{kind=link}

New Zealand Dollar dropped broadly in Asian session today after a lower-than-expected consumer inflation reading increased speculation that the next RBNZ rate hike may be the last in the current cycle. This development also pulled Australian Dollar down, making them the day’s worst performers so far. In contrast, Swiss Franc and Euro are trading higher, followed by US Dollar and Japanese Yen, suggesting that the markets are not in a risk-on mood. British Pound and Canadian Dollar are currently mixed.

For the week, the Pound is the strongest currency, bolstered by this week’s employment and inflation data, which likely paves the way for another BoE rate hike in May and possibly more afterwards. Dollar is the second strongest, supported by a rebound in treasury yields. Meanwhile, New Zealand Dollar is the weakest, followed by Canadian Dollar and Japanese Yen. Australian Dollar remains resilient, while the Euro’s direction is unclear.

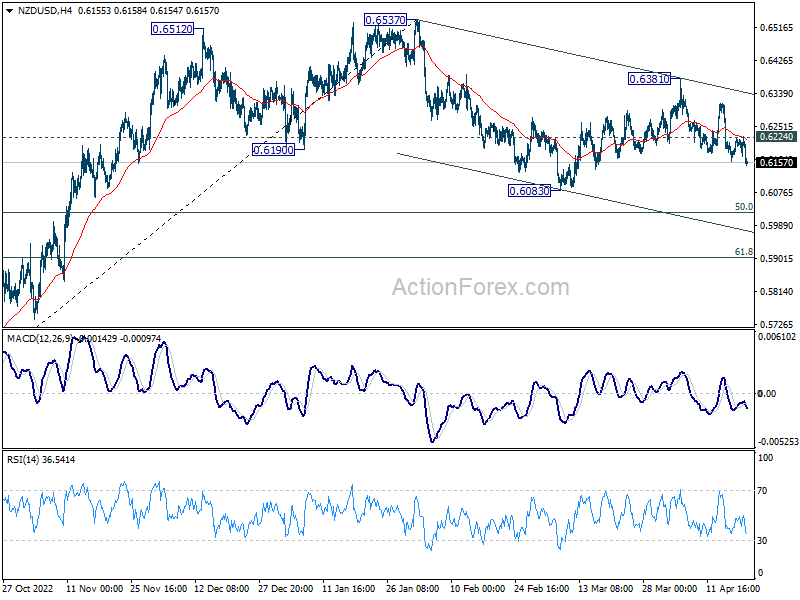

Technically, NZD/USD has resumed its decline from 0.6381 following the release of New Zealand’s CPI data. Intraday bias is back on the downside, targeting 0.6083 support level and below. However, without strong downward acceleration, significant support could emerge around 50% retracement of 0.5511 to 0.6537 at 0.6024, potentially leading to a rebound and completing the overall corrective pattern from the 0.6537 high.

In Asia, at the time of writing, Nikkei is up 0.28%. Hong Kong HSI is up 0.01%. China Shanghai SSE is down -0.52%. Singapore Strait Times is down -0.49%. Japan 10-year JGB yield is down -0.0060 at 0.472. Overnight, DOW dropped -0.23%. S&P 500 dropped -0.01%. NASDAQ rose 0.03%. 10-year yield rose 0.030 to 3.602.

ECB Schnabel emphasizes data-driven approach amid banking sector disturbances

European Central Bank (ECB) Executive Board member Isabel Schnabel emphasized the importance of a data-driven approach to policy decisions in light of recent disturbances in the banking sector. She stated yesterday, “I can’t tell you what we’ll decide at the next meeting, and especially at the following meetings,” adding that the situation has become “even more complex.”

Schnabel noted the significance of monitoring the potential impact of banking sector uncertainty on lending, saying, “It’s even more important that we look at all the data we’ll get. It’s important whether the uncertainty in the banking sector will have an additional impact on lending.”

When discussing the ECB’s future plans for its balance sheet, Schnabel admitted that the endpoint remains uncertain and is currently under discussion. She emphasized the need to manage the balance sheet in a way that markets can digest during these turbulent times and expressed satisfaction with the current approach, stating, “So far, it’s worked extraordinarily well.”

Fed Williams sees continuing trend of slowing inflation

New York Fed President John Williams emphasized the need to utilize monetary policy tools to achieve price stability during a speech at the Money Marketeers of New York University. He expressed confidence in attaining a sufficiently restrictive stance to bring inflation down to Fed’s 2% longer-run goal

Williams noted that “the most recent data indicate that this trend of slowing inflation is continuing.” He expects PCE core inflation to ease to 3.25% this year and reaching the 2% target within the next two years. He also commented on the labor market, calling it “very tight” but showing some signs of cooling. Williams expects the unemployment rate to rise to between 4% and 4.5% over the next year, with growth moderating this year before rebounding next year.

