{kind=link}

Euro is making broad gains in Asian session, fueled by hawkish comments from a top ECB official who suggested that the next rate hike could be a 50bps one. Euro’s strength is also lifting the Swiss Franc, while Sterling remains firm but lags slightly behind. In contrast, Australian and Canadian dollars are underperforming, with the Aussie looking particularly vulnerable ahead of tomorrow’s CPI report and facing additional pressure from selling in cross against New Zealand Dollar.

Yen is also weak as markets anticipate BoJ will maintain its current policy stance unchanged at this week’s meeting. Mild risk aversion in Asian stocks is providing slight support for the Japanese currency, but this may be short-lived. Dollar is mixed for now, alongside US stocks and bonds, but could be vulnerable to an extended selloff against European majors if key support levels are decisively broken.

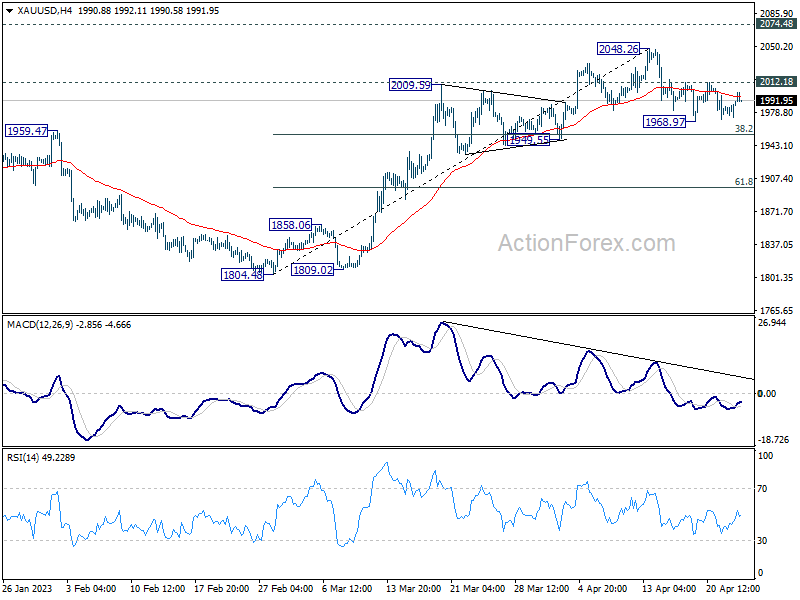

Technically, Gold appears to be attempting to find a bottom ahead of 38.2% retracement of 1804.48 to 2048.26 at 1955.13. Break of 2012.18 resistance could signal that correction from 2048.26 is complete, potentially leading to a strong rally through 2048.26 and towards record high of 2074.48. If realized, this move may coincide with break of 1.1075 in EUR/USD, regardless of which one occurs first.

In Asia, at the time of writing, Nikkei is up 0.14%. Hong Kong HSI is down -1.62%. China Shanghai SSE is down -0.35%. Singapore Strait Times is down -0.80%. Japan 10-year JGB yield is up 0.0117 at 0.484. Overnight, DOW rose 0.20%. S&P 500 rose 0.09%. NASDAQ dropped -0.29%. 10-year yield dropped -0.055 to 3.515.

