{kind=link}

Dollar stays generally firm in Asian session, following the post CPI rally overnight. Yen is some what helped by the selloff in stock markets despite rebound in US yields, and remains firm except versus the greenback. On the other hand, Australian Dollar tumbles sharply following much worse than expected job data, and leads other commodity currencies lower.

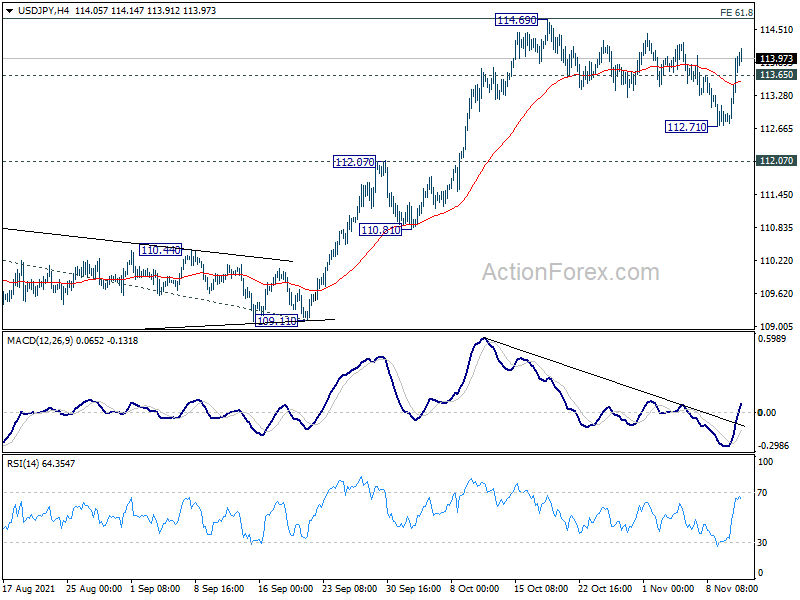

Technically, Dollar has made some progress with EUR/USD breaking through 1.1512 temporary low, and GBP/USD breaking 1.3410 support. USD/CAD’s break of 1.2497 resistance is also a sign of more rally. A focus now is on whether USD/JPY would break through 114.69 high to resume larger up trend, and confirm Dollar’s one-sided rally.

In Asia, at the time of writing, Nikkei is up 0.47%. Hong Kong HSI is down -0.15%. China Shanghai SSE is up 0.59%. Singapore Strait Times is flat. Japan 10-year JGB yield is up 0.0113 at 0.071. Overnight, DOW dropped -0.66%. S&P 500 dropped -0.82%. NASDAQ dropped -1.66%. 10-year yield rose 0.128 to 1.560.

A look at 5-yr and 10-yr yield after strong rebound

US treasury yields staged a strong rebound overnight following the much stronger than expected CPI data. Five year yield closed up 0.146 at 1.214. The development suggests that pull back from 1.251 has completed after well defending 1.042 support. The stay above rising 55 day EMA also keeps near term outlook bullish. Retest of 1.251 resistance would be seen soon. Firm break there will resume larger up trend from 0.192 to 100% projection of 0.192 to 0.988 from 0.606 at 1.402.

10-year yield also closed up 0.128 at 1.560. While the treat from 1.691 should have completed at 1.415, there is no clear sign of an upside breakout yet. Also, even if 1.691 would be broken, there is another key resistance at 1.765 ahead. Hence, near term outlook is more on the neutral side for now.

Australia employment dropped -46.3k, unemployment rate jumped to 5.2%

Australia employment decreased -46.3k in October, much worse than expectation of 50k rise. At 12.84m, employment level was back below pre-pandemic peak. Full time jobs dropped -40.4k while part-time jobs dropped -5.9k.

Unemployment rate jumped sharply from 4.6% to 5.2%, well above expectation of 4.7%. But participation rate also rose slightly from 64.5% to 64.7%. Monthly hours worked dropped -1m hours.

Bjorn Jarvis, head of labour statistics at the ABS: “The increases in unemployment show that people were preparing to get back to work, and increasingly available and actively looking for work – particularly in New South Wales, Victoria and the Australian Capital Territory. This follows what we have seen towards the end of other major lockdowns, including the one in Victoria late last year.”

“It may seem counterintuitive for unemployment to rise as conditions are about to improve. However, this shows how unusual lockdowns are, compared with other economic shocks, in how they limit being able to work and look for work.”

Japan PPI surged to 8% yoy in Oct, highest since 1981

Japan corporate goods price index rose 8.0% yoy in October, up from September’s 6.4% yoy, well above expectation of 6.9% yoy. That’s also the highest level since January 1981.

Looking at some details, lumber & wood surged 57.0% yoy. Petroleum and cola rose 44.5% yoy. Iron and steel rose 21.8%. Nonferrous metals rose 31.4% yoy. Export price rose 13.7% yoy while import price rose 38.0% yoy.

