{kind=link}

New Zealand Dollar rises broadly after RBNZ halts its asset purchase program. The movement also takes Aussie slightly higher. On the other hand, Dollar is not quite able to extend the post-CPI rally, and softens slightly. European majors are currently mixed. Focus will now turn to BoC policy decision and the reaction in Canadian Dollar next.

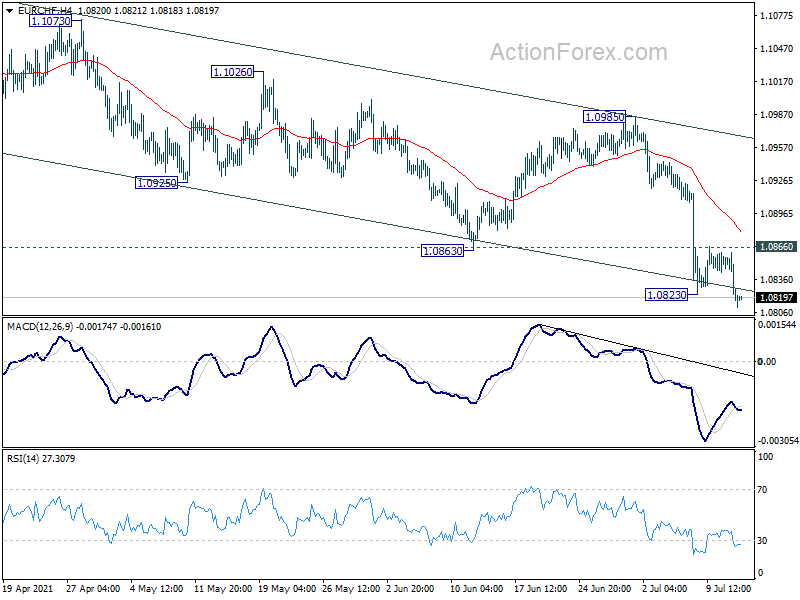

Technically, EUR/USD’s break of 1.1780 temporary low suggests resumption of recent decline. But corresponding levels in GBP/USD, AUD/USD, USD/CHF and USD/CAD are still holding. On the other hand, EUR/GBP has taken out 0.8529 support to resume the choppy fall from 0.8718. EUR/CHF has also broken 1.0823 support to resume the fall from 1.1149. Hence, the fall in EUR/USD is more due to weakness in Euro for now.

In Asia, at the time of writing, Nikkei is trading down -0.26%. Hong Kong HSI is down -0.56%. China Shanghai SSE is down -0.48%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is down -0.0040 at 0.021. Overnight, DOW dropped -0.31%. S&P 500 dropped -0.35%. NASDAQ dropped -0.38%. 10-year yield rose 0.052 to 1.415.

