{kind=link}

While Dollar remains generally firm, Yen is reversing much of this week’s gain. The moves come as European benchmark yields are trading generally higher. Major European stock indexes are also in slight positive position. Canadian Dollar is rebounding, responding more to rising core inflation reading. European majors and other commodity currencies are mixed for now.

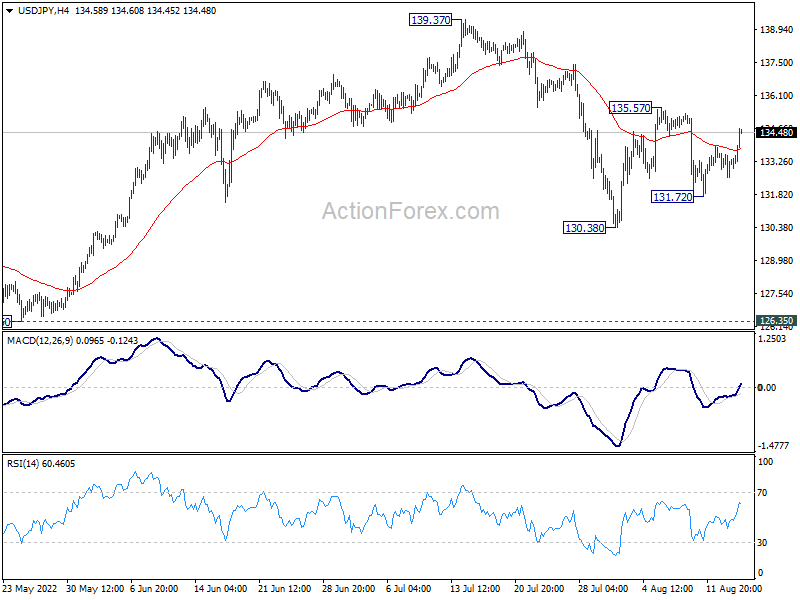

Technically, one focus is on whether USD/JPY would break through 135.57 minor resistance to resume the rebound from 130.38. If happens, such move could be accompanied by break of 138.38 minor resistance in EUR/JPY and 163.91 minor resistance in GBP/JPY. Such development might come in tandem with stronger rally in US stocks and benchmark yields.

In Europe, at the time of writing, FTSE is up 0.56%. DAX is up 0.15%. CAC is up 0.06%. Germany 10-year yield is up 0.060 at 0.960. Earlier in Asia, Nikkei dropped -0.01%. Hong Kong HSI dropped -1.05%. China Shanghai SSE rose 0.05%. Singapore Strait Times dropped -0.09%. Japan 10-year JGB yield dropped -0.0168 to 0.170.

Canada CPI slowed to 7.6% yoy in Jul, as gasoline prices fell

Canada CPI slowed from 8.1% yoy to 7.6% yoy in July, matched expectations. Excluding gasoline, prices accelerated from 6.5% yoy to 6.6% yoy. Gasoline prices slowed sharply from 54.6% yoy to 35.6% yoy.

For the month, CPI rose 0.1% mom, lowest since December. Gasoline prices dropped -9.2% mom, largest monthly decline since April 2020.

CPI common rose from 4.6% yoy to 5.5% yoy, above expectation of 4.7% yoy. CPI median rose from 4.9% yoy to 5.0% yoy, above expectation of 4.9% yoy. CPI trimmed slowed from 5.5% yoy to 5.4% yoy, matched expectations.

Germany ZEW dropped to -55.3, further decline in already weak economic growth

Germany ZEW Economic Sentiment dropped slightly from -53.8 to -55.3 in August, below expectation of -52.7. Current Situation index dropped from -45.8 to -47.6, above expectation of -48.0.

Eurozone ZEW Economic Sentiment dropped from -51.1 to -54.9, below expectation of -52.0. Current Situation Index rose 2.5 pts to -42.0. Eurozone inflation expectations rose 2.1 pts to -23.5, indicating a reduction of the high inflation rates within the next six months.

“The ZEW Economic Expectations decrease again slightly in August after a sharp drop in the previous month. The financial market experts therefore expect a further decline in the already weak economic growth in Germany. The still high inflation rates and the expected additional costs for heating and energy lead to a decrease in profit expectations for the private consumption sector. In contrast, the expectations for the financial sector are improving due to the supposed further increase in short-term interest rates”, comments Michael Schröder, researcher at ZEW and head of the ZEW financial market survey, on current results.

Eurozone exports rose 20.1% yoy in Jun, imports rose 43.5% yoy

Eurozone exports of goods to the rest of the world rose 20.1% yoy to EUR 252.2B in June. Imports rose 43.5% yoy to EUR 276.8B. Trade balance came in at EUR -24.6B deficit. Intra-eurozone trade rose 24.2% yoy to EUR 236.4B.

In seasonally adjusted term, exports dropped -0.1% mom to EUR 241.8B. Imports rose 1.3% mom to EUR 272.7B. Trade deficit widened from EUR -27.2B to EUR -30.8B, versus expectation of EUR -20.0B. Intra-eurozone trade was unchanged at EUR 224.1B.

UK payrolled employment rose 73k in Jul, unemployment rate unchanged at 3.8% in Jun

UK payrolled employment increased by 73k, or 0.2% mom, in July. Comparing with the same month a year ago, payrolled employees rose 29.7m, or 2.9% yoy. Claimant count dropped -10.5k, smaller than expectation of -32.9k. Median monthly pay rose 6.6% yoy to GBP 2108.