Looking ahead

UK GDP, productions and trade balance will be featured in European session. ECB will release monthly economic bulletin too. US and Canada will be on holiday.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7302; (P) 0.7348; (R1) 0.7371; More…

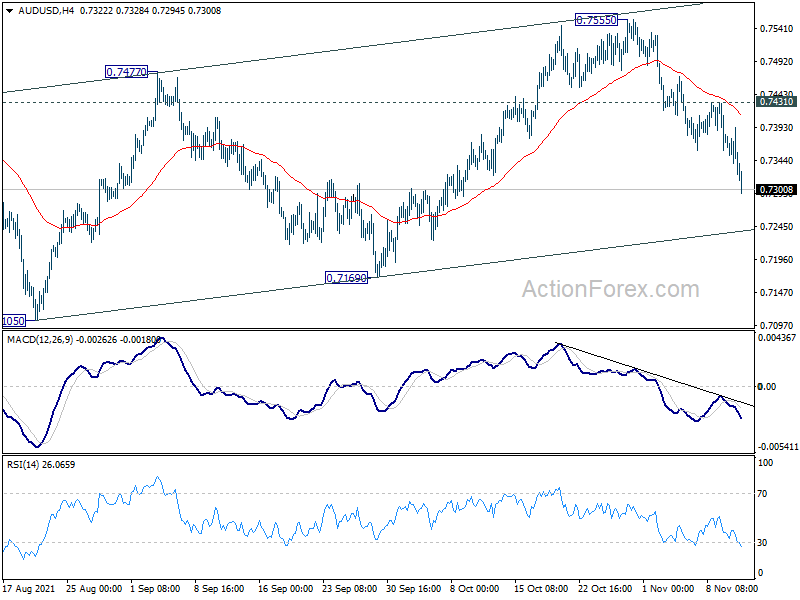

AUD/USD’s fall from 0.7555 extends to as low as 0.7294 so far today. Current development argues that corrective rise from 0.7105 has completed with three waves up to 0.7555. Intraday bias stays on the downside for 0.7169 support first, and then 0.7105 low. We’d look for bottoming signal again at around 0.6991 key support. On the upside, though, break of 0.7431 resistance is needed to indicate completion of the fall. Otherwise, further decline will remain in favor.

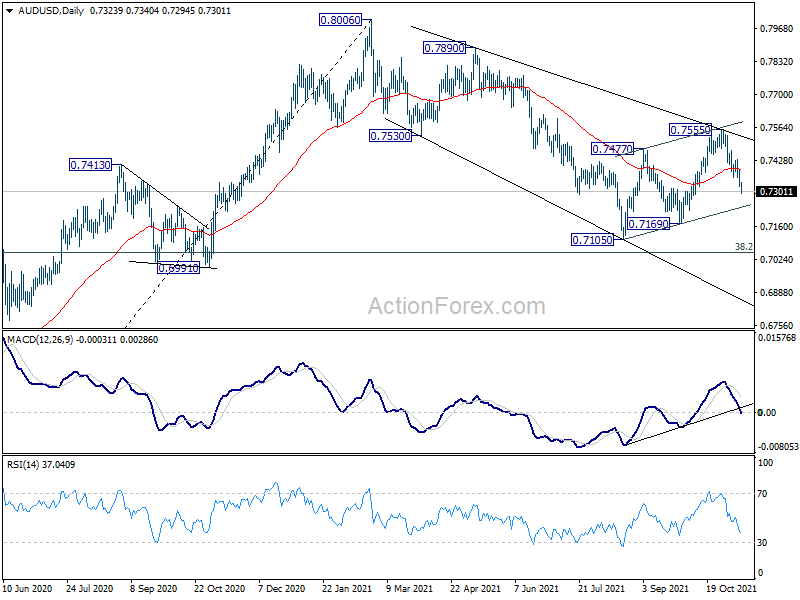

In the bigger picture, with 0.6991 cluster support (38.2% retracement of 0.5506 to 0.8006 at 0.7051) intact, we’re seeing price action from 0.8006 as a correction only. That is, up trend from 0.5506 low would resume after the correction completes. In that case, main focus will be 0.8135 key resistance (2018 high). Sustained break there will carry larger bullish implications. However, sustained break of 0.6991 will argue that the whole medium term trend has indeed reversed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Oct | 8.00% | 6.90% | 6.30% | 6.40% |

| 00:01 | GBP | RICS Housing Price Balance Oct | 70% | 68% | 68% | 69% |

| 00:30 | AUD | Employment Change Oct | -46.3K | 50K | -138K | -141.1K |

| 00:30 | AUD | Unemployment Rate Oct | 5.20% | 4.70% | 4.60% | |

| 07:00 | GBP | GDP Q/Q Q3 P | 1.50% | 5.50% | ||

| 07:00 | GBP | GDP M/M Sep | 0.50% | 0.40% | ||

| 07:00 | GBP | Index of Services 3M/3M Sep | 1.90% | 3.70% | ||

| 07:00 | GBP | Manufacturing Production M/M Sep | 0.20% | 0.50% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Sep | 4.10% | 4.10% | ||

| 07:00 | GBP | Industrial Production M/M Sep | 0.20% | 0.80% | ||

| 07:00 | GBP | Industrial Production Y/Y Sep | 3.70% | |||

| 07:00 | GBP | Goods Trade Balance (GBP) Sep | -14.3B | -14.9B | ||

| 09:00 | EUR | ECB Monthly Bulletin | ||||

| 12:00 | GBP | NIESR GDP Estimate Oct | 1.50% |