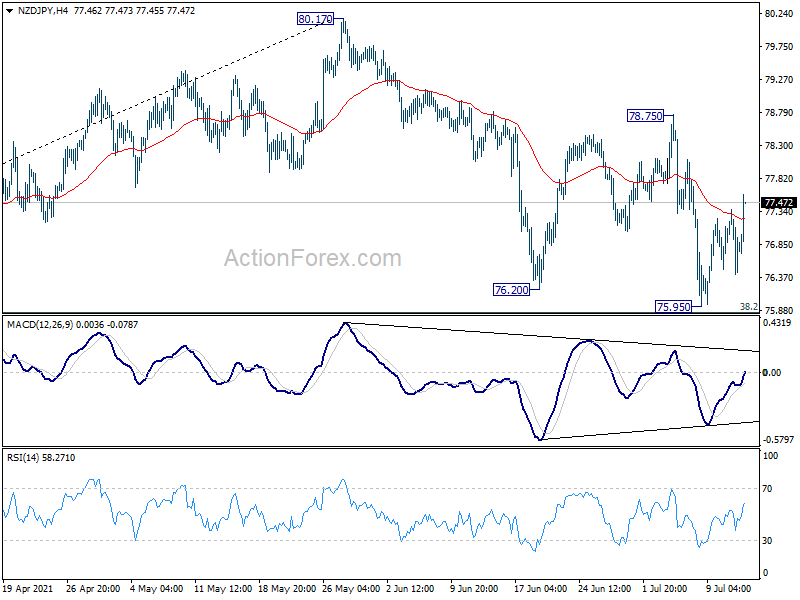

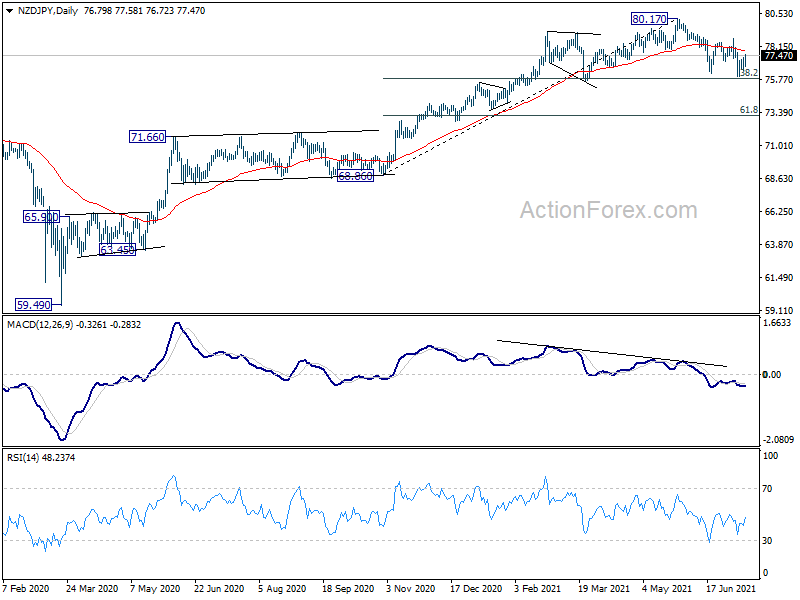

RBNZ halts asset purchases, NZD/JPY jumps

RBNZ surprised the markets as it announced to halt the additional asset purchases under the Large Scale Asset Purchase (LSAP) program by July 23. Meanwhile, OCR was kept unchanged at 0.25%. and the Funding for Lending Program was maintained. The Committee agreed that “the level of monetary stimulus could now be reduced to minimise the risk of not meeting its mandate.”

The central bank said the economy “remains robust” despite ongoing impact from international border restrictions. Aggregate economic activity is already “above its pre-COVID-19 level”. It expected “near-term spikes” in headline CPI in Q2 and Q3, reflecting “one-off” or “temporary” factors. In the absence of any further significant shocks, “more persistent consumer price inflation pressure is expected to build over time due to rising domestic capacity pressures and growing labour shortages”.

New Zealand Dollar jumps broadly after the surprised move by RBNZ. NZD/JPY is back above 77 handle after hitting 75.95 last week. Overall outlook is unchanged that price actions from 80.17 are seen as a correction to rise from 68.86 only. We’d expect strong support from 38.2% retracement of 68.86 to 80.17 at 75.84 to complete the correction.

Focus will now turn to whether current rebound could extend through 78.75 resistance to indicate that such correction has completed. In this case, stronger rise would be seen back to retest 80.17 high first.

Australia Westpac consumer sentiment rose to 108.8 despite NSW lockdown

Australia Westpac-Melbourne Institute Consumer Sentiment rose 1.5% to 108.8 in July, up from 107.2. Confidence has “held up overall” despite a sharp fall in New South Wales, as Victoria and Western Australia recorded strong “bounce-backs”.

Westpac said RBA is not expected announce any change at August 3 meeting. The focus would mainly be on the Statement on Monetary Policy on August 6. RBA would have a few more weeks to assess the impact of the lockdown in Sydney.

Fitch affirms US rating at AAA with negative outlook

Fitch Ratings affirmed US Long-Term Foreign Currency Issuer Default Rating (IDR) at “AAA” with a “negative” outlook. It said, the rating is “supported by structural strengths that include the size of the economy, high per capita income and a dynamic business environment.” It’s “debt tolerance” is considered “higher” than that of other AAA sovereigns.

