{kind=link}

Trading in the currency market is rather quiet today, with major pairs and crosses stuck inside yesterday’s range. Other markets are also treading water with European indexes and US futures slightly up. Benchmark treasury yields are mixed. Gold is retreating slightly while oil prices are also range bound. As for the week, Dollar remains the worst performing one, followed by Canadian and Aussie. Swiss Franc is the strongest, followed by Euro and Kiwi.

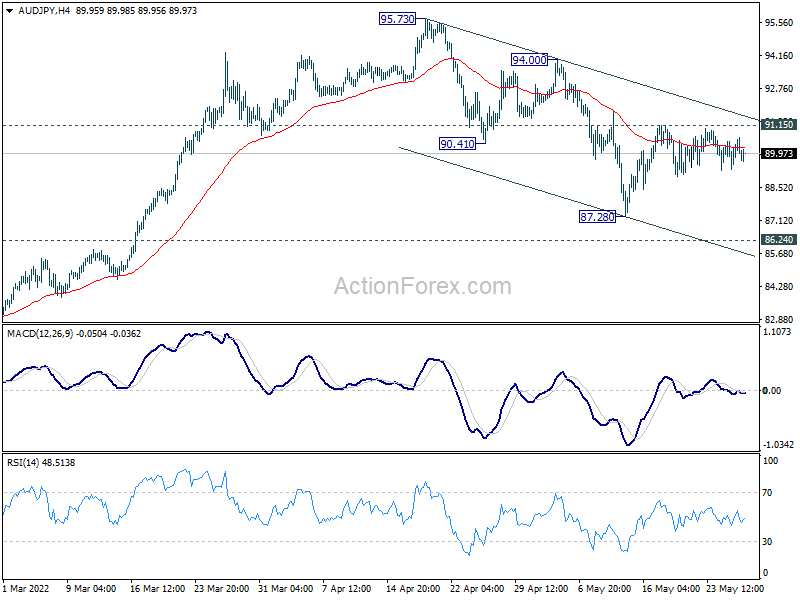

Technically, US stocks have been very resilient this week, but there is no clear turn around in the near term trend yet. If overall sentiment does improve further, it’s likely that AUD/JPY would finally break through 91.15 resistance to resume the rebound from 87.28 low. Such development, if happens, would also firm the case that correction from 95.73 is finished, and bring retest of this high. In that case, stock markets should be staging a strong rebound too, or something is wrong underneath.

In Europe, at the time of writing, FTSE is up 0.12%. DAX is up 0.84%. CAC is up 0.78%. Germany 10-year yield is up 0.010 at 0.964. Earlier in Asia, Nikkei dropped -0.27%. Hong Kong HSI dropped -0.27%. China Shanghai SSE rose 0.50%. Singapore Strait Times rose 0.93%. Japan 10-year JGB yield rose 0.0232 to 0.235.

US initial jobless claims dropped to 210k continuing claims down to 1.348m

US initial jobless claims dropped -8k to 210k in the week ending May 21, matched expectations. Four-week moving average of initial claims rose 7k to 207k.

Continuing claims rose 31k to 1346k in the week ending May 14. Four-week moving average of continuing claims dropped -14k to 1348k, lowest since January 17, 1970 when it was 1340k.

Also released, Q1 GDP was revised down from -1.4% annualized to -1.5%. GDP price index was revised up from 8% to 8.1%.

Canada retail sales flat in Mar, auto and parts contracted sharply

Canada retail sales was flat mom in March, worse than expectation of 1.5% mom rise. Sales were up in 10 of 11 subsectors, led by gasoline (up 7.4%). However, sales at motor vehicle and parts dealers (-6.4%) erased the gains observed in the remaining subsectors.

For Q1 as a whole, sales were up 3.0%, largest quarterly rise since Q3 of 2020. Preliminary data indicates sales rose 0.8% mom in April.

BoJ Kuroda: Exit from easy monetary policy won’t be easy

BoJ Governor Haruhiko Kuroda reiterated to the parliament today that ultra-loose monetary policy must be maintained for now. Consumer inflation is still expected to slow next year and beyond, after spiking above 2% target this year, only because of surging energy prices.

