{kind=link}

Australian Dollar is experiencing a wild ride this week, tumbling in Asian trading hours due to lower-than-anticipated CPI results. The “encouraging” data has raised speculation about a potential pause in RBA’s tightening plans next week. There are also talks that the hike month was the last in the cycle. This decline is also dragging down New Zealand Dollar, which is following suit as one of today’s weakest performers.

Japanese Yen, meanwhile, is attempting to recover from its losses, but with limited success. Market chatter suggests that the Japanese government is likely to resort to verbal intervention tactics until 150 level against Dollar is under serious threat, reserving actual market intervention as a last resort. Dollar is faring marginally better, gaining some ground, albeit without much enthusiasm when matched up against European currencies.

Today’s economic data release schedule remains light, shifting investor attention towards the upcoming remarks from top officials of Fed, ECB, BoJ and BoE at the ECB Forum, in Sintra, Portugal

Technically, some attention should be paid on developments in the US stock markets for the rest of the week. Yesterday’s strong bounce in S&P 500 affirms the case that fall from 4448.47 is merely a near term pull back. Up trend from 3491.58 is not being threatened with 4261.07 support safe by a big margin. Further rise in S&P 500 will put 4448.47 short term top in focus in the early part of next week, for reacting the heavy weight US data like NFP.

In Asia, at the time of writing, Nikkei is up 1.60%. Hong Kong HSI is down -0.13%. China Shanghai SSE is down -0.52%. Singapore Strait Times is up 0.14%. Japan 10-year JGB yield is up 0.0118 at 0.393. Overnight, DOW rose 0.63%. S&P 500 rose 1.15$. NASDAQ rose 1.65%. 10-year yield rose 0.049 to 3.768.

Australia CPI slowed to 5.6% yoy in May, lowest in more than a year

Australia monthly CPI slowed notably from 6.8% yoy to 5.6% yoy in May, below expectation of 6.1% yoy. That’s also the lowest reading in more than a year since April 2022. Excluding volatile items and travel, CPI also ticked down from 6.5% yoy to 6.4% yoy.

The most significant contributors to the annual increase in the monthly CPI indicator in May were Housing (+8.4 per cent), Food and non-alcoholic beverages (+7.9 per cent), and Furniture, household equipment and services (+6.0 per cent). Partly offsetting the rise was a fall in Automotive fuel (-8.0 per cent).

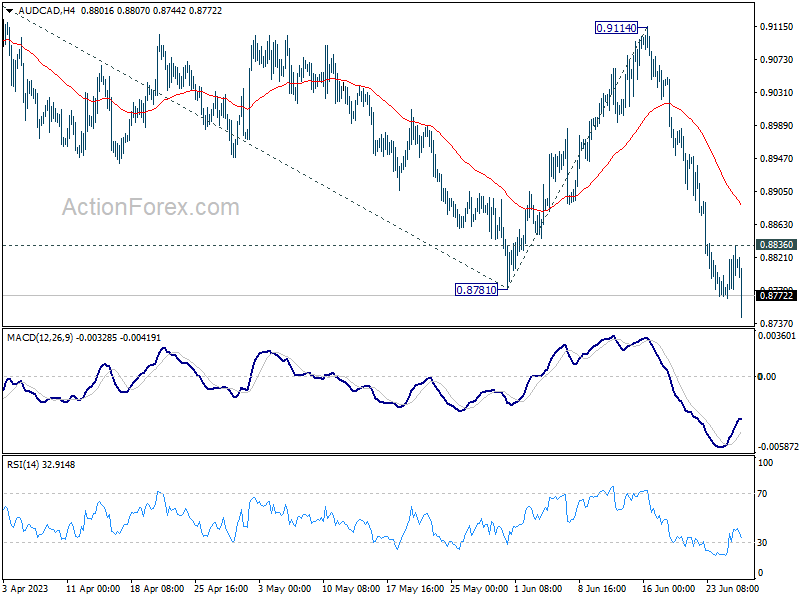

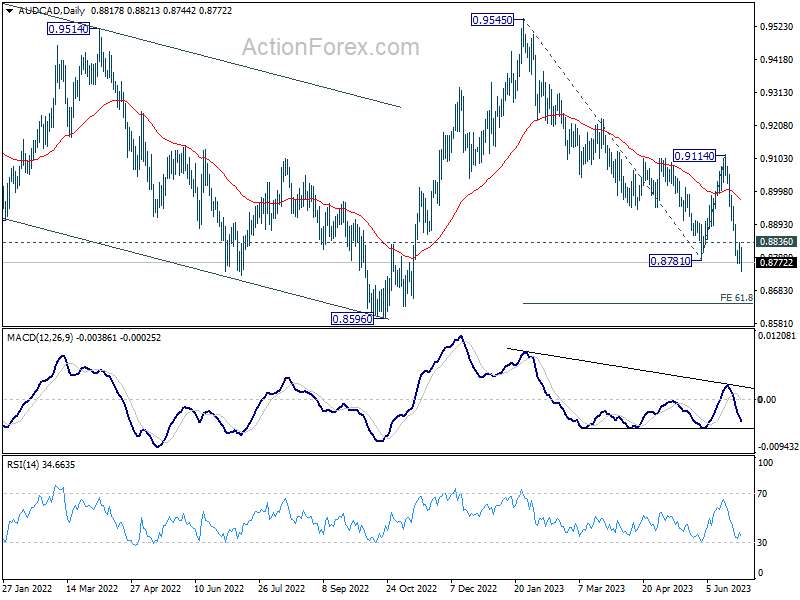

AUD/CAD’s fall taking off after CPI from AU and CA

Australian Dollar falls broadly after data showed that CPI slowed much more than expected in May. Some economists are now seeing consumer inflation, at 5.6% and around the very lower end of forecasts, being soft enough to give confidence for RBA to pause again next week. On the other hand, without any downside surprise from Canadian CPI released overnight, BoC is more likely to continue tightening next month than not.