Additionally, Williams addressed the recent major bank collapse in the US, stating that the banking system remains sound and resilient. However, he anticipates that the collapse will result in tighter credit conditions for households and businesses, which could impact spending. Williams highlighted the importance of closely monitoring credit conditions and their potential effects on the economy.

Fed’s Goolsbee discusses May FOMC Prospects, robust job market, and lingering inflation concerns

Chicago Fed President Austan Goolsbee discussed the upcoming May FOMC meeting, the strength of the job market, and persistent inflation in an interview. Goolsbee cautioned against reading too much into his stance on interest rates, stating, “We still got a couple of weeks before the actual meeting, so if anybody imputed some specific basis points of what I was for, that’d be inaccurate.”

Goolsbee acknowledged the strong job market as the most robust part of the economy, with “unprecedented numbers,” while noting that inflation remains a concern. He said, “Inflation — there’s been some improvement, but in a way that’s the worst part of the economy,” adding that it has been “more persistent than we wanted.”

As for the potential impact of the recent failure of two US banks on the economy, Goolsbee said it is essential to monitor the extent of the slowdown. He explained, “How much squeezing is going to be coming from the bank side I think is going to matter for whether this economy is going to slow down.” Goolsbee emphasized that the intensity of the anticipated growth slowdown in the second half of the year would depend significantly on the financial sector.

New Zealand CPI slows in to 6.7% Q1, RBNZ may conclude rate hike cycle soon

In Q1, New Zealand CPI growth slowed down from prior quarter’s 7.2% yoy, registering a 6.7% yoy increase, falling short of the expected 7.0% yoy. The largest contributor to the annual inflation rate was the food sector, followed by housing and household utilities.

On a quarterly basis, CPI rose by 1.2% qoq in Q1, below the anticipated 1.5% qoq increase, marking the lowest result in two years. Vegetables and fruit were the primary drivers of food prices, rising by 8.6% and 11%, respectively.

These figures came in lower than RBNZ’s forecast of a 1.8% qoq and 7.3% yoy inflation. Despite the slowdown in inflation, another 25bps rate hike is still anticipated in May due to the persistently high inflation levels. However, it appears increasingly likely that the upcoming rate hike will be the last in the current cycle.

Australia NAB quarter business conditions resilient, but confidence clearly negative

Australia NAB Quarterly Business Confidence dropped from -1 to -4 in Q1. Current Business Conditions fell from 20 to 16. Business Conditions for the next three months decreased from 22 to 19. But Business Conditions for the next 12 months rose from 18 to 20.

“Consistent with our monthly business survey, today’s release confirms business conditions remained resilient through the first quarter of 2023 at levels well above average,” said NAB Chief Economist Alan Oster. “This strength remains broad based and leading indicators are also holding up, although business confidence is now clearly negative.”

Japan sees 25th consecutive month of export growth, record trade deficit in fiscal 2022

In March, Japan’s exports rose 4.3% yoy to JPY 8824B, above expectation of 2.6% yoy. This marks the 25th consecutive month of growth, primarily driven by auto shipments to the United States.

By region, exports to the US increased by 9.4% yoy in March, slowing down from prior month’s 14.9% yoy growth. On the other hand, exports to China, Japan’s largest trading partner, declined by -7.7% yoy marking the fourth consecutive month of decline.

Imports rose 7.3% yoy to JPY 9579B, below expectation of 11.4% yoy. Consequently, Japan registered a trade deficit of JPY -755 billion.

In fiscal 2022 ended March, Japan recorded a record trade deficit of JPY -21.73T, surpassing prior record of JPY -13.76T registered in fiscal 2013. Imports rose 32.2% to JPY 120.95T while exports rose 15.5% to JPY 99.23T.