The negative outlook reflects “ongoing risks to the public finances and debt trajectory, notwithstanding the improvement in Fitch’s fiscal and debt projections since its last review”. Key variables including “real interest rates and fiscal deficits may not follow the expected path, potentially creating downside risk.”

BoC to continue tapering, EUR/CAD range bound

BoC is generally expected to continue with tapering today, reducing weekly asset purchases from CAD 3B to CAD 2B. It’s also expected to maintain the projection that first rate hike would happen in H2 of 2022. The focuses would be on new economic projections, in particular, on whether inflation forecasts would be up graded significantly.

Here are some previews on BoC:

- BOC Preview – Hawkish Stance to Maintain with More Tapering

- BOC Preview: Ready To Continue Tapering, But Does That Mean USD/CAD Will Move Lower?

- Bank of Canada to Taper Again as Loonie Succumbs to Delta Concerns

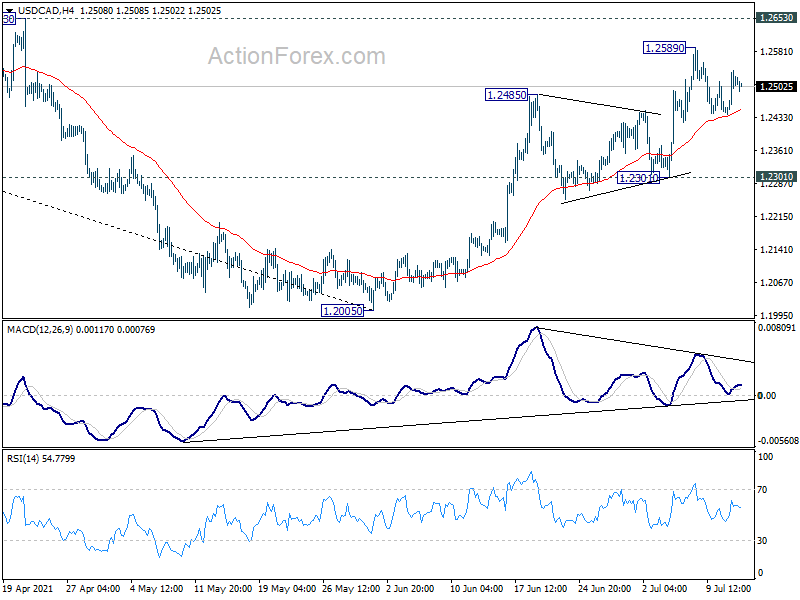

Canadian Dollar’s reaction to BoC’s tapering hasn’t been positive so far. Outlook in EUR/CAD is unclear. Bullish convergence in daily MACD argues that medium term momentum is diminishing. Yet, it failed to sustain above the 55 day EMA, despite rebounding to 1.4913. Also, price actions from 1.4580 are more corrective looking than not. So, we’d see if today’s BoC announce could finally trigger deeper fall back towards 1.4580.

Looking ahead

UK CPI and PPI are the main focuses in European session while Eurozone will release industrial production. Later in the day, Canada will release manufacturing sales alongside BoC rate decision. Fed will release Beige Book economic report.

