{kind=link}

New Zealand Dollar falls broadly today as the markets considered the RBNZ rate hike as a dovish one, probably with interest rate already peaked. The development also takes Aussie lower too. Meanwhile, Sterling is attempting a bounce after strong core CPI reading, as well as services prices. But buyers of the Pound appear to be hesitating for now. Euro is also slightly firmer but there is no apparent momentum except versus commodity currencies. Dollar and Yen are mixed, awaiting further guidance from overall risk sentiment.

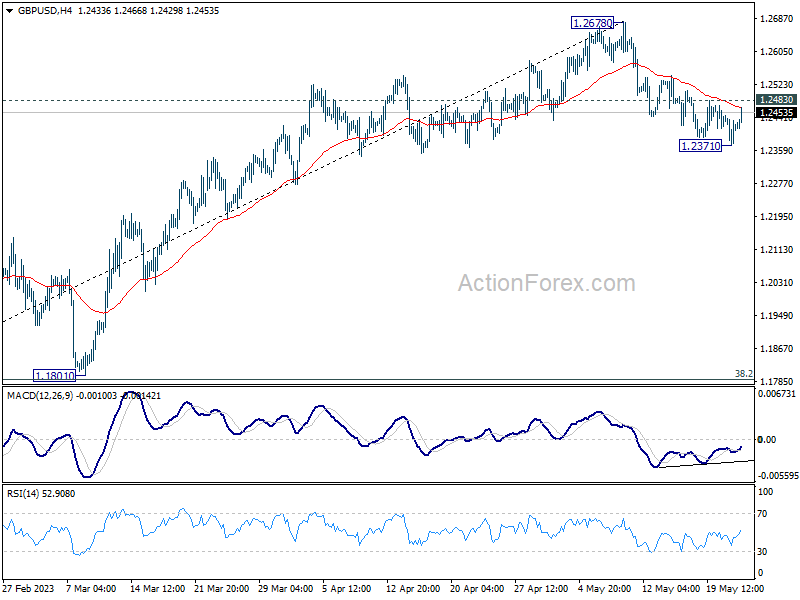

Technically, one focus for the rest of the day would be on whether Sterling could extend its rebound attempt. EUR/GBP has already breached 0.8660 temporary low too, and it’s on track to resume the decline from 0.8977. Levels to watch include 1.2483 minor resistance in GBP/USD, and 172.60 temporary top in GBP/JPY. Break of these levels would mark a stronger come back in the Pound.

In Asia, Nikkei closed down -0.89%. Hong Kong HSI is down -1.17%. China Shanghai SSE is down -0.89%. Singapore Strait Times is down -0.30%. Japan 10-year JGB yield is up 0.0089 at 0.413. Overnight, DOW dropped -0.69%. S&P 500 dropped -1.12%. NASDAQ drooped -1.26%.

UK CPI slowed to 8.7%, CPI core rose to highest since 1992

UK CPI slowed from 10.1% yoy to 8.7% yoy in April, above expectation of 8.2% yoy. On a monthly basis, CPI rose by 1.2% mom, above expectation of 0.8% mom.

CPI core (excluding energy, food, alcohol and tobacco) rose from 6.2% yoy to 6.8% yoy, above expectation of 6.2% yoy. That’s the highest level since March 1992.

CPI goods annual rate eased from 12.8% yoy to 10.0% yoy, while the CPI services annual rate rose from 6.6% yoy to 6.9% yoy.

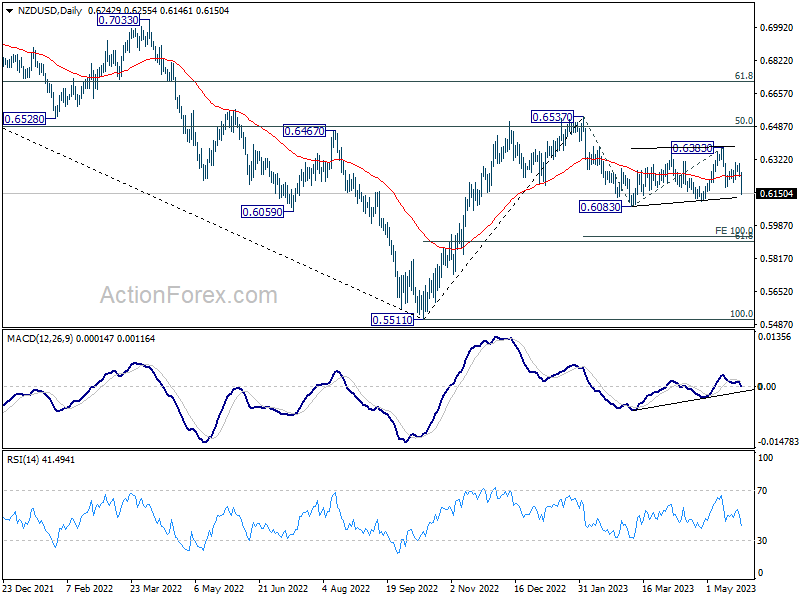

NZD/USD dives after dovish RBNZ hike

RBNZ raised OCR by 25bps to 5.50% today, reaching the projected peak interest rate. The decision was made by a 5-2 vote, with two committee members voted for no change. The central bank noted that “The OCR will need to remain at a restrictive level for the foreseeable future, to ensure that consumer price inflation returns to the 1% to 3% annual target range, while supporting maximum sustainable employment.”

