{kind=link}

Dollar weakened slightly in early US session, following the release of economic data which showed that consumer inflation slowed in February to the level as expected. The absence of an upside surprise in the CPI readings means that Fed should be in a more comfortable position to address uncertainties over the banking system. This could make a 50bps rate hike look much less necessary to policymakers, while the markets have already priced it out. US futures rose after the release, indicating a potential rebound. However, Treasury yields remained steady.

In the currency markets, Canadian Dollar is the strongest performer today so far, followed by New Zealand and Australian Dollars. Yen was the worst performer, reversing all gains made against all currencies except the greenback. Euro and Dollar were the next weakest performers. Euro, in particular, is lacking some firepower as the markets question whether ECB will deliver on its promise of a 50 basis points rate hike this Thursday.

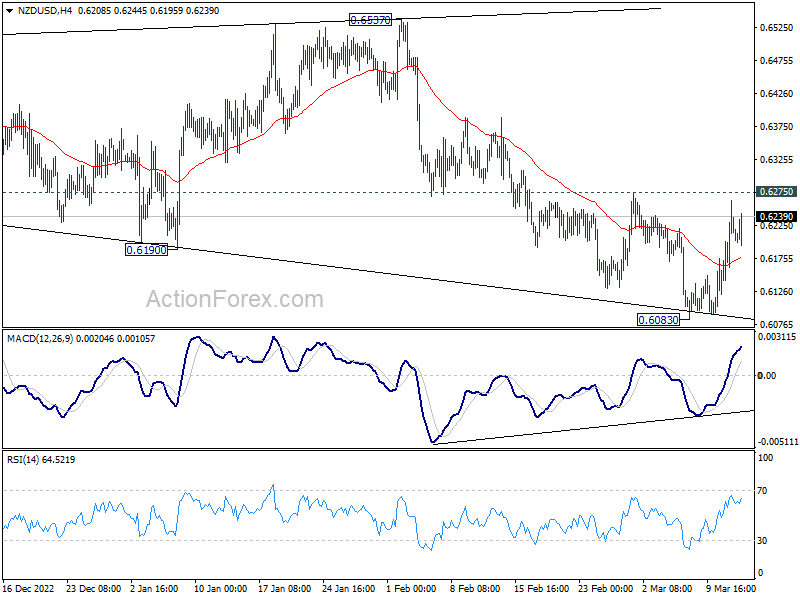

Technically, a major focus is still on whether Dollar would break through near term support levels against commodity currencies, to alight with the near term bearish outlook against others. The levels to watch include 0.6694 resistance in AUD/USD, 0.6725 resistance in NZD/USD, and 1.3664 support in USD/CAD. Decisive break of these levels is need to confirm underlying weakness in Dollar.

In Europe, at the time of writing, FTSE is up 0.55%. DAX is up 1.63%. CAC is up 1.42%. Germany 10-year yield is up 0.1451 at 2.403. Earlier in Asia, Nikkei dropped -2.19%. Hong Kong HSI dropped -2.27%. China Shanghai SSE dropped -0.72%. Singapore Strait Times dropped -0.08%. Japan 10-year JGB yield dropped -0.0226 to 0.283.

US CPI slowed to 6.0% yoy in Feb, core CPI down to 5.5% yoy

US CPI slowed from 6.4% yoy to 6.0% yoy in February, matched expectations. That’s also the lowest reading since September 2021. Core CPI (all items less food and energy) slowed slightly from 5.6% yoy to 5.5% yoy, matched expectations, and was the lowest since December 2021. Energy index rose 5.2% yoy while food index rose 9.5% yoy.

For the month, CPI rose 0.4% mom while core CPI rose 0.5% mom. Food index rose 0.4% mom and energy index decreased 0.6% mom.

UK payrolled employment rose 98k in Feb, unemployment rate unchanged at 3.7% in Jan

In February, UK payrolled employment rose 98k or 0.3% mom. Comparing to the same month a year ago, payrolled employment rose 1040k or 3.6% yoy. Median monthly pay rose 6.7% yoy. Claimant count dropped -11.2k versus expectation of -12.4k.

In the three month to January, unemployment rate was unchanged at 3.7%, better than expectation of a rise to 3.8%. Average earnings excluding bonus rose 6.5%, below expectation of 6.6%. Average earnings including bonus rose 5.7%, matched expectations.

Australia Westpac consumer sentiment unchanged at 78.5, second sub-80 read in a row

Australia Westpac Consumer Sentiment Index was unchanged at 78.5 in March, a second month of extremely weak reading, near historical lows. Areas of most concern remain inflation, interest rates, and the economy.

Westpac noted that there were only one month of sub-80 reading during the COVID pandemic and the global financial crisis period. Runs of sub-80 have only been seen during the recession during the 1980s and 1990s.

Regarding RBA policy, Westpac will wait after release of data on employment, inflation, spending, and confidence, before deciding to change the expectation of a 25bps hike in April. But Westpac maintained the forecast of another 25bps hike in May.

Australia NAB business confidence fell to -4, conditions down to 17

Australia NAB Business Confidence dropped sharply from 6 to -4 in February. Business Conditions dropped from 18 to 17. Looking at some details, trading conditions were unchanged at 27. Profitability conditions dropped from 18 to 14. Employment conditions rose from 11 to 12.

“Overall, the survey confirms the ongoing resilience of the economy through the first months of 2023, though we continue to expect a more material slowdown in demand later in the year when the full effect of rate rises has passed through,” said NAB.