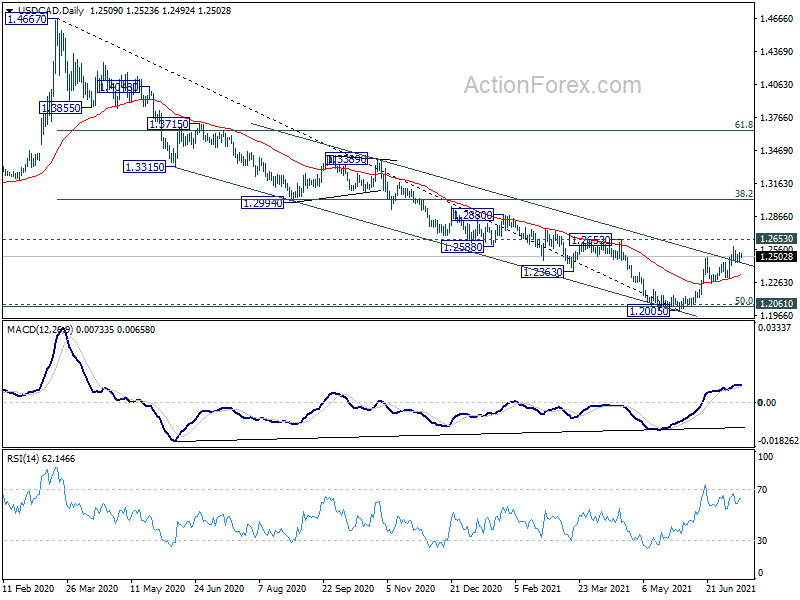

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2458; (P) 1.2499; (R1) 1.2554; More…

Intraday bias in USD/CAD remains neutral as consolidation from 1.2589 is extending. Another rise is still in favor as long as 1.2301 support holds. Break of 1.2589 will target 1.2653 structural resistance to confirm larger bullish reversal. However, on the downside, break of 1.2301 support will dampen the bullish case and turn bias back to the downside for 1.2005 low instead.

In the bigger picture, fall from 1.4667 is seen as the third leg of the corrective pattern from 1.4689 (2016 high). It might have completed after hitting 1.2061 (2017 low) and 50% retracement of 0.9406 to 1.4689 at 1.2048. Sustained break of 38.2% retracement of 1.4667 to 1.2005 at 1.3022 will pave the way to 61.8% retracement at 1.3650. Overall, medium term outlook remains neutral at worst with 1.2048/61 support zone intact.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | Westpac Consumer Confidence Jul | 1.50% | -5.20% | ||

| 2:00 | NZD | RBNZ Interest Rate Decision | 0.25% | 0.25% | 0.25% | |

| 4:30 | JPY | Industrial Production M/M May F | -6.50% | -5.90% | -5.90% | |

| 6:00 | GBP | CPI M/M Jun | 0.20% | 0.60% | ||

| 6:00 | GBP | CPI Y/Y Jun | 2.20% | 2.10% | ||

| 6:00 | GBP | Core CPI Y/Y Jun | 2.00% | 2.00% | ||

| 6:00 | GBP | RPI M/M Jun | 0.30% | 0.30% | ||

| 6:00 | GBP | RPI Y/Y Jun | 3.40% | 3.30% | ||

| 6:00 | GBP | PPI Input M/M Jun | 1.20% | 1.10% | ||

| 6:00 | GBP | PPI Input Y/Y Jun | 10.80% | 10.70% | ||

| 6:00 | GBP | PPI Output M/M Jun | 0.60% | 0.50% | ||

| 6:00 | GBP | PPI Output Y/Y Jun | 4.80% | 4.60% | ||

| 6:00 | GBP | PPI Core Output M/M Jun | 0.30% | 0.40% | ||

| 6:00 | GBP | PPI Core Output Y/Y Jun | 3.20% | 2.70% | ||

| 9:00 | EUR | Eurozone Industrial Production M/M May | 0.20% | 0.80% | ||

| 12:30 | USD | PPI M/M Jun | 0.50% | 0.80% | ||

| 12:30 | USD | PPI Y/Y Jun | 7.10% | 6.60% | ||

| 12:30 | USD | PPI Core M/M Jun | 0.40% | 0.70% | ||

| 12:30 | USD | PPI Core Y/Y Jun | 5.30% | 4.80% | ||

| 12:30 | CAD | Manufacturing Sales M/M May | -1.10% | -2.10% | ||

| 14:00 | CAD | BoC Interest Rate Decision | 0.25% | 0.25% | ||

| 14:30 | USD | Crude Oil Inventories | -6.9M | |||

| 15:15 | CAD | BoC Press Conference | ||||

| 18:00 | USD | Fed’s Beige Book |