{kind=link}

Sterling is notably lower today in otherwise mixed markets. Euro is also firm, with help from recovery against the Pound. Aussie is the stronger one, mainly because it’s paring last week’s losses. Upside is so far limited ahead of tomorrow’s RBA monetary policy decision. On the other hand, Swiss Franc softens mildly, paring some of last week’s gains.

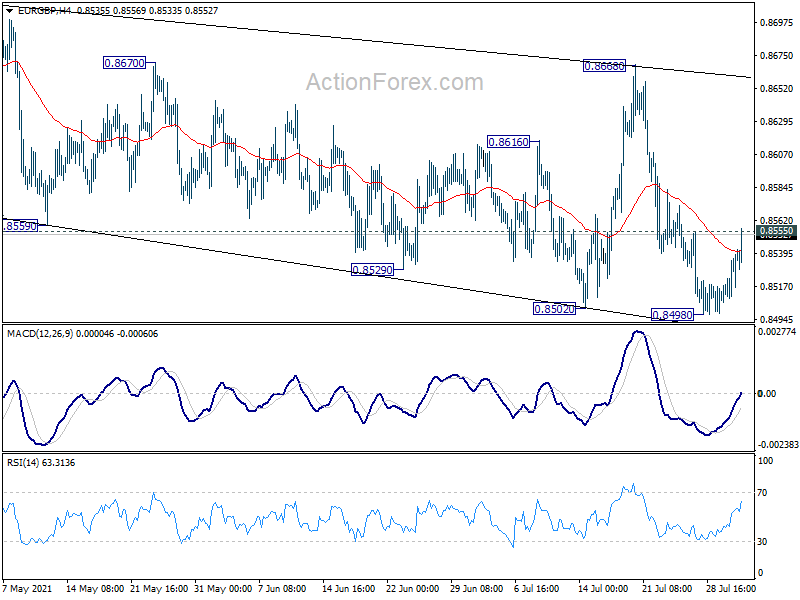

Technically, firm break of 0.8555 resistance in EUR/GBP would indicate short term bottoming at 0.8498. Stronger rebound could follow for 0.8868 resistance. If happens, we’d see if that wold translate into selling in the Pound, like breaking through 151.55 minor support in GBP/JPY. Or, Euro will rise on the rise, with EUR/USD breaking through 1.1907 temporary top.

In Europe, at the time of writing, FTSE is up 0.63%. DAX is up 0.19%. CAC is up 0.74%. Germany 10-year yield is up 0.010 at -0.449. Earlier in Asia, Nikkei rose 1.82%. Hong Kong HSI rose 1.06%. China Shanghai SSE rose 1.97%. Singapore Strait Times dropped -0.18%. Japan 10-year JGB yield rose 0.0016 to 0.021.

UK PMI manufacturing finalized at 60.4, stretched supply chains led to sharp rise in costs

UK PMI Manufacturing was finalized at 60.4 in July, down from June’s 63.9. Markit said output and new order growth eased to four-month lows. Stretched supply chains led to sharp rise in costs.

Rob Dobson, Director at IHS Markit, said: “Although July saw UK manufacturers report a further month of solid growth, scarcities of inputs, transport and labour are stifling many businesses. On one hand, manufacturers are benefiting from reopening economies…. On the other, the recent surge in global manufacturing growth has led to another month of near-record supply chain delays, exacerbated by factories and their customers building up safety stocks….

“Demand outstripping supply is also driving up prices. Input costs again rose at a near survey-record pace, leading to a near-record increase in manufacturers’ selling prices. Amid growing indications that many supply chain disruptions and raw material shortages are unlikely to be fully resolved until 2022, the outlook remains one of constrained growth combined with high inflation for the foreseeable future.”

Eurozone PMI manufacturing finalized at 62.8, inflows of new orders outstripping production to unprecedented extent

Eurozone PMI Manufacturing was finalized at 62.8 in July, down from June’s 63.4. Markit said output and order growth rates slowed, but employment rose at survey-record pace. Inflation rates hit new highs as supply chain disruptions continue.

The readings for most member states except Germany declined, but remained strong: Netherlands (67.4), Germany (65.9), Austria (63.9), Italy (60.3), Spain (58.0), France (58.0), Greece (57.4).

Chris Williamson, Chief Business Economist at IHS Markit said: “July survey showed inflows of new orders outstripping production to an extent unprecedented in the survey’s 24-year history. Capacity constraint indicators continue to flash red. Input shortages worsened again in July at a near record rate and July saw another near-record rise in backlogs of work…. Prices pressures meanwhile show no sign of abating, with July seeing another record increase in both input costs and prices charged for goods as demand exceeds supply, and concerns over future supply availability flare up again.”