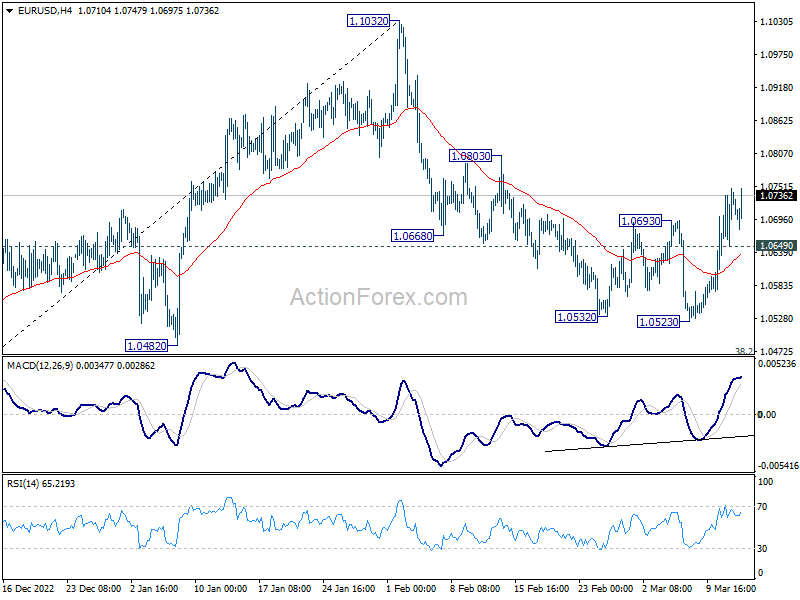

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0672; (P) 1.0710; (R1) 1.0771; More…

EUR/USD’s rally from 1.0523 is still in progress and intraday bias stays on the upside. As noted before, corrective decline from 1.1032 should have completed at 1.5023, ahead of 1.0482 key support. Break of 1.0803 resistance will bring retest of 1.1032 high next. On the downside, below 1.0649 minor support will turn intraday bias neutral. But risk will stay on the upside as long as 1.0523 support holds, in case of retreat.

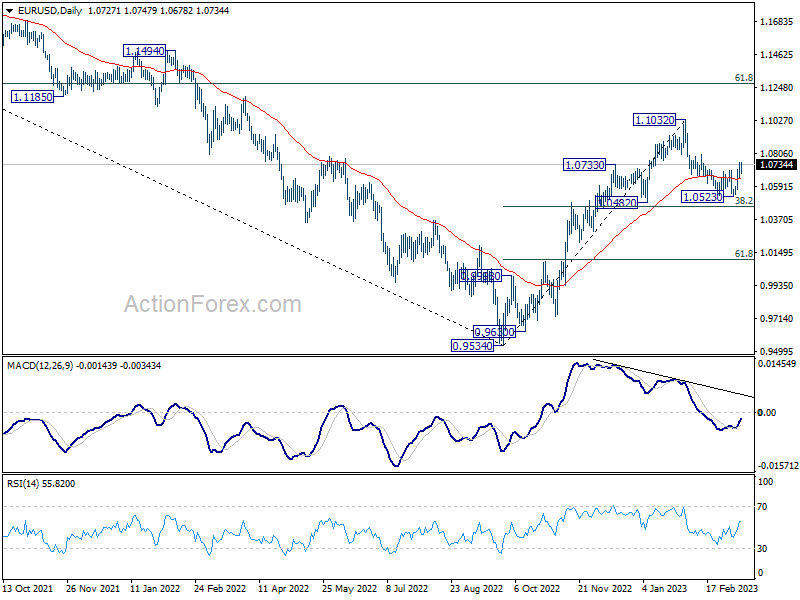

In the bigger picture, as long as 1.0482 support holds, rise from 0.9534 (2022 low) should continue to 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. However, sustained break of 1.0482 will bring deeper fall to 61.8% retracement of 0.9534 to 1.1032 at 1.0106, even as a corrective pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Mar | 0.00% | -6.90% | ||

| 00:30 | AUD | NAB Business Conditions Feb | 17 | 18 | ||

| 00:30 | AUD | NAB Business Confidence Feb | -4 | 6 | ||

| 07:00 | GBP | Claimant Count Change Feb | -11.2K | -12.4K | -12.9K | -30.3K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Jan | 3.70% | 3.80% | 3.70% | |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jan | 6.50% | 6.60% | 6.70% | |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Jan | 5.70% | 5.70% | 5.90% | 6.00% |

| 07:30 | CHF | Producer and Import Prices M/M Feb | -0.20% | 0.50% | 0.70% | |

| 07:30 | CHF | Producer and Import Prices Y/Y Feb | 2.70% | 3.40% | 3.30% | |

| 09:00 | EUR | Italy Industrial Output M/M Jan | -0.70% | -0.40% | 1.60% | 1.20% |

| 11:00 | USD | NFIB Business Optimism Index Feb | 90.9 | 91.2 | 90.3 | |

| 12:30 | CAD | Manufacturing Sales M/M Jan | 4.10% | -0.40% | -1.50% | -2.10% |

| 12:30 | USD | CPI M/M Feb | 0.40% | 0.40% | 0.50% | |

| 12:30 | USD | CPI Y/Y Feb | 6.00% | 6.00% | 6.40% | |

| 12:30 | USD | CPI Core M/M Feb | 0.50% | 0.40% | 0.40% | |

| 12:30 | USD | CPI Core Y/Y Feb | 5.50% | 5.50% | 5.60% |