{kind=link}

The markets are generally quiet in Asian session today. Dollar is mildly firmer together with Canadian. Sterling and Swiss Franc are soft. But major pairs and crosses are stuck inside Friday’s range. Asian stocks are mixed, with Japan on Holiday, while others tread water. Gold is consolidating in tight range too. Crude oil is the more lively one, extending near term rebound. Markets could stay quiet with a very light calendar today. But volatility is expected with some important data featured later in the week.

Technically, Euro has turned weaker late last week against commodity currencies. The question is whether such weakness would spread to other pairs. Attention will be on 1.0899 minor support in EUR/USD, 0.8358 minor support in EUR/GBP, and 1.0184 minor support in EUR/CHF. Break of these levels together will signal return of Euro selloff.

In Asia, at the time of writing, Hong Kong HSI is down -0.08%. China Shanghai SSE is up 0.02%. Singapore Strait Times is up 0.18%. Japan is on holiday.

New Zealand goods export rose 22% yoy in Feb, imports rose 37% yoy

New Zealand goods exports rose 22% yoy to NZD 5.5B in February. Goods imports rose 37% yoy to NZD 5.9B. Trade deficit came in at NZD -385m, smaller than expectation of NZD -808m.

Exports to all top destinations increased, including China (up NZD 80m or 5.4%), Australia (up NZD 119m or 22.0%), US (up NZD 37m or 7.4%), EU (up NZD 62m or 25%), and Japan (up NZD 71m or 34%).

Imports from all top partners also rose, including China (up NZD 490m or 45%), EUR (up NZD 209m or 32%), Australia (up NZD 137m or 26%), US (up NZD 105m or 29%), and Japan (up NZD 167m or 60%).

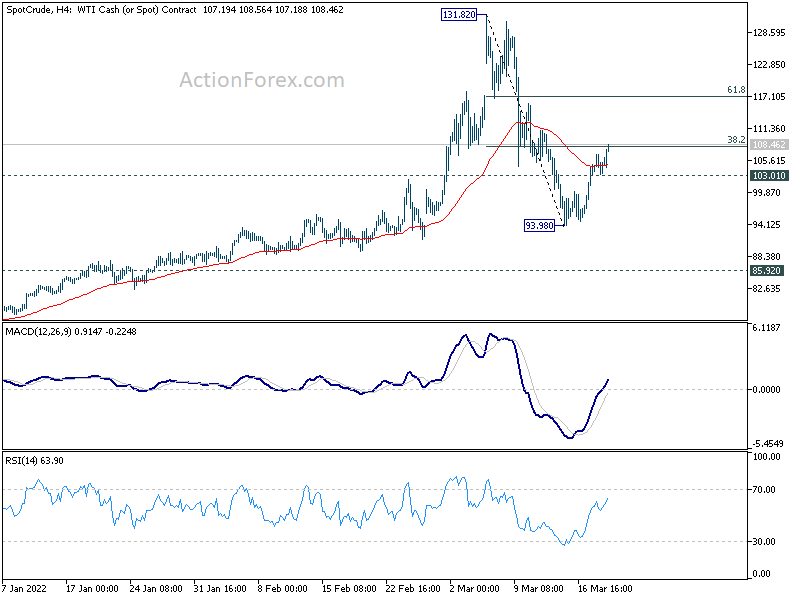

WTI crude oil extending rebound, pressing 108 fib level

WTI crude oil is extends the near term rebound and is back above 108. It’s reported that OPEC+ missed its production target by slightly more than 1m barrels per day in February. At the same time, some Baltic countries are pushing EU for an oil embargo on Russia for its invasion of Ukraine.

WTI is now pressing 38.2% retracement of 131.82 to 93.98 at 108.43. Sustained trading above there will pave the way to 61.8% retracement at 117.36 and above. Such development would also affirm the case that corrective pattern from 131.82 high is a sideway pattern. This is the preferred case given the notable support from 55 day EMA.

Nevertheless, rejection by 108.43, followed by break of 103.01 minor support will likely extend the fall from 131.82 through 93.98, and set up a deep correction instead.

SNB rate decision plus a lot of important data

SNB rate decision is a focus this week. The central will will certainly keep monetary unchanged, and maintain the necessity of negative rate and readiness for intervention. Though, the comment on recent steep appreciation in the Franc, with EUR/CHF breaching parity, will be closely watched. Meanwhile, BoJ will release meeting minutes and ECB will release monthly bulletin.

There are also many important economic data, including PMIs from Japan, Eurozone, UK and US. Inflation data include Germany PPI, UK CPPI and PPI and Japan Tokyo CPI. Sentiment indicator include Germany Ifo, Eurozone and UK consumer confidence. US will also release durable goods orders and UK will release retail sales. Here are some highlights for the week:

- Monday: New Zealand trade balance; Germany PPI, Bundesbank monthly report.

- Tuesday: UK public sector net borrowing; Eurozone current account; Canada IPPI, RMPI;.