The overall announce was seen as being dovish by the markets, sending New Zealand Dollar broadly lower. NZD/USD’s break of 0.6181 support confirms resumption of the decline from 0.6383 for retesting 0.6083/0.6110 support zone.

More importantly, the development is inline with the view that corrective pattern from 0.6083 has completed with three waves up to 0.6383. That is, the decline from 0.6537 might be ready to resume too. Firm break of 0.6083 will target 100% projection of 0.6537 to 0.6083 from 0.6383 at 0.5929.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2376; (P) 1.2412; (R1) 1.2450; More…

Intraday bias in GBP/USD is turned neutral with current recovery. Another fall is expected as long as 1.2483 resistance holds. Break of 1.2371, and sustained trading below 55 D EMA (now at 1.2397) will confirm that it’s in correction to whole up trend from 1.0351. Deeper fall should then be seen to 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789). On the upside, however, break of 1.2483 resistance will bring stronger rebound back to retest 1.2678 high instead.

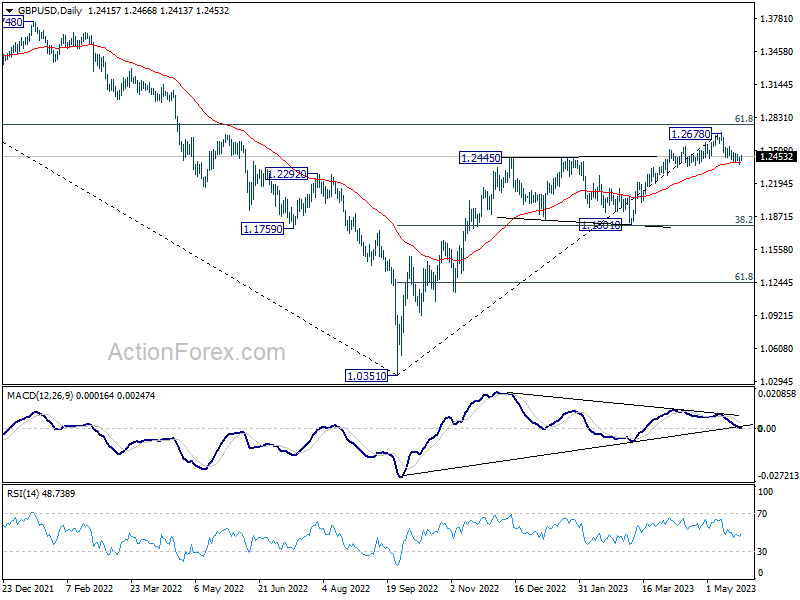

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Q/Q Q1 | -1.40% | 0.20% | -0.60% | -1.00% |

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q1 | -1.10% | -1.00% | -1.30% | -1.60% |

| 00:30 | AUD | Westpac Leading Index M/M Apr | 0.00% | 0.00% | ||

| 02:00 | NZD | RBNZ Rate Decision | 5.50% | 5.50% | 5.25% | |

| 03:00 | NZD | RBNZ Press Conference | ||||

| 06:00 | GBP | CPI M/M Apr | 1.20% | 0.80% | 0.80% | |

| 06:00 | GBP | CPI Y/Y Apr | 8.70% | 8.20% | 10.10% | |

| 06:00 | GBP | Core CPI Y/Y Apr | 6.80% | 6.20% | 6.20% | |

| 06:00 | GBP | RPI M/M Apr | 1.50% | 1.70% | 0.70% | |

| 06:00 | GBP | RPI Y/Y Apr | 11.40% | 11.20% | 13.50% | |

| 06:00 | GBP | PPI Input M/M Apr | -0.30% | -0.50% | 0.20% | |

| 06:00 | GBP | PPI Input Y/Y Apr | 3.90% | 3.80% | 7.60% | 7.30% |

| 06:00 | GBP | PPI Output M/M Apr | 0.00% | -0.10% | 0.10% | 0.00% |

| 06:00 | GBP | PPI Output Y/Y Apr | 5.40% | 7.40% | 8.70% | 8.50% |

| 06:00 | GBP | PPI Core Output M/M Apr | 0.00% | 0.10% | 0.30% | |

| 06:00 | GBP | PPI Core Output Y/Y Apr | 6.00% | 7.30% | 8.50% | 8.30% |

| 08:00 | EUR | Germany IFO Business Climate May | 93.4 | 93.6 | ||

| 08:00 | EUR | Germany IFO Current Assessment May | 95.2 | 95 | ||

| 08:00 | EUR | Germany IFO Expectations May | 91.7 | 92.2 | ||

| 14:30 | USD | Crude Oil Inventories | 1.5M | 5.0M | ||

| 18:00 | USD | FOMC Minutes |