AUD/CAD’s decline could finally be taking off with today’s selloff. Technically, further fall is expected as long as 0.8836 minor resistance holds. The whole fall from 0.9545 should target 61.8% projection of 0.9545 to 0.8781 from 0.9114 at 0.8642, or further to 0.8596 (2022 low). Nevertheless, break of 0.8836 will argue that the sentiment could have flipped again and mix up the outlook.

Looking ahead

Germany Gfk consumer sentiment, Swiss Credit Suisse economic expectations and Eurozone M3 will be released in European session. US will release goods trade balance later in the day.

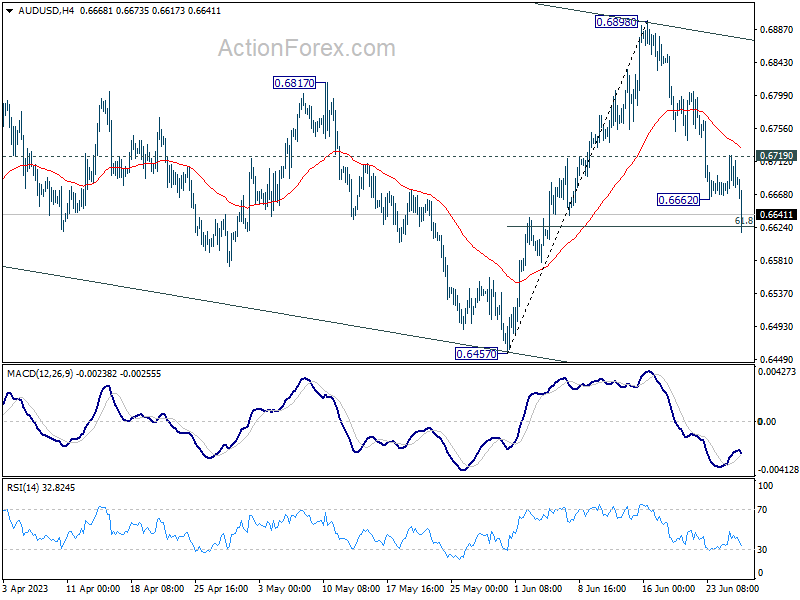

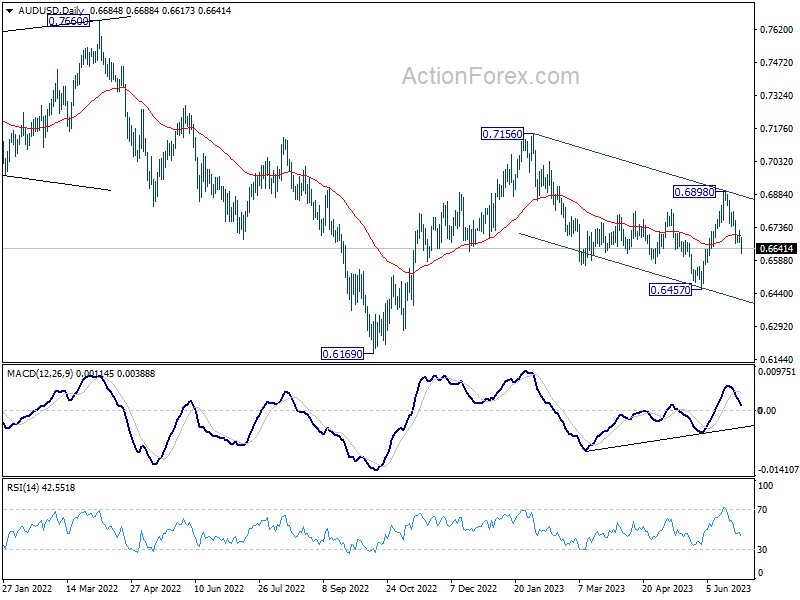

AUD/USD Daily Report

Daily Pivots: (S1) 0.6663; (P) 0.6692; (R1) 0.6716; More…

AUD/USD’s fall from 0.6898 resumed after brief recovery and intraday bias is back on the downside. Sustained break of 61.8% retracement of 0.6457 to 0.6898 at 0.6625 will path the way back to 0.6457 key support level. On the upside, above 0.6719 resistance will turn intraday bias neutral again first.

In the bigger picture, outlook is mixed up by the deeper the expected pull back from 0.6898. Still, price actions from 0.7156 are seen as a correction to rebound from 0.6169. Break of 0.6457 will resume the fall towards 0.6169 low. On the upside, though, break of 0.6898 resistance will argue that rise from 0.6169 is ready to resume through 0.7156.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y May | 5.60% | 6.10% | 6.80% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence (Jul) | -23 | -24.2 | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Jun | -32.2 | |||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y May | 1.50% | 1.90% | ||

| 12:30 | USD | Goods Trade Balance (USD) May P | -92.3B | -96.8B | ||

| 12:30 | USD | Wholesale Inventories May P | 0.10% | -0.10% | ||

| 14:30 | USD | Crude Oil Inventories | -1.4M | -3.8M |