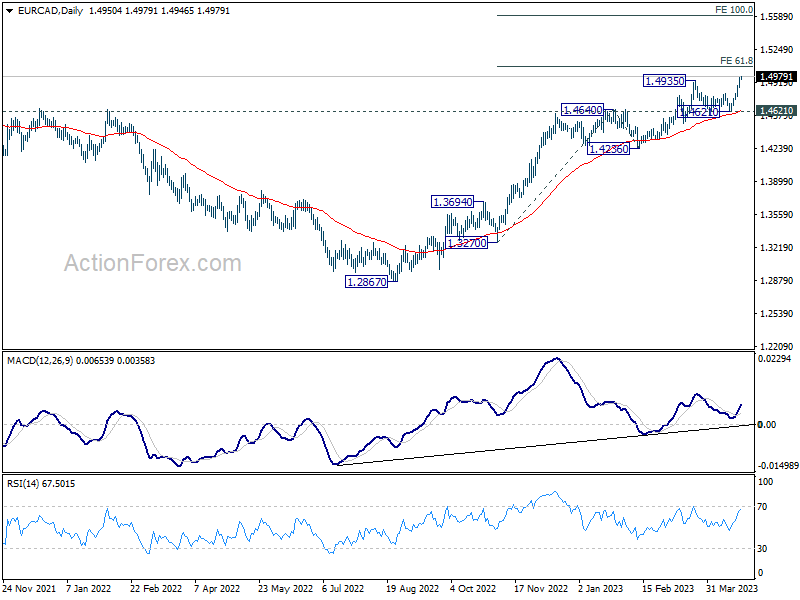

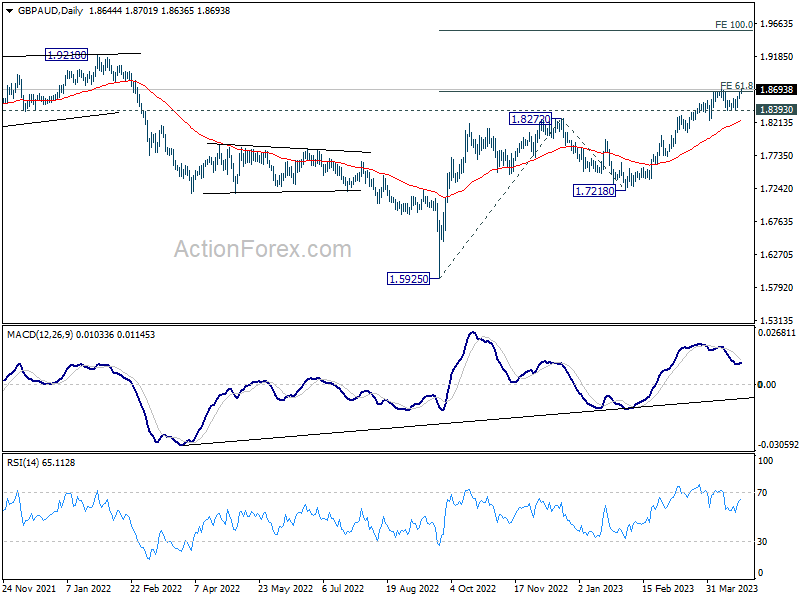

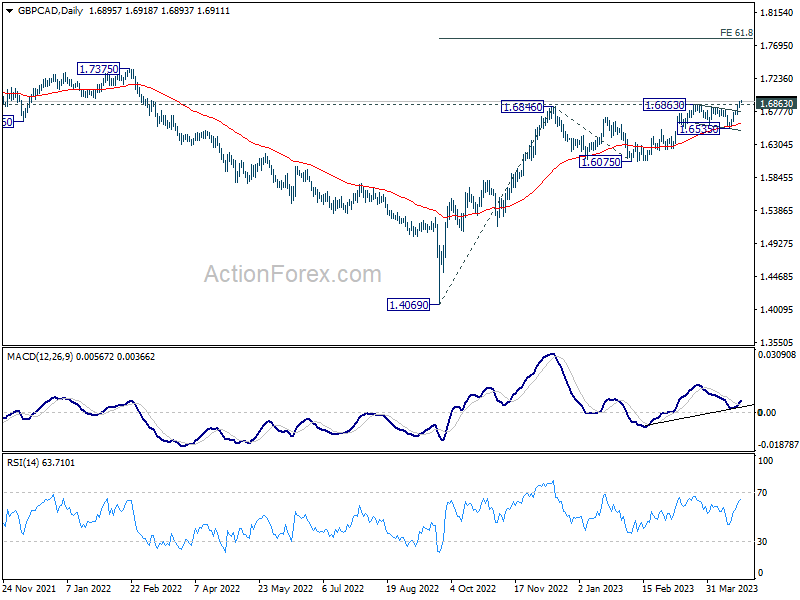

EUR/AUD, EUR/CAD, GBP/AUD, GBP/CAD uptrend resumptions

Both Euro and Sterling staged upside breakout against Australian and Canadian Dollar this week, resuming respective medium term up trend. Comments from a top ECB official overnight indicates that a 50bps is not off the table for May policy meeting. Meanwhile, recent data from the UK clearly indicates the need for extended tightening from BoE to fight the still-double-digit inflation. On the other hand, there is no data supporting BoC to move out from its pause. Aussie looks vulnerable to tomorrow’s CPI release, which would be crucial to whether RBA would deliver a final hike in the currency cycle.

