{kind=link}

While NASDAQ surged to new record high overnight, overall closes were mixed with DOW slightly down. Asia markets also lack a clear direction. Investors appear to remain cautious ahead of US non-farm payroll report tomorrow. So far, New Zealand and Australian Dollars are the strongest ones for the week. Canadian Dollar is lagging far behind with WTI oil price struggling around 68 handle. Swiss Franc and Yen are the worst performing ones. But both are just range bound against the greenback, which is clearly weak against other Europeans and commodity currencies.

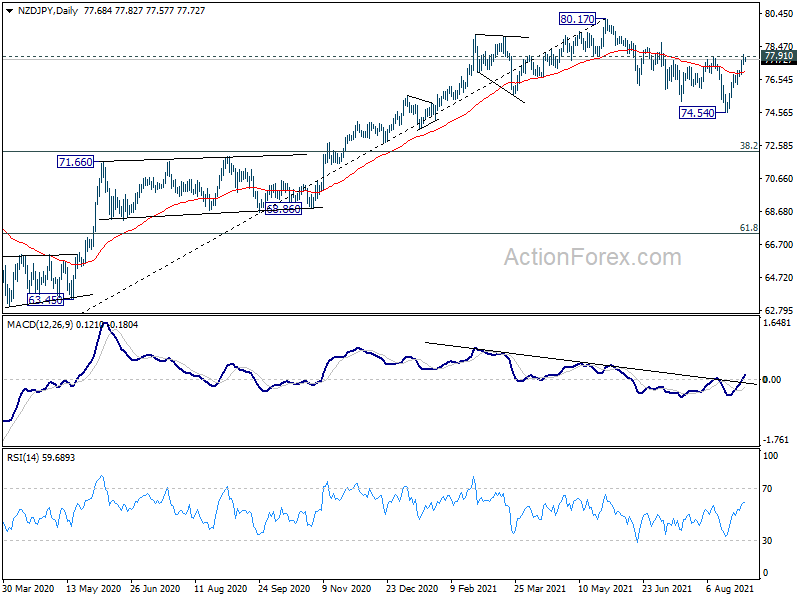

Technically, NZD/JPY’s breach of 77.91 resistance suggests that correction from 80.17 has completed at 74.54 already. It’s also the first sign that Yen crosses are staging bullish reversals. But, to play safe, we’d like to firstly see sustained trading above this 77.91 resistance in NSD/JPY. Additionally, AUD/JPY and EUR/JPY should take out corresponding resistance levels at 81.56 and 130.54 respectively, to add to the case of Yen crosses bullish reversal.

In Asia, at the time of writing, Nikkei is up 0.26%. Hong Kong HSI is up 0.08%. China Shanghai SSE is up 0.55%. Singapore Strait Times is down -0.30%. Japan 10-year JGB yield is up 0.0041 at 0.035. Overnight, DOW dropped -0.14%. S&P 500 rose 0.03%. NASDAQ rose 0.33% to new record at 15309.38. 10-year yield dropped -0.02 to 1.302.

Australia trade surplus hit record AUD 12.12B, as exports to China rose

Australia goods and services exports rose 5% mom in July to AUD 45.94B. The strong rise is exports was based on strong Asian demand for LNG and thermal coal, combined with sharply higher prices for iron ore. Exports to China also rose to record AUD 19.4B. Goods and services imports rose 3% mom to AUD 33.83B, due to sharp increase in parts and accessories for telecommunications equipment.

Trade surplus widened to AUD 12.12B, above expectation of AUD 10.1B., hitting a new record.

New Zealand terms of trade rose 3.3% in Q2 as export prices surged

New Zealand merchandise terms of trade rose 3.3% in Q2, well above expectation of 0.3%. Export prices for goods rose 8.3% while import prices rose 4.8%. Export volume for goods rose 2.9% while import volumes rose 4.4%. Export values rose 9.2% and import values rose 4.6%. Services terms of trade dropped -8.5%. Services export prices fell -1.6% while import prices rose 7.7%.

Terms of trade measures New Zealand’s purchasing power for import goods, based on the prices it receives for exports. An increase in terms of trade means that New Zealand can buy more import goods for the same quantity of exports.

BoJ Kataoka: BoJ must strengthen monetary easing

BoJ board member Goushi Kataoka, a known persistent dove, warned that the Japan economy remained in a “severe state”. The economy is heading toward recovery but “not fast enough.

He added that risks to the outlook are skewed to the downside. In particular, “risks to consumption are heightening” due to surge in Delta infections. “There’s a good chance the impact of the pandemic may last longer than expected,” he added.

Kataoka also continued his push for more aggressive monetary policy easing. “Personally, I believe the BoJ must strengthen monetary easing,” he said, as inflation would remain distant from the 2% target for years.

Looking ahead

Swiss retail sales, CPI and GDP will be released in European session while Eurozone will release PPI. Canada will release building permits and trade balance. US will release jobless claims, trade balance, factory orders and non-farm productivity.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 129.95; (P) 130.21; (R1) 130.53; More….