- Wednesday: UK CPI, PPI; US new home sales; Eurozone consumer confidence.

- Thursday: Australia PMIs; BoJ minutes, PMI manufacturing; Eurozone PMIs, ECB monthly bulletin; UK PMIs; SNB rate decision; US durable goods orders, jobless claims, current account, PMIs.

- Friday: Japan Tokyo CPI, corporate service prices; UK Gfk consumer confidence, retail sales; Germany Ifo business climate, M3 money supply; US pending home sales.

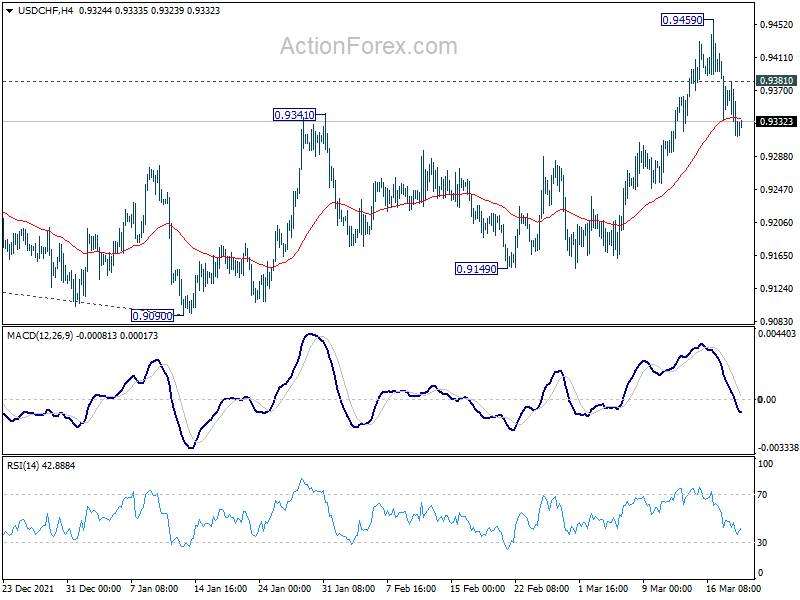

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9295; (P) 0.9338; (R1) 0.9363; More….

Intraday bias in USD/CHF is mildly on the downside at this point. Pull back from 0.9459 short term top is on track to 55 day EMA (now at 0.9248). On the upside, above 0.9381 minor resistance will flip bias back to the upside. Firm break of 0.9471 will resume the rise from 0.8756 to 61.8% projection of 0.8756 to 0.9471 from 0.9090 at 0.9532.

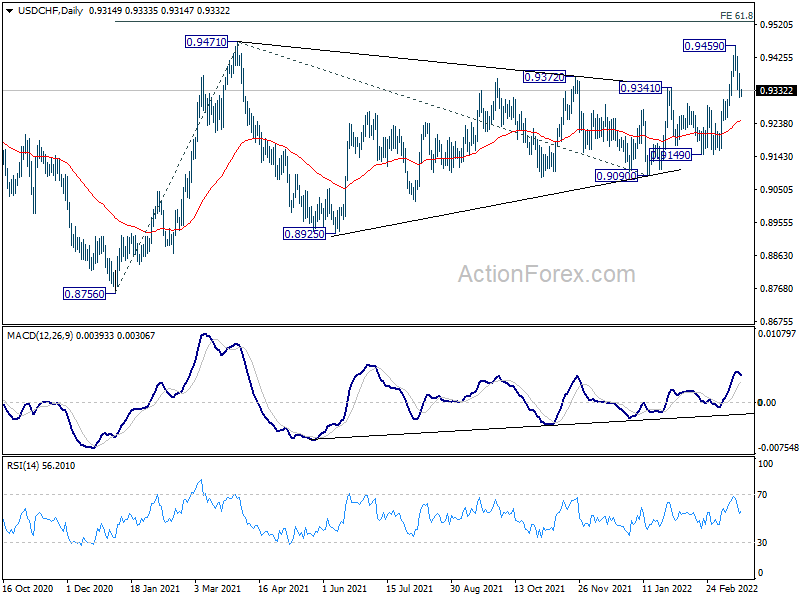

In the bigger picture, medium term outlook will be neutral at best as long as 0.9471 resistance holds. Larger down trend could still extend through 0.8756 (2021 low). However, firm break of 0.9471 will argue that whole down trend form 1.0342 (2016 high), has completed with waves down to 0.8756. A medium term up trend should be set up to target 1.0237/0342 resistance zone.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Feb | -385M | -808M | -1082M | -1126M |

| 14:01 | GBP | Rightmove House Price Index M/M Mar | 1.70% | 2.30% | ||

| 02:00 | EUR | Germany PPI M/M Feb | 1.70% | 2.20% | ||

| 07:00 | EUR | Germany PPI Y/Y Feb | 26.10% | 25.00% |