EUR/AUD’s up trend from 1.4281 is now in progress for 100% projection of 1.4281 to 1.5976 from 1.5254 at 1.6949. Near term outlook will stay bullish as long as 1.6219 support holds, in case of retreat.

EUR/CAD’s break of 1.4935 confirmed resumption of whole up trend from 1.2867. Immediate target is 61.8% projection of 1.3270 to 1.4640 from 1.4236 at 1.5083. Sustained break there could prompt upside acceleration to 100% projection at 1.5606. Meanwhile, outlook will stay bullish as long as 1.4261 support holds, in case of retreat.

GBP/AUD’s breach of 1.8697 resistance argues that uptrend from 1.5925 is resuming. Outlook will stay bullish as long as 1.8393 support holds, in case of retreat. Sustained trading above 61.8% projection of 1.5925 to 1.8272 from 1.7218 at 1.8668 could prompt upside acceleration to 1.9218 resistance and then 100% projection at 1.9565.

GBP/CAD’s break of 1.6846 resistance also indicates resumption of up trend from 1.4069. Near term outlook will stay bullish as long as 1.6535 support holds. Current rise should target 61.8% projection of 1.4069 to 1.6846 from 1.6075 at 1.7791 next.

ECB’s Schnabel: Further rate hikes needed, 50 not off the table

ECB Executive Board member Isabel Schnabel said in a Politico interview that additional rate hikes are necessary, with the size of these hikes depending on incoming data. “The data we have so far shows that inflation is higher and the economy more resilient than projected,” she added that “data dependence means that 50 basis points are not off the table” for May meeting.

She also noted that “it’s far too early to declare victory on inflation.” She explained that if core inflation remains high and persistent, even if it reaches a peak, the information content of that data point might be limited. “So what we really need is confidence that it’s actually coming down in a sustained manner.”

Schnabel acknowledged that she cannot predict the terminal interest rate, noting that rates must be set on a meeting-to-meeting basis. She also addressed concerns about a potential recession, stating, “So far, there are no particular signs of a weakening in economic developments. At this point in time, I have no reason to believe that a recession is coming.”

ECB’s Makhlouf: Too early to start planning for a pause

ECB Governing Council member Gabriel Makhlouf stated in a blog post that it is too early to plan for a pause in tightening of monetary policy, emphasizing the need to focus on incoming data. In a blog post, Makhlouf said, “on the evidence so far, it is too early to start planning for a pause in our tightening of policy.” He further noted that based on current evidence, restrictive rate levels are necessary to balance supply and demand in the economy and reduce inflation.

In separate occasion, another Governing Council member François Villeroy de Galhau emphasized the role of climate change in affecting price stability and economic activity. He highlighted that addressing climate change is not an instance of mission creep or politicization, but rather a core duty of central banks worldwide. Villeroy stated, “It’s not mission creep, it’s not a politicisation of our mandate – it is our core business and core duty.”

BoJ Governor Ueda stresses need for continued monetary easing

BoJ Governor Kazuo Ueda addressed parliament today, emphasizing, “In light of current economic, price and financial developments, it’s appropriate to maintain monetary easing, now conducted through yield curve control.”

Ueda reiterated the importance of keeping Japan’s monetary policy loose to achieve the 2% inflation target in a sustainable and stable manner, along with wage hikes. He added that if wage growth and inflation accelerate faster than expected and require tightening monetary policy, BoJ is prepared to respond by raising interest rates.

Despite this, Ueda warned of the risk of inflation falling further below expectations, calling it “very worrying.” He noted that “the risk of inflation undershooting forecasts is bigger than the risk of overshooting,” emphasizing the need to maintain the BoJ massive stimulus for the time being.

Looking ahead

Swiss trade balance and UK public sector net borrowing will be released in European session. Later in the day, US will release house price index, consumer confidence and new home sales.