Looking ahead

Germany PPI and ECB meeting accounts are the main features. Later in the day, US jobless claims, existing home sales and Philly Fed survey will be released.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6689; (P) 0.6715; (R1) 0.6740; More…

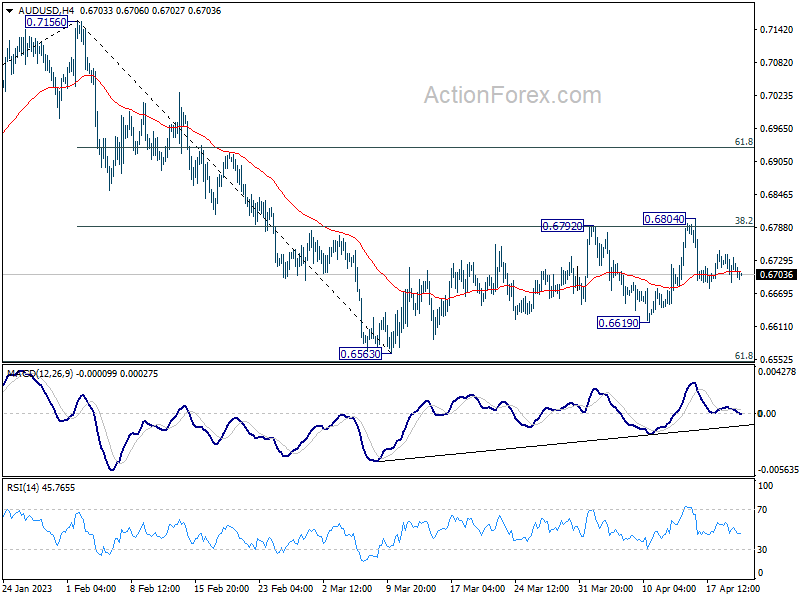

AUD/USD dips mildly today but stays in range of 0.6619/6804. Intraday bias remains neutral at this point. On the downside, break of 0.6619 will indicate that decline from 0.7156 is resuming through 0.6563 low. Nevertheless, sustained break of 0.6804 will bring stronger rally back to 61.8% retracement of 0.7156 to 0.6563 at 0.6929.

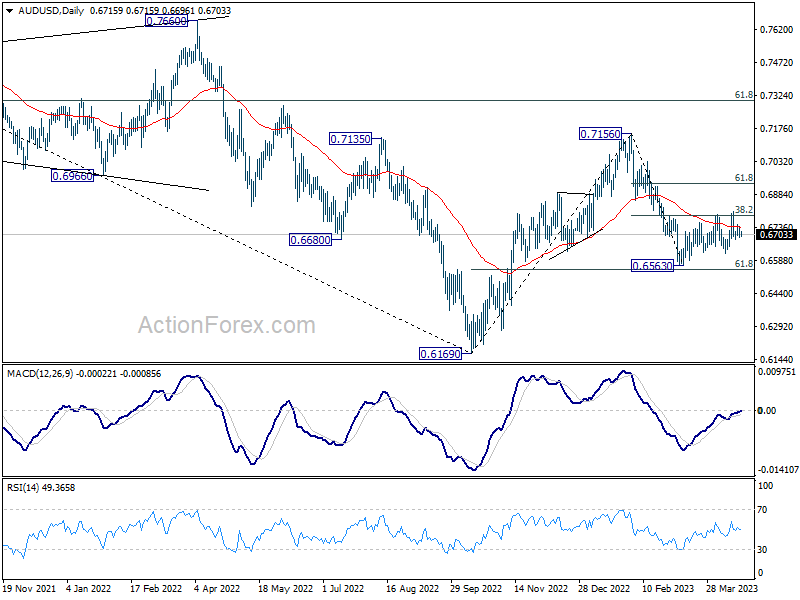

In the bigger picture, as long as 61.8% retracement of 0.6169 to 0.7156 at 0.6546 holds, the decline from 0.7156 is seen as a correction to rally from 0.6169 (2022 low) only. Another rise should still be seen through 0.7156 at a later stage. However, sustained break of 0.6546 will raise the chance of long term down trend resumption through 0.6169 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q1 | 1.20% | 1.50% | 1.40% | |

| 22:45 | NZD | CPI Y/Y Q1 | 6.70% | 7.00% | 7.20% | |

| 23:50 | JPY | Trade Balance (JPY) Mar | -1.21T | -1.78T | -1.19T | -1.25T |

| 01:30 | AUD | NAB Business Confidence Q1 | -4 | -1 | ||

| 04:30 | JPY | Tertiary Industry Index M/M Feb | 0.70% | 0.40% | 0.90% | 0.70% |

| 06:00 | EUR | Germany PPI M/M Mar | -0.50% | -0.30% | ||

| 06:00 | EUR | Germany PPI Y/Y Mar | 9.80% | 15.80% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | USD | Initial Jobless Claims (Apr 14) | 238K | 239K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Apr | -19.1 | -23.2 | ||

| 14:00 | USD | Existing Home Sales Mar | 4.50M | 4.58M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Apr P | -18 | -19 | ||

| 14:30 | USD | Natural Gas Storage | 69B | 25B |