{kind=link}

The stock markets are starting to display some resilience, despite hawkish FOMC minutes. US stocks managed to close higher after initial selloff. Nikkei is also showing some strength in Asian session. Dollar and Yen are retreating mildly while Aussie and Kiwi are trading higher. As for the week, Euro and Sterling remain the runaway loser, followed by Canadian. On the other hand, Aussie has overtaken the first place, followed by Dollar and then Yen.

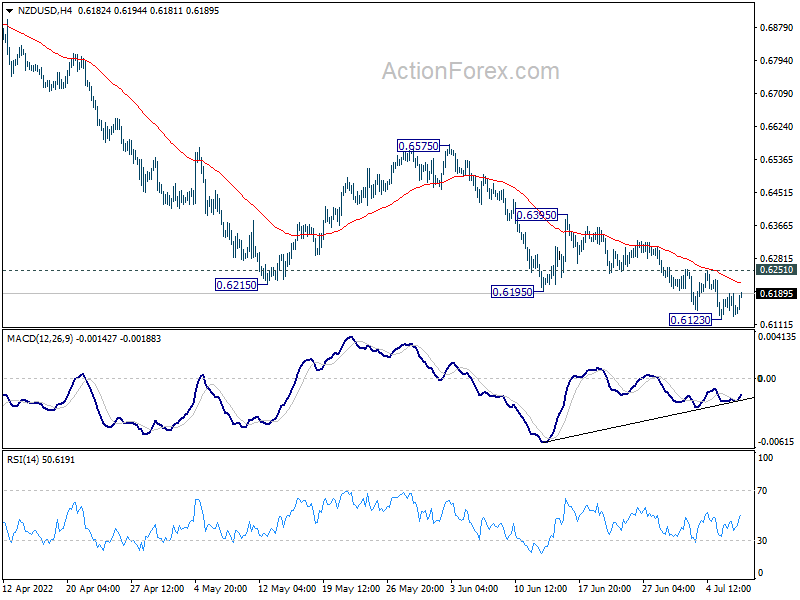

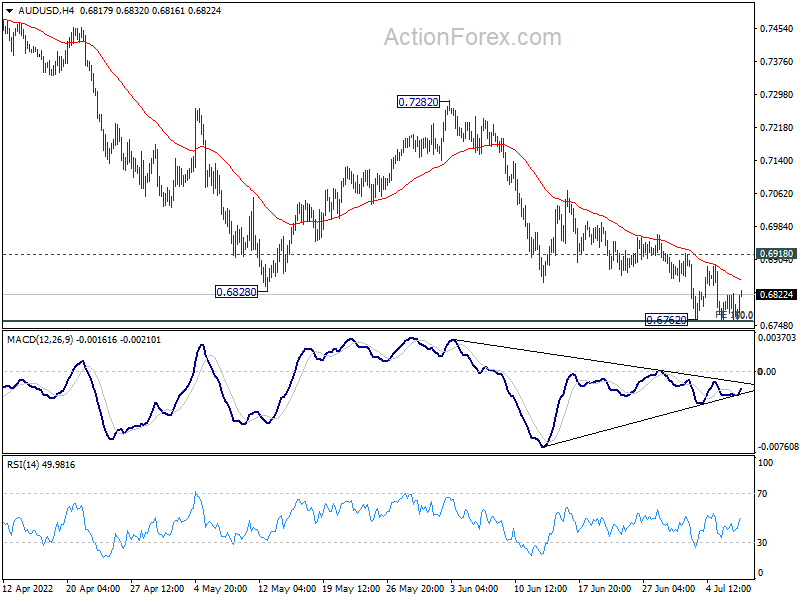

Technically, as Aussie and Kiwi are displaying some resilience, focuses will be on AUD/USD and NZD/USD. Though, the more decisive moves could only come after tomorrow’s non-farm payrolls. Anyway, AUD/USD is still defending 0.6756/60 cluster support. Break of 0.6918 minor resistance will suggest short term bottoming and raise the chance of bullish reversal. Similarly, break of 0.6251 minor resistance in NZD/USD should also bring rebound to 0.6395 resistance and possibly above.

In Asia, at the time of writing, Nikkei is trading up 1.33%. Hong Kong HSI is down -0.17%. China Shanghai SSE is up 0.50%. Singapore Strait Times is up 0.15%. Japan 10-year JGB yield is down -0.0044 at 0.245. Overnight, DOW rose 0.23%. S&P 500 rose 0.36%. NASDAQ rose 0.35%. 10-year yield rose 0.104 to 2.913.

Fed minutes: As even more restrictive stance could be appropriate

In the minutes of the June 14–15 FOMC meeting, Fed noted, “participants concurred that the economic outlook warranted moving to a restrictive stance of policy, and they recognized the possibility that an even more restrictive stance could be appropriate if elevated inflation pressures were to persist.”

Also, “participants recognized that policy firming could slow the pace of economic growth for a time, but they saw the return of inflation to 2 percent as critical to achieving maximum employment on a sustained basis.”

