{kind=link}

As European treasury yields rebound, the Euro and Sterling gains against Dollar and Swiss Franc today. However, their upside remains limited by near term resistance. Also, momentum against commodity currencies appears less pronounced. The greenback is trading lower amid generally stabilizing risk sentiment, but market fluctuations remain limited, with European indexes and US futures fluctuating in a tight range between gains and losses.

Commodity currencies are holding their ground alongside the Yen, with traders likely awaiting the release of key economic data, such as US consumer confidence report, to make more significant moves. However, the most significant market impact is expected on Friday with the release of critical data, including Eurozone CPI and US PCE inflation.

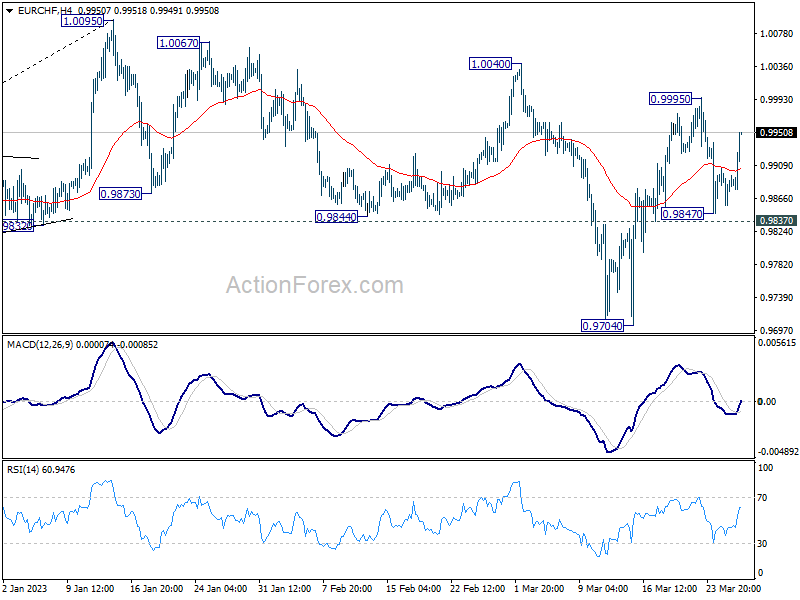

Technically, EUR/CHF is worth a watch for the week. The corrective retreat from 0.9995 might have completed after defending 0.9837. Break of 0.9995 will resume the whole rise form 0.9704. More importantly, that would reaffirm the case that correction from 1.0095 has completed at 0.9704. Larger up trend from could be from 0.9407 could be ready to resume through 1.0095 in this case.

In Europe, at the time of writing, FTSE is down -0.02%. DAX is down -0.08%. CAC is down -0.09%. Germany 10-year yield is up 0.053 at 2.283. Earlier in Asia, Nikkei rose 0.15%. Hong Kong HSI rose 1.1%. China Shanghai SSE dropped -0.19%. Singapore Strait Times rose 0.51%. Japan 10-year JGB yield rose 0.0197 to 0.314.

US goods exports rose 5.5% yoy in Feb, imports dropped -1.9% yoy

In February, US goods exports rose 5.5% yoy to USD 167.8B. Goods imports dropped -1.9% yoy to USD 259.5B. Trade deficit widened slightly to USD -91.6B.

Whole sales inventories rose 0.2% mom to USD 920.3B. Retail inventories rose 0.8% mom to USD 747.3B.

BoE officials address credit conditions and interest rates amid market turmoil

BoE Governor Andrew Bailey acknowledged the existence of “some evidence of some tightening credit conditions” during today’s parliamentary hearing, addressing concerns surrounding the current financial market turmoil. Despite the tightening, Bailey remains optimistic, stating that “we do not see a critical development in that respect.”

The Governor emphasized that the BoE always considers credit conditions when setting monetary policy and expressed confidence in the bank’s ability to assess the impact of raising interest rates on the position of the banks themselves.

Deputy Governor Dave Ramsden shared similar sentiments, acknowledging the importance of vigilance regarding the risks higher interest rates might pose to other parts of the economy. He added that the current environment is “volatile and challenging,” highlighting the need for careful monitoring and assessment by central bank officials to ensure financial stability and well-informed policy decisions.

Australia retail sales turnover up 0.2% mom in Feb, appeared to have levelled out

Australia retail sales turnover rose 0.2% mom to AUD 35.14B in February, matched expectations. Through the year, retail sales rose 6.4% yoy.

Ben Dorber, ABS head of retail statistics, said retail sales rose modestly in February and appear to have levelled out after a period of increased volatility over November, December and January.

“On average, retail spending has been flat through the end of 2022 and to begin the new year.”

Retail turnover rose modestly across most of the states and territories, with rises at 1.0% or less. Queensland recorded the only fall in turnover, down -0.4%.

