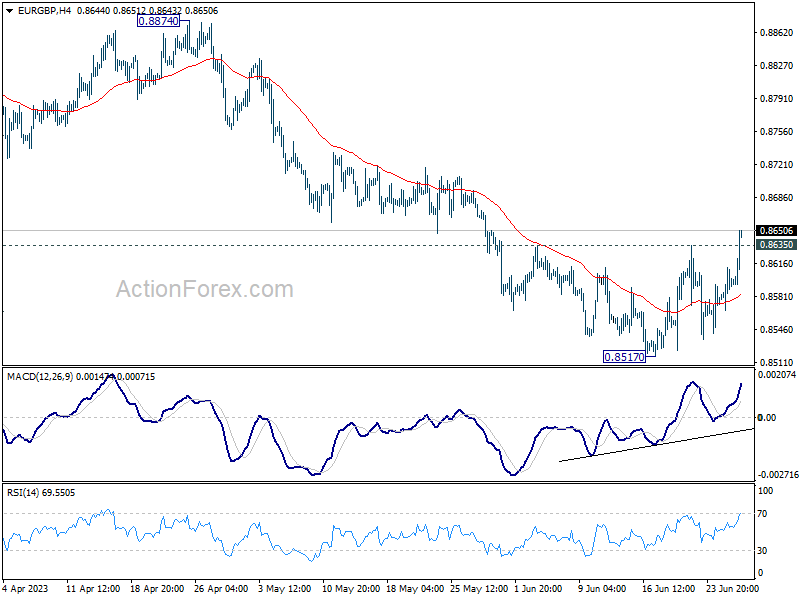

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8573; (P) 0.8593; (R1) 0.8618; More…

EUR/GBP’s break of 0.8635 resistance confirms short term bottoming at 0.8517, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for 55 D EMA (now at 0.8658) and above. For now, as long as 0.8717 support turned resistance holds, fall from 0.8977 could still have another leg through 0.8517 before completion. However, firm break of 0.8717 will turn outlook bullish for 0.8977 resistance next.

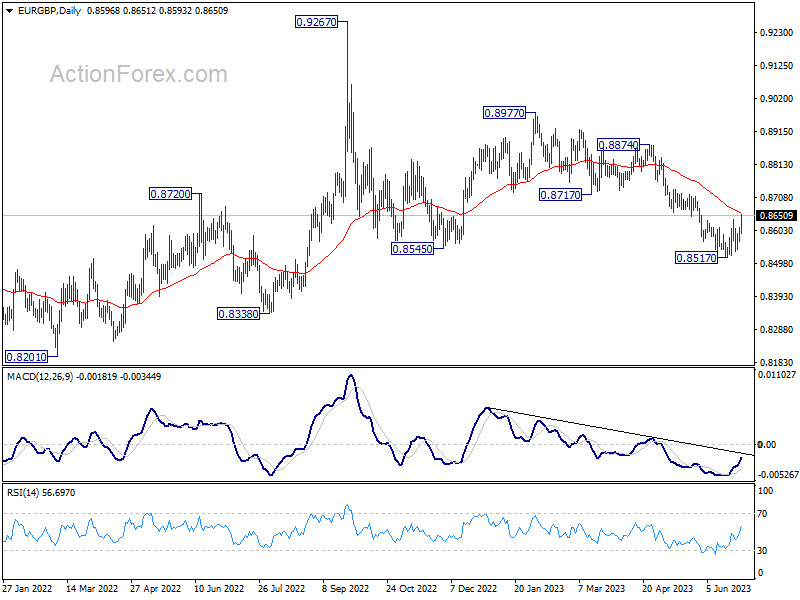

In the bigger picture, the down trend from 0.9267 (2022 high) is still in progress. It’s seen as part of the long term range pattern from 0.9499 (2020 high). Deeper fall could be seen towards 0.8201 (2022 low). But strong support should be seen from there to bring reversal. This will now remain the favored case as long as 0.8717 support turned resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y May | 5.60% | 6.10% | 6.80% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Jul | -25.4 | -23 | -24.2 | -24.4 |

| 08:00 | CHF | Credit Suisse Economic Expectations Jun | -30.8 | -32.2 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y May | 1.40% | 1.50% | 1.90% | |

| 12:30 | USD | Goods Trade Balance (USD) May P | -91.1B | -92.3B | -96.8B | |

| 12:30 | USD | Wholesale Inventories May P | -0.10% | 0.10% | -0.10% | |

| 14:30 | USD | Crude Oil Inventories | -1.4M | -3.8M |