“Many participants judged that a significant risk now facing the Committee was that elevated inflation could become entrenched if the public began to question the resolve of the Committee to adjust the stance of policy as warranted,” the minutes noted.

Australia AiG services dropped to 48.8, two-speed pattern to gather pace

Australia AiG Performance of Services Index dropped -0.4 to 48.8 in June. Looking at some details, sales plummeted by -8.8 to 41.9. Employment surged 7.9 to 55.3. New orders ticked down by -0.8 to 58.9. Input prices rose 0.3 to 69.0. Selling prices rose 5.3 to 67.2. Averages jumped 10.3 to 67.7.

Innes Willox, Chief Executive Ai Group, said: “With interest rates rising for the first time in a decade, we have seen a ‘two-speed’ services sector emerge in June. Industries which are sensitive to sentiment changes – such as business & property, and personal & recreational services – declined into contraction. Less interest-rate-exposed services remained in a growth phase. With the RBA increasing rates by 50 basis points again this week, we would expect this two-speed pattern to gather pace.”

Also from Australia, goods and services exports rose 9.5% mom to AUD 58.4B in May. Goods and services imports rose 5.8% mom to AUD 42.4B. Trade surplus widened from AUD 13.2B to AUD 16.0B.

Looking ahead

Swiss unemployment rate and foreign currency reserves, Germany industrial production will be released in European session. But ECB meeting accounts could catch most attention.

Later in the day, US will release ADP jobs, jobless claims and trade balance. Canada will also release trade balance.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6753; (P) 0.6790; (R1) 0.6817; More…

Intraday bias in AUD/USD is staying neutral at this point. Strong support could still be seen from 0.6756/60 cluster support to complete the whole correction from 0.8006, and bring rebound. On the upside, above 0.6918 resistance will indicate short term bottoming, and turn bias back to the upside for 0.7282 resistance. However, sustained break of 0.6756/60 will carry larger bearish implication and target 0.6461 fibonacci level next.

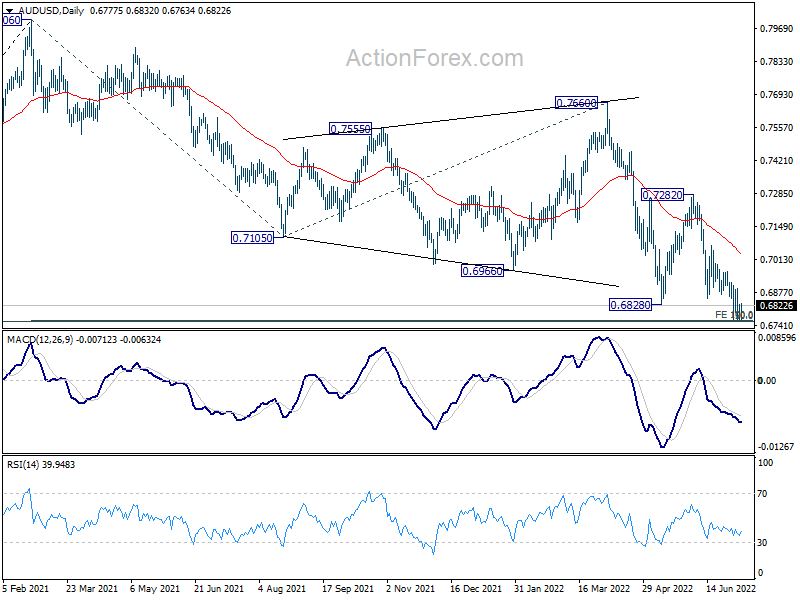

In the bigger picture, price actions from 0.8006 are seen as a corrective pattern to rise from 0.5506 (2020 low). Strong support is expected from 50% retracement of 0.5506 to 0.8006 at 0.6756 to complete the pattern. This coincides with 100% projection of 0.8006 to 0.7105 from 0.7660 at 0.6760. However firm break of 0.6756/60 will raise the chance of bearish reversal and target 61.8% retracement at 0.6461.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index Jun | 48.8 | 49.2 | ||

| 01:30 | AUD | Trade Balance (AUD) May | 15.97B | 10.90B | 10.50B | 13.25B |

| 05:00 | JPY | Leading Economic Index May P | 101.40% | 101.60% | 102.90% | |

| 05:45 | CHF | Unemployment Rate Jun | 2.20% | 2.20% | ||

| 06:00 | EUR | Germany Industrial Production M/M May | 0.40% | 0.70% | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jun | 925B | |||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:15 | USD | ADP Employment Change Jun | 200K | 128K | ||

| 12:30 | USD | Initial Jobless Claims (Jul 1) | 230K | 231K | ||

| 12:30 | USD | Goods and Services Trade Balance (USD) May | -85.0B | -87.1B | ||

| 12:30 | CAD | International Merchandise Trade (CAD) May | 2.5B | 1.5B | ||

| 14:00 | CAD | Ivey PMI Jun | 74 | 72 | ||

| 14:30 | USD | Natural Gas Storage | 82B | |||

| 15:00 | USD | Crude Oil Inventories | -2.8M |