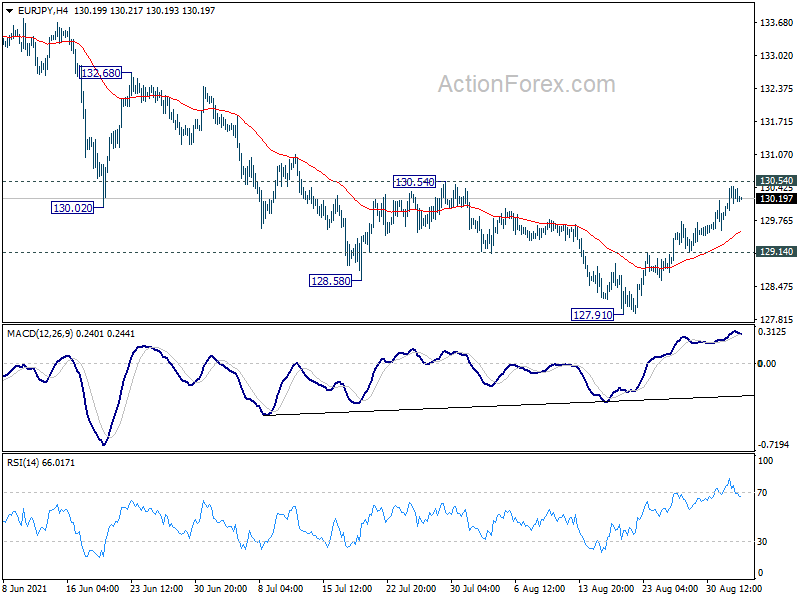

EUR/JPY’s rebound from 127.91 short term bottom is still in progress and intraday bias stays on the upside for 130.54 resistance. Sustained break there will argue that whole correction from 134.11 has completed and turn near term outlook bullish. Further rise should then be see back to retest 134.11 high. On the downside, however, below 129.14 minor support will turn bias back to the downside for retesting 127.91 low instead.

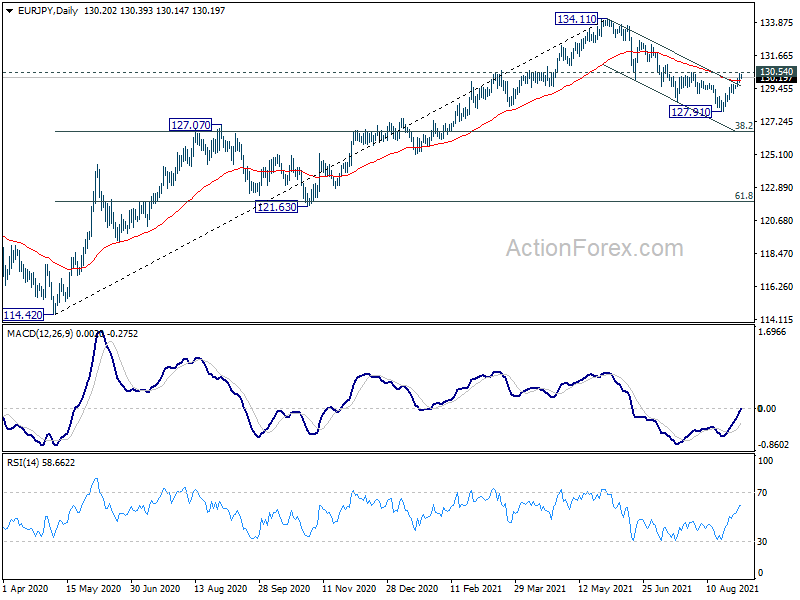

In the bigger picture, rise from 114.42 is seen as a medium term rising leg inside a long term sideway pattern. As long as 127.07 resistance turned support holds, further rise is still expected to retest 137.49 (2018 high). However, firm break of 127.07 will argue that the medium term trend has reversed, deeper fall would be seen to 61.8% retracement of 114.42 to 134.11 at 121.94.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Terms of Trade Index Q2 | 3.30% | 0.30% | 0.10% | |

| 23:50 | JPY | Monetary Base Y/Y Aug | 14.90% | 16.20% | 15.40% | |

| 1:30 | AUD | Trade Balance (AUD) Jul | 12.12B | 10.10B | 10.50B | 11.11B |

| 6:30 | CHF | Real Retail Sales Y/Y Jul | 0.20% | 0.10% | ||

| 6:30 | CHF | CPI M/M Aug | 0.10% | -0.10% | ||

| 6:30 | CHF | CPI Y/Y Aug | 0.80% | 0.70% | ||

| 7:00 | CHF | GDP Q/Q Q2 | 1.90% | -0.50% | ||

| 9:00 | EUR | Eurozone PPI M/M Jul | 1.20% | 1.40% | ||

| 9:00 | EUR | Eurozone PPI Y/Y Jul | 10.90% | 10.20% | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Aug | -92.80% | |||

| 12:30 | CAD | Building Permits M/M Jul | 6.90% | |||

| 12:30 | CAD | International Merchandise Trade (CAD) Jul | 3.2B | |||

| 12:30 | USD | Initial Jobless Claims (Aug 27) | 351K | 353K | ||

| 12:30 | USD | Trade Balance (USD) Jul | -74.5B | -75.7B | ||

| 12:30 | USD | Nonfarm Productivity Q2 | 2.40% | 2.30% | ||

| 12:30 | USD | Unit Labor Costs Q2 | 1.00% | 1.00% | ||

| 14:00 | USD | Factory Orders M/M Jul | 0.40% | 1.50% | ||

| 14:30 | USD | Natural Gas Storage | 29B |