{kind=link}

Dollar turns softer in early US session after much worse than expected jobless claims data. Euro is closely following as next weakest and then Swiss Franc. On the other hand, Australian Dollar is extending post-job data gains. Canadian Dollar is also firm on oil prices. Yen is mixed for the moment as European stock markets are mixed while US futures point to mild recovery at open.

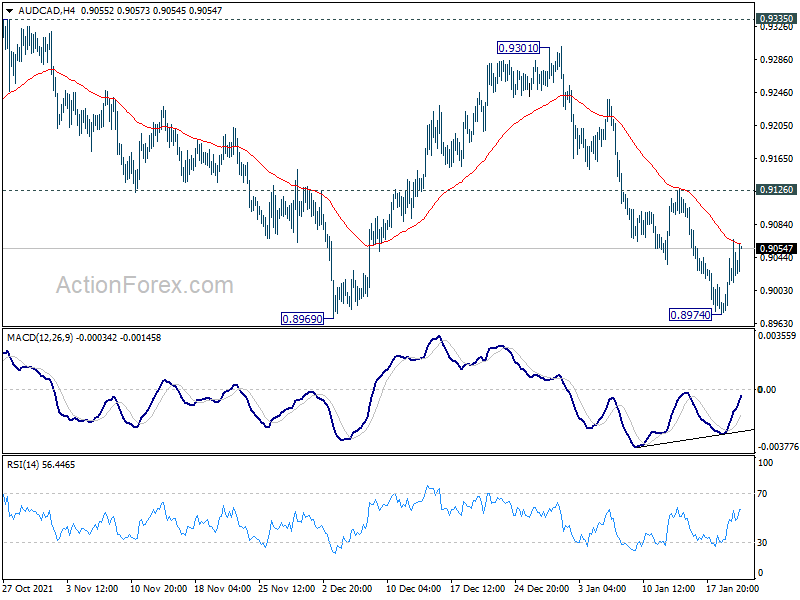

Technically, AUD/CAD appears to be bottoming at 0.8974, just ahead of 0.8969 low, on bullish convergence condition in 4 hour MACD. Further break of 0.9126 resistance should confirmation completion of fall from 0.9301 and bring stronger rise back to this resistance level. If that happens, that would be a signal of a turn in tide between Aussie and Loonie. Also, that could give additional lift to AUD/USD for rising through 0.7313 resistance.

In Europe, at the time of writing, FTSE is down -0.21%. DAX is up 0.17%. CAC is down -0.24%. Germany 10-year yield is down -0.0267 at -0.036. Earlier in Asia, Nikkei rose 1.11%. Hong Kong HSI rose 3.42%. China Shanghai SSE dropped -0.09%. Singapore Strait Times rose 0.33%. Japan 10-year JGB yield rose 0.0078 to 0.145.

US jobless claims rose sharply by 55k to 286k

US initial jobless claims rose sharply by 55k to 286k in the week ending January 15, well above expectation of 215k. Four-week moving average of initial claims rose 20k to 231k.

Continuing claims rose 84k to 1635k in the week ending January 8. Four-week moving average of continuing claims dropped -55k to 1664k, lowest since April 27, 2019.

Philly Fed manufacturing rose from 15.4 to 23.2, well above expectation of 19.9.

ECB accounts: Higher for longer inflation scenario cannot be ruled out

In the accounts of ECB’s December 15-16 meeting, Governing Council members concurred that the “recent and projected near-term increase in inflation was driven largely by temporary factors that were expected to ease in the course of 2022. ” However, it was also “cautioned” that a “‘higher for longer’ inflation scenario could not be ruled out.”

Thus, ECB should “communicate clearly that it was ready to act if price pressures proved to be more persistent and inflation failed to fall below the target as quickly as the baseline projections foresaw.” On the other hand, concerns were also expressed about “premature scaling back of monetary stimulus and asset purchases.”

A “large majority” of members agreed with the policy changes, including scaling back the pace of PEPP purchases in Q1, extend the PEPP reinvestment horizon until at changes end of 2024, increase APP net purchases temporarily.

But some couldn’t support the overall package on some reservations on “recalibration of APP purchases and the extension of the minimum PEPP reinvestment period, as well as the statement about flexibility in future asset purchases beyond the confines of the specific circumstances of the present pandemic.”