Germany PMI Manufacturing was finalized at 65.9 in July, up from June’s 65.1. The future was the third-highest since the survey began in 1996. There was survey-record increase in employment. Also, both price indices reached new record highs.

France PMI Manufacturing was finalized at 58.0 in July, down from June’s 59.0. Markit said production growth remained strong, but slowed. Supplier performance continued to deteriorate substantially. Input prices rose at fastest rate since March 2011.

Swiss CPI rose to 0.7% yoy in Jul, retail sales rose 0.1% yoy in Jun

Swiss CPI came in at -0.1% mom, 0.7% yoy in July, matched expectations. That compared to June’s reading of 0.1% mom, 0.6% yoy.

Retail sales rose 0.1% yoy mom in real term in June, well below expectation of 3.4% yoy. Sales excluding service stations dropped -0.5% yoy. Food, drinks and tobacco dropped -2.1% yoy. Non-food sector rose 1.2% yoy.

SVME PMI rose to 71.1 in July, up from 66.7, above expectation of 61.5.

Australia AiG manufacturing dropped to 60.8, further easing ahead

Australia AiG Performance of Manufacturing Index dropped -2.4 pts to 60.8 in July. Looking at some details, production rose 1.1 to 61.8. Employment rose 0.5 to 60.8. New orders dropped sharply by -8.1 to 62.5. Exports dropped -6.6 to 53.6. Input prices rose 5.8 to 84.6. Selling prices rose 1.1 to 64.7.

Ai Group Chief Executive Innes Willox said: “While COVID-19 outbreaks and associated restrictions in some states undoubtedly dampened the upswing in activity and shook confidence, the manufacturing sector recorded another strong month of expansion in July…. The slower pace of the manufacturing upswing in July and the slower pace of growth in new orders suggest further easing in the months ahead. A significant headwind for the sector is that Sydney’s toughest restrictions relate to local government areas where there is a concentration of manufacturing sites and the manufacturing workforce.”

Japan PMI manufacturing finalized at 53.0 in Jul, sharp rise in cost burdens

Japan PMI Manufacturing was finalized at 53.0 in July, up from June’s 52.4. Markit said output and new orders rose at faster rates. There were sharp rise in cost burdens amid supply chain disruption. Businesses reported softer optimism regarding future output.

Usamah Bhatti, Economist at IHS Markit, said: “The Japanese manufacturing sector continued to see an improvement in operating conditions… the pace of expansion quickened as firms recorded stronger growth in both output and new orders… supply chain disruption continued to impact activity within the sector, with firms recording the second greatest deterioration in lead times in over a decade. Material shortages and logistical disruption contributed to a rapid rise in average cost burdens, as input prices rose at the fastest pace since September 2008.

China Caixin PMI manufacturing dropped to 50.3 in Jul, recovery not yet solid

China Caixin PMI Manufacturing dropped to 50.3 in July, down from 51.3, below expectation of 51.0. Caixin said output growth slowed amid slight drop in new orders. Staffing levels were broadly unchanged while inflationary pressures eased.

Wang Zhe, Senior Economist at Caixin Insight Group said: “China’s official second-quarter economic figures were in line with expectations, but the Caixin China manufacturing PMI in July and relevant data suggested the recovery of the economy is not yet solid. The economy is still facing huge downward pressure, and we need to ensure entrepreneurs’ confidence.”

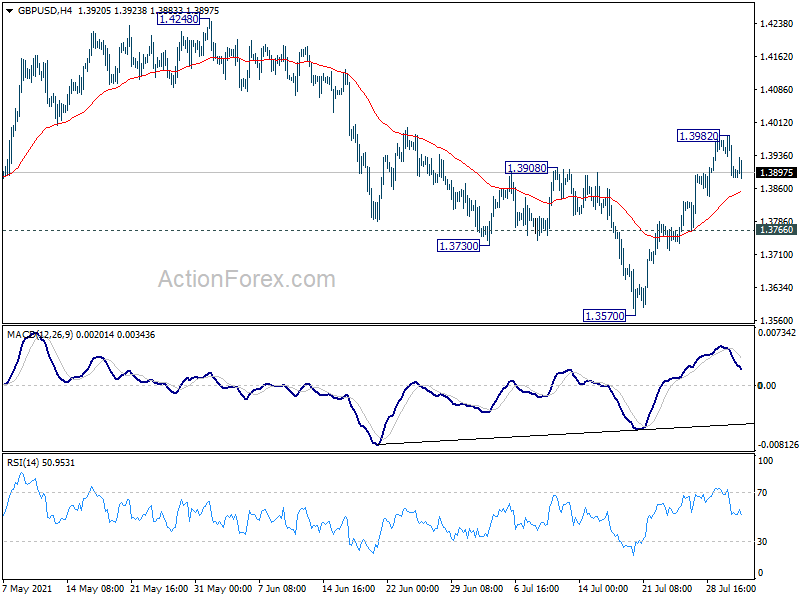

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3869; (P) 1.3927; (R1) 1.3965; More….