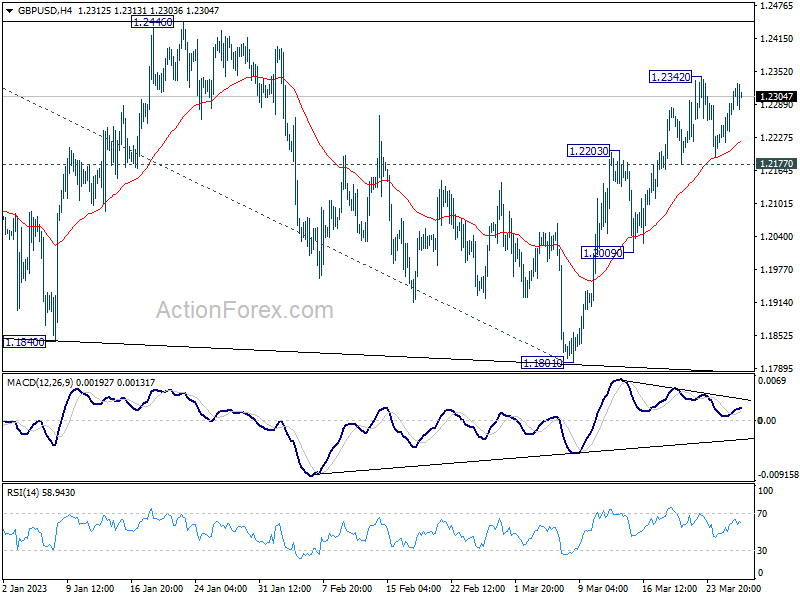

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2240; (P) 1.2267; (R1) 1.2314; More…

GBPUSD is still bounded in range below 1.2342 and intraday bias stays neutral first. With 1.2177 minor support intact, further rally is expected. On the upside, break of 1.2342 will target 1.2445/6 resistance zone. Firm break there will resume larger rally from 1.0351, and target 1.2759 fibonacci level. On the downside, however, break of 1.2177 minor support will argue that corrective pattern from 1.2445 is extending with another falling leg, and turn bias to the downside for 1.2009 support instead.

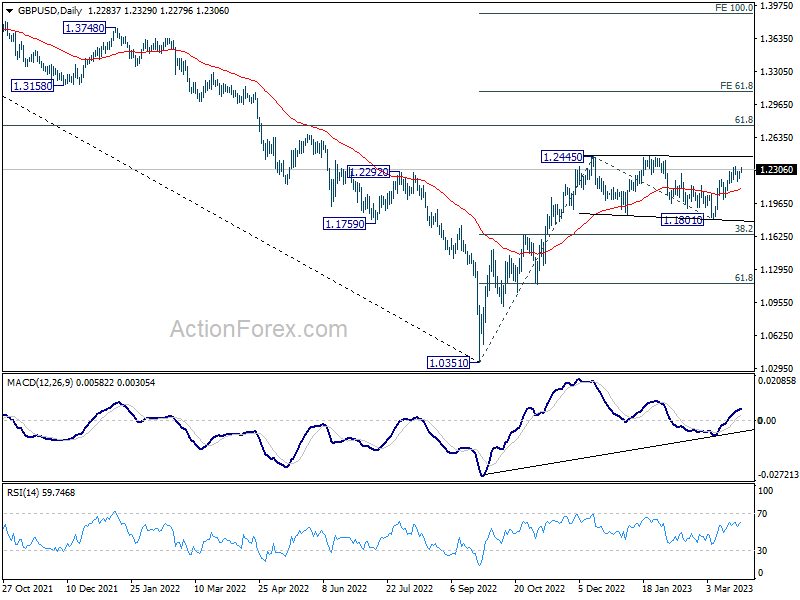

In the bigger picture, price action from 1.2445 are seen as a corrective pattern to rise from 1.0351 medium term bottom (2022 low). Resumption of the rally from 1.0351 is expected and break of 1.2446 will target 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. This will remain the favored case as long as 38.2% retracement of 1.0351 to 1.2445 at 1.1645 holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Feb | 0.20% | 0.40% | 1.90% | 1.80% |

| 11:00 | GBP | BoE Quarterly Bulletin | ||||

| 12:30 | USD | Goods Trade Balance (USD) Feb P | -91.6B | -91.5B | -91.1B | |

| 12:30 | USD | Wholesale Inventories Feb P | 0.20% | 0.20% | -0.40% | -0.50% |

| 13:00 | USD | Housing Price Index M/M Jan | 0.20% | -0.20% | -0.10% | |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jan | 2.50% | 4.50% | 4.60% | |

| 14:00 | USD | Consumer Confidence Mar | 101.7 | 102.9 |