In the three months to June, unemployment rate was unchanged at 3.8%, matched expectations. Average earnings excluding bonus rose 4.7% 3moy, above expectation of 4.4%. Average earnings including bonus rose 5.1% 3moy, below expectation of 5.2%.

RBA Minutes: Further monetary policy normalization expected

In the minutes of the August 2 meeting, RBA expects to “take further steps in the process of normalizing monetary conditions over the months ahead”. However, it is “not on a pre-set path.” The path is a “narrow one” and “subject to considerable uncertainty”. The size of timing of future rate hikes will be guided by incoming data and the assessment of the outlook for inflation and labor market, including the risks.

RBA said that inflation is expected to “peak later in 2022”, then decline to top of 2-3% target range by the end of 2024. The expected moderation reflected “the ongoing resolution of global supply-side problems, the stabilization of commodity prices and the impact of rising interest rates in Australia and overseas”. Medium-term inflation expectation remained “well anchored”.

The Australian economy was “growing strongly” with resilient consumer spending and positive investment outlook. National income was boosted by rise in terms of trade to record high”. Outlook is expected to “remain strong” for the rest of 2022, then slow in 2023 and 2024. Employment was “growing strongly” and further declines in unemployment rate were expected over the months ahead.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 132.71; (P) 133.16; (R1) 133.75; More…

Intraday bias in USD/JPY remains neutral at this point. Overall, corrective pattern from 139.37 will extend further. On the upside, above 135.57 will resume the rebound to retest 139.37 high. On the downside, below 131.72 will resume the fall from 139.37 through 130.38 support.

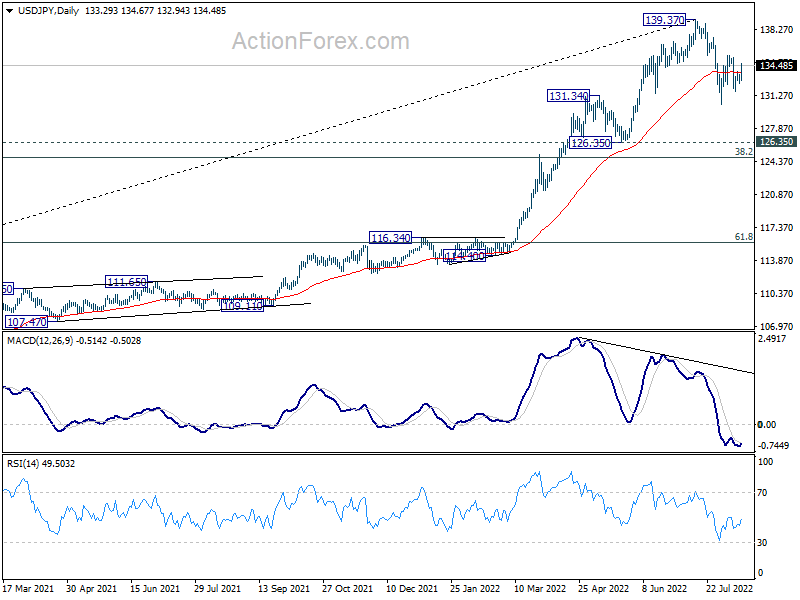

In the bigger picture, fall from 139.37 medium term top is seen as correcting whole up trend from 101.18 (2020 low). While deeper decline cannot be ruled out, outlook will stays bullish as long as 55 week EMA (now at 122.70) holds. Long term up trend is expected to resume through 139.37 at a later stage, after the correction finishes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 04:30 | JPY | Tertiary Industry Index M/M Jun | -0.20% | 0.50% | 0.80% | 1.10% |

| 06:00 | GBP | Claimant Count Change Jul | -10.5K | -32.0K | -20.0K | -26.8K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Jun | 3.80% | 3.80% | 3.80% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jun | 4.70% | 4.40% | 4.30% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jun | 5.10% | 5.20% | 6.20% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jun | -30.8B | -20.0B | -26.0B | -27.2B |

| 09:00 | EUR | Germany ZEW Economic Sentiment Aug | -55.3 | -52.7 | -53.8 | |

| 09:00 | EUR | Germany ZEW Current Situation Aug | -47.6 | -48 | -45.8 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Aug | -54.9 | -52 | -51.1 | |

| 12:15 | CAD | Housing Starts Jul | 275K | 265K | 274K | 272K |

| 12:30 | CAD | CPI M/M Jul | 0.10% | 0.10% | 0.70% | |

| 12:30 | CAD | CPI Y/Y Jul | 7.60% | 7.60% | 8.10% | |

| 12:30 | CAD | CPI Common Y/Y Jul | 5.50% | 4.70% | 4.60% | |

| 12:30 | CAD | CPI Median Y/Y Jul | 5.00% | 4.90% | 4.90% | |

| 12:30 | CAD | CPI Trimmed Y/Y Jul | 5.40% | 5.40% | 5.50% | |

| 12:30 | USD | Building Permits Jul | 1.67M | 1.65M | 1.70M | |

| 12:30 | USD | Housing Starts Jul | 1.45M | 1.35M | 1.56M | |

| 13:15 | USD | Industrial Production M/M Jul | 0.20% | -0.20% | ||

| 13:15 | USD | Capacity Utilization Jul | 80.10% | 80.00% |