Nevertheless, Kuroda also noted when the right time comes, BoJ will plan an exit from easy policy. “The key would be how to raise interest rates and scale back the BOJ’s expanded balance sheet,” he said. “The BOJ can combine various means and ensure markets remain stable in executing a smooth exit from easy policy. I must add, however, that it won’t be easy,” he said.

Regarding exchange rate depreciation, Kuroda said Fed’s rate hike may not necessarily weaken the Yen, if they also shoot down stock prices.

Prime Minister Fumio Kishida said in the same parliament session, “sharp yen moves are undesirable. While a weak yen benefits exports and firms with overseas assets, it hurts households and some businesses via higher costs.”

RBNZ Orr: Single biggest risk is embedded inflation expectation

RBNZ Governor Adrian Orr told a parliamentary committee today, “the single biggest risk to this nation at the moment is enabling current high CPI inflation to become embedded in future ongoing inflation expectation.”

Orr said that a recession is not projected for New Zealand, even though he cannot rule it out. Challenges to growth were coming through significant downgrades to global growth, particularly China.

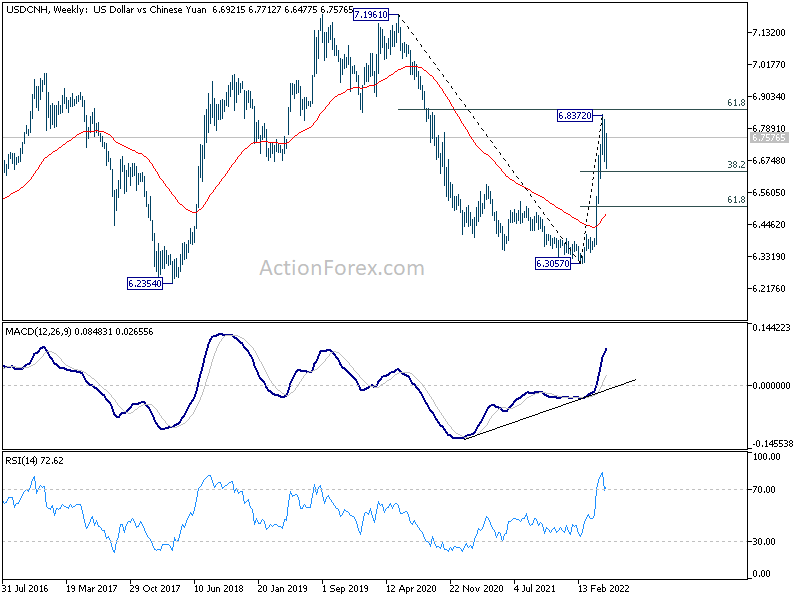

USD/CNH finished pull back, heading back to 6.83

Yuan’s decline today suggests that the near term recovery is already completed and there’s risk of more downside. The selloff came after Chinese Premier Li Keqiang held a rare high-profile meeting yesterday on measures to support the economy. That’s is seen as a sign that the government is in deep worry about the impact of the extend tough pandemic lockdowns in many majors city, including Shanghai.

USD/CNH’s pull back from 6.8372 has likely completed at 0.6477, just ahead of 38.2% retracement of 6.3057 to 6.8372 at 6.6342. Strong rebound should be seen to 6.8372 and possibly above. The key resistance, however, still lies 61.8% retracement of 7.1961 to 6.3057 at 6.8560. USD/CNH could still be rejection by this fibonacci level at the second attempt.