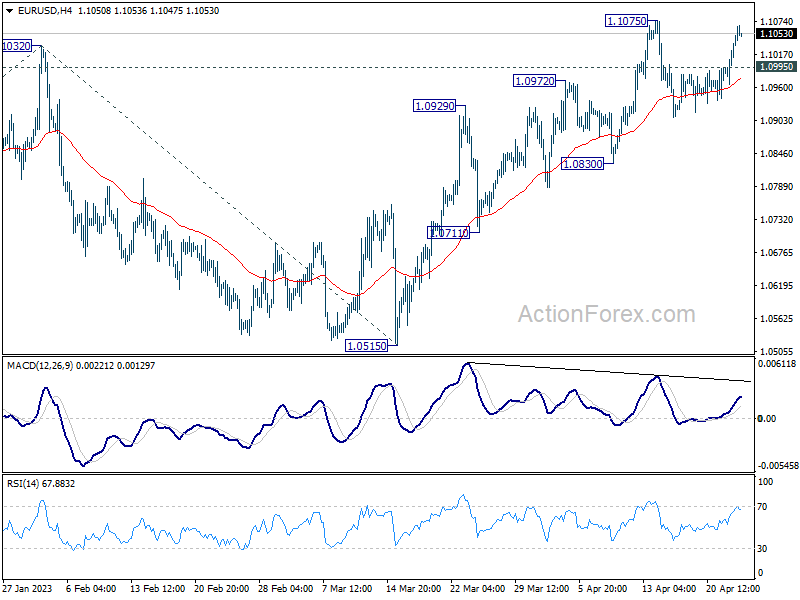

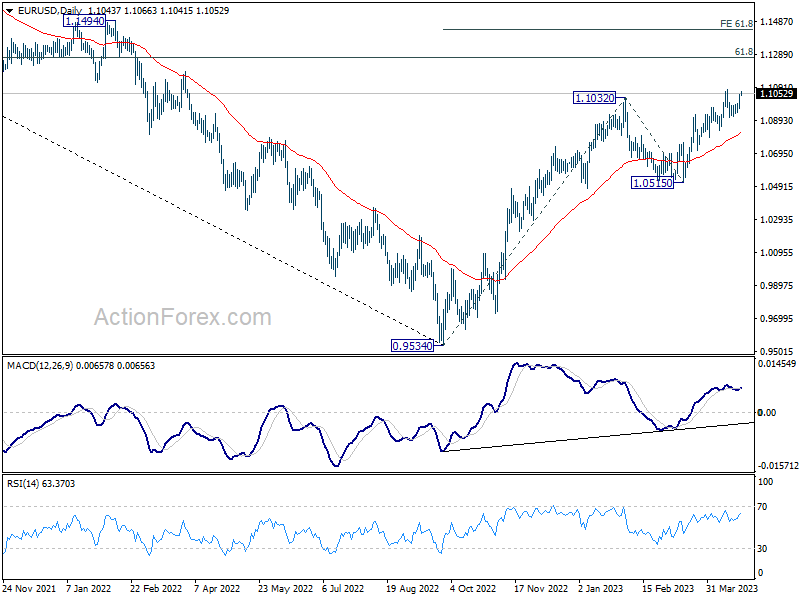

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0992; (P) 1.1021; (R1) 1.1076; More…

Immediate focus is now on 1.1075 resistance in EUR/USD as rebound extends today. Decisive break there will resume larger up trend from 0.9534 to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441. On the downside, break of 1.0995 minor support will now indicate that corrective pattern from 1.1075 is extending with one more falling leg before completion.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Mar | 1.60% | 1.60% | 1.80% | 1.70% |

| 06:00 | CHF | Trade Balance (CHF) Mar | 4.20B | 3.31B | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Mar | 12.2B | 15.9B | ||

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Feb | 1.80% | 2.50% | ||

| 13:00 | USD | Housing Price Index M/M Feb | -0.20% | 0.20% | ||

| 14:00 | USD | Consumer Confidence Apr | 104.1 | 104.2 | ||

| 14:00 | USD | New Home Sales Mar | 630K | 640K | ||

| 22:45 | NZD | Trade Balance (NZD) Mar | -500M | -714M |