ECB Lagarde: We have every reason not to act like Fed on inflation

ECB President Christine Lagarde told France Inter radio inflation will “stabilize” and “ease gradually in the course of 2022. “.

“The cycle of the economic recovery in the U.S. is ahead of that in Europe. We thus have every reason not to act as rapidly and as brutally that one can imagine the Fed would do,” she said.

Nevertheless, she added, “we have started to react and we obviously are standing ready, to react by monetary policy measures if the figures, the data, the facts demand it.”

Eurozone CPI finalized at 5% yoy in Dec, EU at 5.3% yoy

Eurozone CPI was finalized at record 5.0% yoy in December, up from November’s 4.0%. Core CPI was finalized at 2.6% yoy. The highest contribution to came from energy (+2.46%), followed by services (+1.02%), non-energy industrial goods (+0.78%) and food, alcohol & tobacco (+0.71%).

EU CPI was finalized at 5.3% yoy, up from November’s 5.2% yoy. The lowest annual rates were registered in Malta (2.6%), Portugal (2.8%) and Finland (3.2%). The highest annual rates were recorded in Estonia (12.0%), Lithuania (10.7%) and Poland (8.0%). Compared with November, annual inflation fell in seven Member States, remained stable in two and rose in eighteen.

Australia unemployment rate dropped to 4.2%, lowest since 2008

Australia employment grew 64.8k in December to 13.242m, well above expectation of 30.0k. Full time jobs rose 41.5k while part-time jobs rose 23.3k. Unemployment rate dropped from 4.6% to 4.2%, better than expectation of 4.5%. That’s also the lowest rate since August 2008. Participation rate was unchanged at 66.1%. Hours worked rose 1.0% or 18.2m hours.

Bjorn Jarvis, head of labour statistics at the ABS, said: “The latest data shows further recovery in employment following the large 366,000 increase in November. This provides an indication of the state of the labour market in the first two weeks of December, before the large increase in COVID cases later in the month.”

“This is the lowest unemployment rate since August 2008, just before the start of the Global Financial Crisis and Lehman Brothers collapse, when it was 4.0 per cent. This is also close to the lowest unemployment rate in the monthly series – February 2008 – and for a rate below 4.0 we need to look back to the 1970’s when the survey was quarterly,” Javis added.

Japan export rose 17.5% yoy in Dec, imports rose 41.1% yoy

Japan’s export rose 17.5% yoy to record JPY 7881B in December, slowing from November’s 20.5% yoy, but beat expectation of 15.9% yoy. Exports to China grew 10.8% yoy while shipments to US rose 22.1% yoy.

Imports rose 41.1% yoy to record JPY 8463B, the second month with rate above 40% following November’s 43.8% yoy, but missed expectation of 42.8% yoy. Trade deficit came in at JPY -582B.

In seasonally adjusted term, exports dropped -0.2% mom to JPY 7363B while imports dropped -0.7% mom to JPY 7799B. Trade deficit narrowed to JPY -435B.

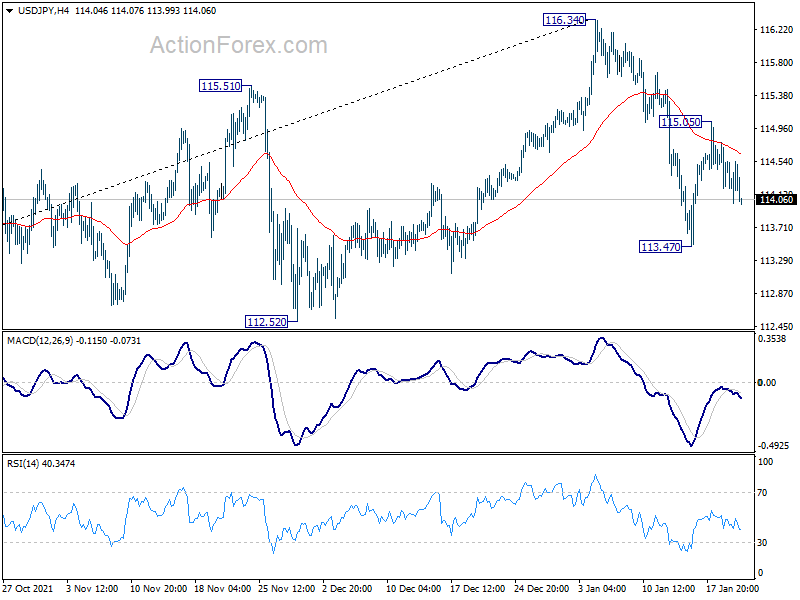

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 114.09; (P) 114.44; (R1) 114.67; More…