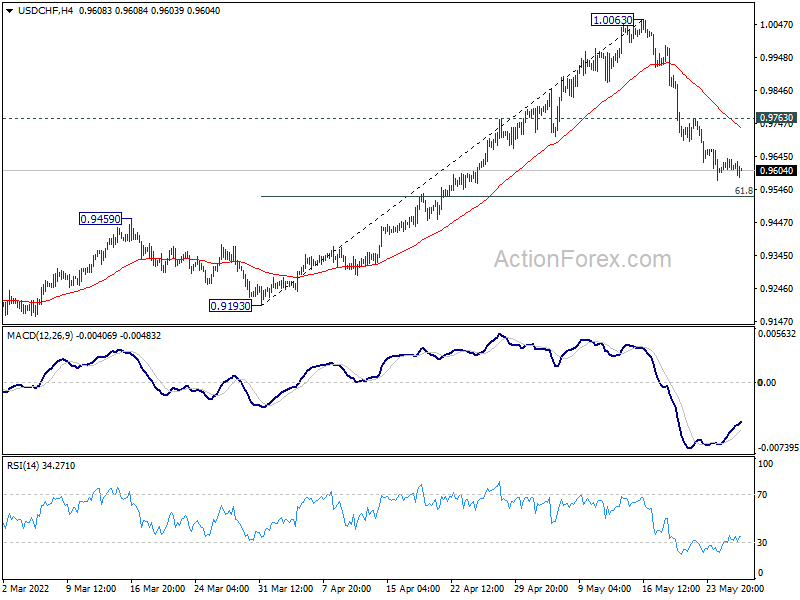

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9599; (P) 0.9621; (R1) 0.9645; More…

USD/CHF’s downside momentum is diminishing as in 4 hour MACD. While further decline cannot be ruled out, downside should be contained by 61.8% retracement of 0.9193 to 1.0063 at 0.9525 to bring rebound. On the upside, above 0.9763 minor resistance will turn bias back to the upside for recovery. However, sustained break of 0.9525 will bring deeper decline to 0.9459 support.

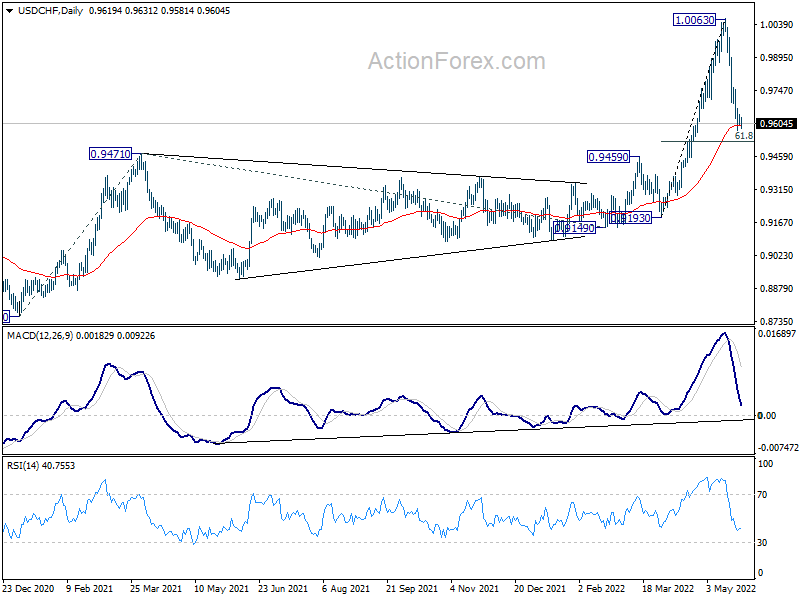

In the bigger picture, down trend from 1.0342 (2016 high) should have completed with three waves down to 0.8756 (2021 low) already. Rise from 0.8756 is likely a medium term up trend of its own. Next target is 161.8% projection of 0.8756 to 0.9471 from 0.9149 at 1.0306, which is close to 1.0342 (2016 high). This will remain the favored case as long as 0.9459 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Apr | 1.70% | 0.90% | 1.30% | |

| 01:30 | AUD | Private Capital Expenditure Q1 | -0.30% | 1.50% | 1.10% | 2.30% |

| 12:30 | CAD | Retail Sales M/M Mar | 0.00% | 1.50% | 0.10% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Mar | 2.40% | 2.20% | 2.10% | |

| 12:30 | USD | Initial Jobless Claims (May 20) | 210K | 210K | 218K | |

| 12:30 | USD | GDP Annualized Q1 P | -1.50% | -1.30% | -1.40% | |

| 12:30 | USD | GDP Price Index Q1 P | 8.10% | 8.00% | 8.00% | |

| 14:00 | USD | Pending Home Sales M/M Apr | -1.70% | -1.20% | ||

| 14:30 | USD | Natural Gas Storage | 83B | 89B |