GBP/USD is staying in consolidation below 1.3982 temporary top. Intraday bias remains neutral at this point. Corrective pattern from 1.4240 could have completed with three waves down to 1.3570. Further rise is expected as long as 1.3766 support holds. On the upside, break of 1.3982 will resume the rise from 1.3570 to retest 1.4248 high. However, break of 1.3766 support will dampen this bullish view and bring retest of 1.3570.

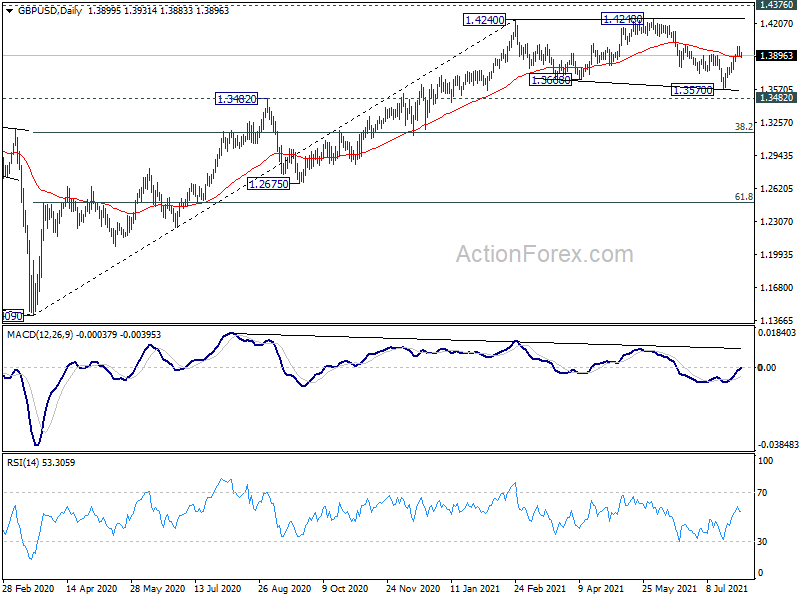

In the bigger picture, as long as 1.3482 resistance turned support holds, up trend from 1.1409 should still continue. Decisive break of 1.4376 resistance will carry larger bullish implications. However, firm break of 1.3482 support will argue that the rise from 1.1409 has completed. GBP/USD would then be seen in another leg of long term range pattern between 1.1409 and 1.4376. Deeper fall could then be seen to 61.8% retracement of 1.1409 to 1.4248 at 1.2493, and even below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Manufacturing Index Jul | 60.8 | 63.2 | ||

| 0:30 | JPY | Manufacturing PMI Jul F | 53 | 52.2 | 52.2 | |

| 1:00 | AUD | TD Securities Inflation M/M Jul | 0.50% | 0.40% | ||

| 1:45 | CNY | Caixin Manufacturing PMI Jul | 50.3 | 51 | 51.3 | |

| 5:00 | JPY | Consumer Confidence Index Jul | 37.5 | 36 | 37.4 | |

| 6:00 | EUR | Germany Retail Sales M/M Jun | 4.20% | 2.00% | 4.20% | 4.60% |

| 6:30 | CHF | Real Retail Sales Y/Y Jun | 0.10% | 3.40% | 2.80% | |

| 6:30 | CHF | CPI M/M Jul | -0.10% | -0.10% | 0.10% | |

| 6:30 | CHF | CPI Y/Y Jul | 0.70% | 0.70% | 0.60% | |

| 7:30 | CHF | SVME PMI Jul | 71.1 | 66 | 66.7 | |

| 7:45 | EUR | Italy Manufacturing PMI Jul | 60.3 | 61.5 | 62.2 | |

| 7:50 | EUR | France Manufacturing PMI Jul F | 58 | 58.1 | 58.1 | |

| 7:55 | EUR | Germany Manufacturing PMI Jul F | 65.9 | 65.6 | 65.6 | |

| 8:00 | EUR | Eurozone Manufacturing PMI Jul F | 62.8 | 62.6 | 62.6 | |

| 8:30 | GBP | Manufacturing PMI Jul F | 60.4 | 60.4 | 60.4 | |

| 13:45 | USD | Manufacturing PMI Jul F | 63.1 | 63.1 | ||

| 14:00 | USD | ISM Manufacturing PMI Jul | 60.8 | 60.6 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jul | 93.2 | 92.1 | ||

| 14:00 | USD | ISM Manufacturing Employment Jul | 49.9 | |||

| 14:00 | USD | Construction Spending M/M Jun | 0.30% | -0.30% |