Intraday bias in USD/JPY stays mildly on the downside for the moment, for 113.47 support. Break there will resume the fall from 112.52 structural support. Considering bearish divergence condition in in daily MACD, further break of 112.52 will confirm that it’s already in correction to the up trend from 102.58. Deeper decline would be seen to 38.2% retracement of 102.58 to 116.34 at 111.08. On the upside, break of 115.05 will resume the rebound from 113.47. But a break of 116.34 high is not expected even in this case.

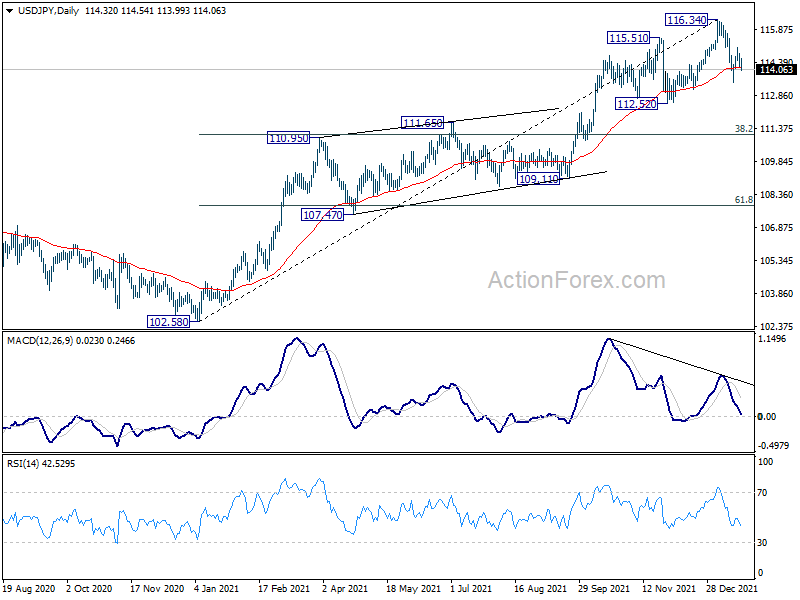

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high). Sustained break there will pave the way to 120.85 (2015 high) and raise the chance of long term up trend resumption. However, firm break of 112.52 support will dampen this bullish case and we’ll assess the outlook based on subsequent price actions later.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Dec | -0.44T | -0.73T | -0.49T | -0.47T |

| 00:00 | AUD | Consumer Inflation Expectations Jan | 4.40% | 4.80% | ||

| 00:01 | GBP | RICS Housing Price Balance Dec | 69% | 69% | 71% | |

| 00:30 | AUD | Employment Change Dec | 64.8K | 30.0K | 366.1K | |

| 00:30 | AUD | Unemployment Rate Dec | 4.20% | 4.50% | 4.60% | |

| 07:00 | EUR | Germany PPI M/M Dec | 5.00% | 0.90% | 0.80% | |

| 07:00 | EUR | Germany PPI Y/Y Dec | 24.20% | 19.40% | 19.20% | |

| 10:00 | EUR | Eurozone CPI Y/Y Dec F | 5.00% | 5.00% | 5.00% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Dec F | 2.60% | 2.60% | 2.60% | |

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 13:30 | USD | Initial Jobless Claims (Jan 14) | 286K | 215K | 230K | 231K |

| 13:30 | USD | Philadelphia Fed Manufacturing Jan | 23.2 | 19.9 | 15.4 | |

| 15:00 | USD | Existing Home Sales Dec | 6.49M | 6.46M | ||

| 15:30 | USD | Natural Gas Storage | -190B | -179B | ||

| 16:00 | USD | Crude Oil Inventories | -2.1M | -4.6M |